Trending

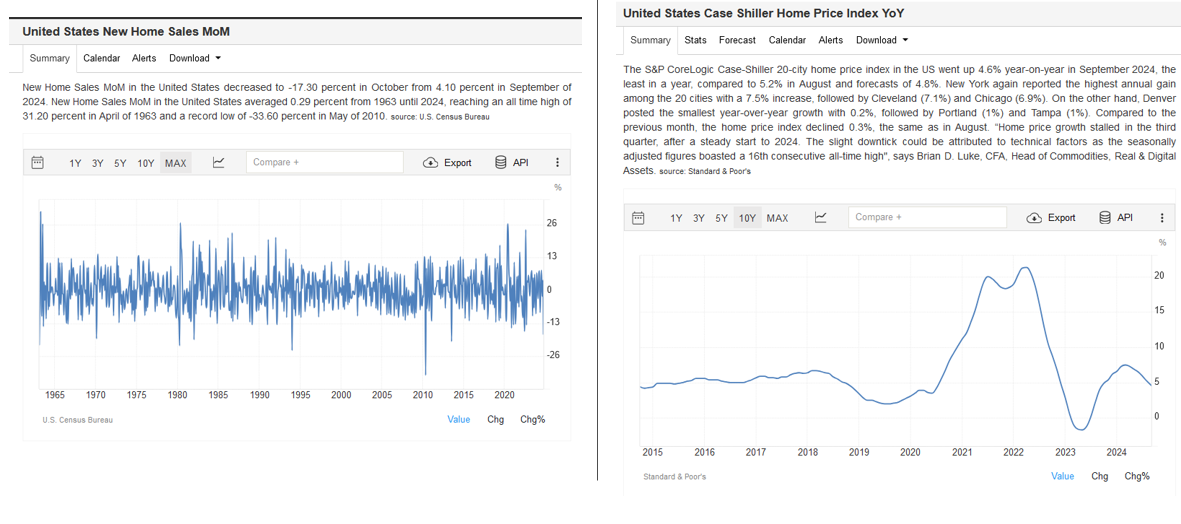

New home sales fell by 17.30% in October, marking the most significant monthly decline in ten years, as shown in the graph on the left below. Furthermore, the supply of new homes on the market rose from 7.7 to 9.5 months. Not surprisingly, building permits fell by 0.4% following a 3.1% decline last month due to slowing sales. New home sales have been negative in six of the previous eight months.

Furthermore, the Case-Shiller home price index shows weakness in the housing market. The latest report shows that previously owned home prices fell by 0.3%, bringing annual home inflation down from 5.2% to 4.6%. As the graph on the right shows, the index is now back to levels or even below those seen in the five years before the pandemic. Furthermore, it continues to decline from the recent peak of 7.5% earlier this year.

The housing data is important to the Fed for two reasons. Most critical, shelter prices, accounting for 40% of CPI, have been elevated. Alongside zero-inflation rental data, which we have shared numerous times, yesterday’s data further confirms that current housing inflation is well below reported CPI shelter prices. Therefore, CPI is overstated. Secondly, employment in the homebuilding industry has been robust. With declining sales and fewer new homes permitted for construction, homebuilders will likely have to pare some of their workforce. Given the Fed’s attention to employment and inflation, the recent housing data supports the Fed if they elect to cut by 25bps in December.

What To Watch

Earnings

![]()

Economy

Market Trading Update

Last week, we discussed the increasingly bullish market forecasts for next year. We also noted that the market tends to trade positively heading into the Thanksgiving holiday, to which the market did not disappoint.

For the week, while there was a bit of sloppy trading along the way, the market finished at new highs, eclipsing the 6000 level on Friday. Technically, the market remains in a very bullish setup, holding support at the 20-DMA and then breaking out to new highs. That rally reversed the short-term “sell signal,” which gives the market room to trade higher into the first week of December. The rising trend line from the August lows remains the likely peak to any rally in December, and as noted last week, expect some weakness in the second and third week of December as mutual funds make annual distributions. For now, any corrective action in early December should be bought in anticipation for a rally into year end.

As we discussed previously, the key drivers for December will be continued share repurchases, portfolio manager rebalancing, and window dressing for year-end reporting. These supports will continue into year-end, and with the Federal Reserve likely to cut rates in mid-December, we expect market participants to remain on the “bull train” for now. As suggested last week:

“If you are underweight equities, consider minor pullbacks and consolidations to add exposure as needed to bring portfolios to target weights. Pullbacks will likely be shallow, but being ready to deploy capital will be beneficial. Once we pass the inauguration, we can assess what policies will likely be enacted and adjust portfolios accordingly.”

The Week Ahead

This week’s jobs data will help guide the Fed’s rate decision on December 18th. The BLS JOLTs report leads the way on Tuesday. Analysts expect the number of job openings to continue to decline to 7.38 million, down from 7.44 million. Job separation and hires will be closely followed as well. Forecasts expect ADP to show the addition of 240k jobs last month. Lastly, after the disappointing addition of only 12k jobs last month, forecasts are for nearly 200k in the BLS report on Friday. The BLS data and any revisions to last month’s data will make gauging employment tricky due to the two hurricanes and their impact on the job market. Also of note this week is the ISM manufacturing and services surveys. It will be interesting to see how the election results initially impact economic sentiment.

The Fed will go into a media blackout after this week. Therefore, we should expect many members to prepare the market for their coming meeting. The speakers on Friday after the employment data may be most relevant.

Memories Of PIIGS

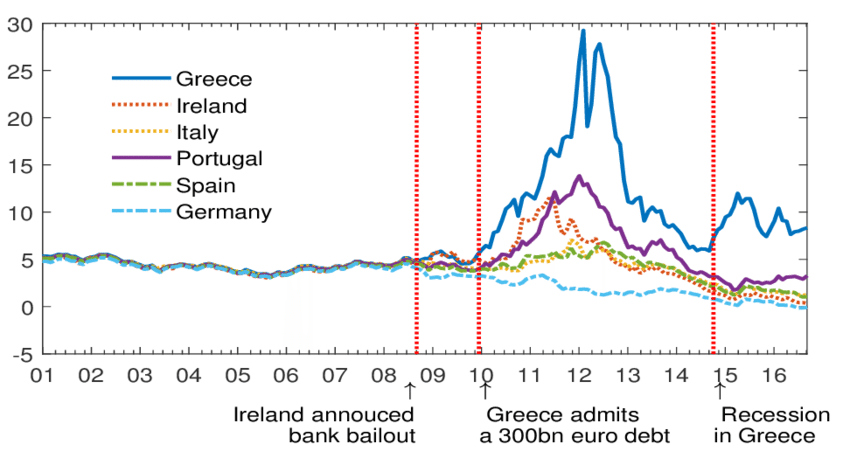

Following the U.S. financial crisis, several eurozone members, known as the PIIGS (Portugal, Ireland, Italy, Greece, and Spain), saw their bond yields surge as investors feared they could not refund maturing debt and make payments on existing debt. The first graph below shows how the bond yields on the debt of the PIIGS rose sharply while the European bellwether Germany fell. We bring this up because French bond yields have been rising rapidly. As the second graph shows, yields on French sovereign debt are at their widest spread to German debt since the Euro crisis.

The market is concerned that France may not pass a budget and enact spending reductions. Per Bloomberg:

The market nerves reflect investor concerns over Prime Minister Michel Barnier’s ability to pass a budget for next year and enact spending cuts to reduce the country’s deficit. The far-right National Rally party’s Marine Le Pen has vowed to bring down his administration with a no-confidence motion if its demands are not met, with the matter likely to come to a head in December.

Adding to the unease, Le Parisien newspaper reported that President Emmanuel Macron believed that Le Pen would carry out her threats, and that Barnier would be ousted soon by a no-confidence vote. Macron’s office denied he made such comments. Barnier warned the country faces a “storm” in financial markets if his budget proposals are rejected and the government is voted out of power.

Unlike in 2012, other European nations do not appear to have credit issues. However, the situation in France could escalate and spread fear among sovereign debt investors. Such would likely manifest in higher yields for associated countries and demand for safer bonds like those of Germany and the U.S.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”