Trending

Written by: Karen Watkin, CFA and Edward Williams

Coming into 2023, many economists and market observers set their base cases to a global recession in the second half of the year. In their view, rapidly tightening monetary policy across nearly all central banks would translate into tighter financial conditions and slower growth in the real economy.

Reality unfolded quite differently.

Economic activity was resilient enough to surprise even the most bullish investors. A historically tight labor market bolstered a strong US consumer, while a warmer-than-expected European winter reduced the risk of an energy crisis—though headwinds from a China slowdown remained. This backdrop forced rates up across the board, and the market pushed back its expectations for rate cuts deep into 2024, acknowledging the “higher for longer” narrative (Display).

We think the rate-hike cycle is likely done, but rates should stay high until the economy shows signs of cooling. Central banks have done well to avoid overtightening—at least on initial assessment. But monetary policy can work on a lag, so growth should be more challenged in 2024. Geopolitical risks are rising and a heavy election year looms, so investors should plan for more volatility than they may expect today. Where does lower growth and the potential for more volatility in 2024 leave multi-asset income investors and their portfolio positioning?

Broadly speaking, our perspectives fit into three themes.

Use Equities for Growth, and Build Up Your Defenses

With bond yields at decade highs, there’s less need to lean into income-generating equities alone. Instead, investors should view their equity allocations as the core driver of growth and upside potential within a multi-asset strategy.

A slower-growth landscape doesn’t bar stocks from delivering reasonable returns, but selectivity matters, as does allocating to companies that offer persistent growth and profitability. US large-cap stocks, for example, have consistently demonstrated these traits, and even though valuations are richer, underlying secular trends may enable this pattern to last (Display).

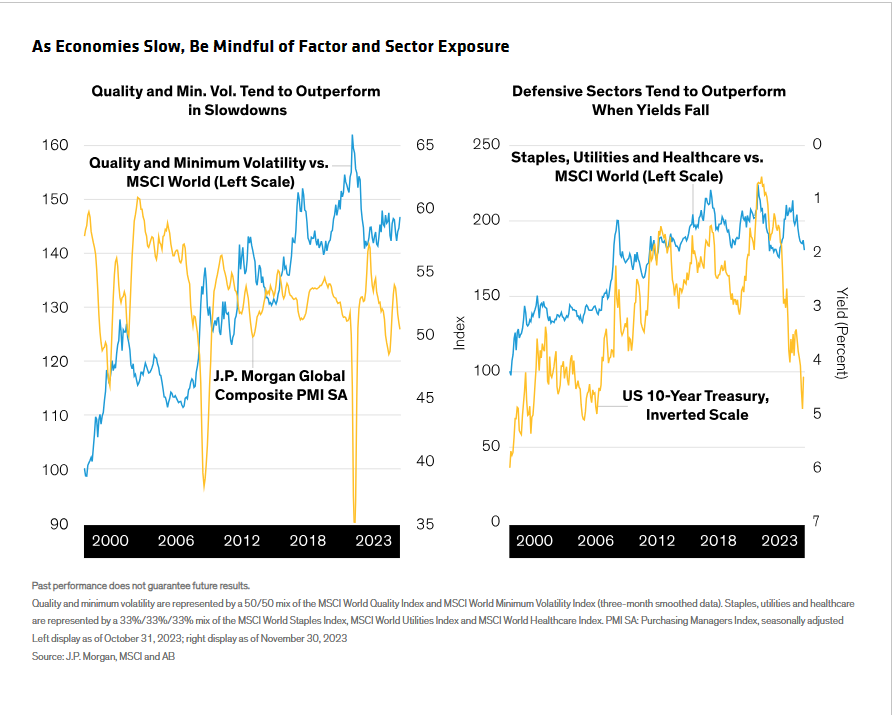

Investors should also look carefully at their factor and sector exposures, because performance patterns can differ quite a bit (Display). For instance, our research indicates that in the slowdown phase of the business cycle, market segments that emphasize quality and stability have tended to produce better risk-adjusted returns than the broader market. Businesses that can demonstrate solid balance sheets and durable growth are typically rewarded when margins soften and pricing power deteriorates.

We see opportunity in more defensive areas, including consumer staples, utilities and healthcare, than in more cyclical sectors, such as financials and consumer discretionary. Defensive names typically outperform once the rate cycle peaks, and should offer better downside mitigation if markets are more volatile. Current valuations may also offer some upside. While recession or a hard landing aren’t our base case, investors seem to have priced out all risk of these outcomes, so companies typically expected to be more resilient as growth slows are trading at attractive discounts versus the broader market.

Seek Opportunities in High-Quality Credit

Excess yields of credit investments over government bonds have dipped from their highs of the past year or so, but yields remain compelling across the quality spectrum, given the sharp rate surge. US investment-grade bonds, for instance, yield close to 6%, roughly three times their level at the end of 2021 and near their post-GFC heights.

As we move through 2024, we expect these attractive all-in yields (Display, left) to draw demand from investors who seek income from quality issuers and expect cash yields to decline. This demand could enhance performance from already high starting yields. Even if credit spreads don’t tighten much during 2024, investors can access attractive total-return potential.

Market fundamentals, such as interest-coverage ratios and leverage, are showing very early signs of deterioration (Display, right), but they’re starting from a very strong footing and in great shape versus previous late-cycle environments. But we’re conscious of risk pockets. Because there’s less need to reach for yield, it’s prudent to stay selective, favoring higher-quality issuers over other parts of the market or alternative income strategies that typically carry more tail risk.

Don’t Give Up on Duration Exposure

The unexpectedly strong economy in 2023 (particularly in the US) and related surge in bond yields meant another painful year for duration-sensitive assets. The return gap between long-term Treasury bonds and equities reached its widest since the late 1990s: around 70% over the past three years (Display).

While our view, along with that of many other investors, on adding duration was a little early in 2023, we believe that the evolving situation since then makes a case for considering more duration than normal as we look ahead to 2024.

There’s more clarity now on the inflation backdrop, making us more certain that we’ve reached, or are very near to reaching, peak interest rates, and yields have tended to decline in advance of rate cuts (Display). In these environments, duration-sensitive assets such as Treasuries have historically flourished and—a key point for multi-asset investors—provided effective diversification to risk assets.

The key risk for duration exposure is that inflation surprises to the upside. However, with yields relatively high, we would expect assets such as Treasuries to provide downside mitigation if there’s a growth shock or escalation in geopolitical tensions. We think having this “recession hedge” is particularly important, to the extent that markets may be complacent heading into 2024.

Looking at the Big (Income) Picture

As we prepare to turn the calendar on this year, we believe multi-asset investors should stay patient and selective. Growth will likely be slower in 2024, as tighter monetary policy weighs on the real economy.

The focus should be on market segments more likely to be better positioned to weather higher-for-longer rates. For stocks, this means an added focus on quality growth and a tilt toward defensive sectors that tend to hold up better as economic conditions moderate. We also prefer higher-quality credit, and we think investors would do well to lock in yields that have rarely been this attractive in recent memory.

In our view, a multi-asset approach should be well placed in 2024, with high income from bonds combining nicely with the growth potential of equities. Duration exposure will likely be an important diversifier for multi-asset income strategies—bringing a crucial source of potential downside mitigation if the economic picture deteriorates.

Related: When Disaster Strikes: Gauging the Investment Risk of Natural Hazards