Trending

As money market account balances soar, the mainstream media again proclaims, “There is $6 trillion of cash on the sidelines just waiting to come into the market.”

No? Well, here it is directly from YahooFinance:

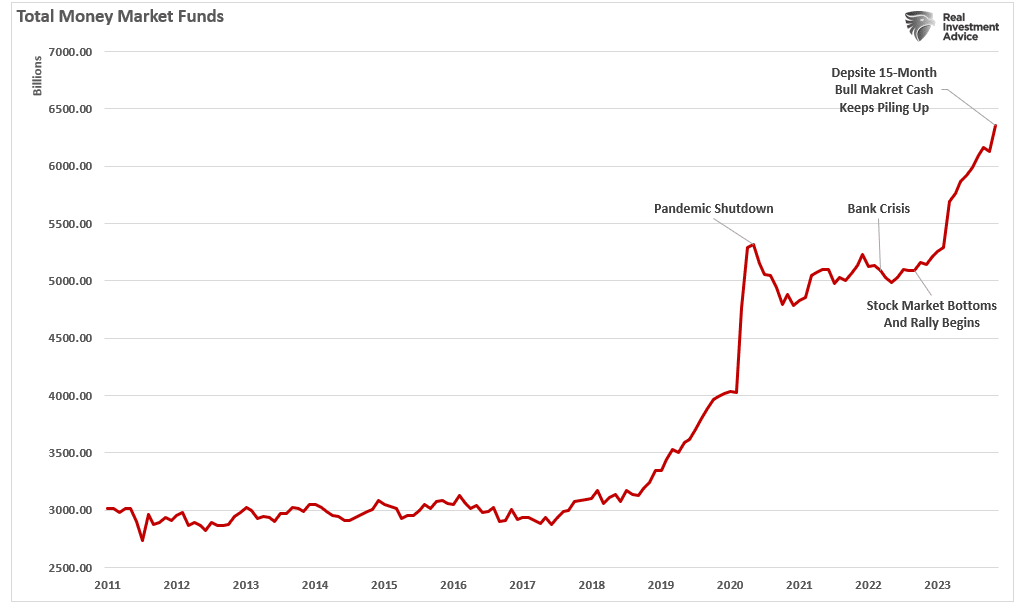

“The growing pile of cash in money market funds should serve as a strong backstop for the stock market in 2024, according to a recent note from Fundstrat’s technical strategist Mark Newton. The allure of 5% interest rates has led to a surge in money market fund assets this year, with total cash on the sidelines recently reaching a record $5.88 trillion. That’s up 24% from last year, when money market funds held $4.73 trillion in cash.

‘While several prominent sentiment polls have turned more optimistic in the last few weeks, this gauge should be a source of comfort to market bulls, meaning that minor pullbacks in the weeks/months to come likely should be buyable given the global liquidity backdrop coupled with ample cash on the sidelines,” Newton said.

The surge in money markets since the “pandemic” has revived the age-old narrative that “money on the sidelines” is set to come into the markets. However, they don’t tell you those funds have accumulated since 1974. Correctly, in the aftermath of crisis events, some of these assets rotate from “safety” to “risk,” but not the degree commentators suggest.

Here is the problem with the “cash on the sidelines” reasoning: it is a complete myth.

The Myth Of Cash On The Sidelines

We have repeatedly discussed this myth, but it is worth repeating, particularly when the financial media begins to push the narrative to garner headlines.

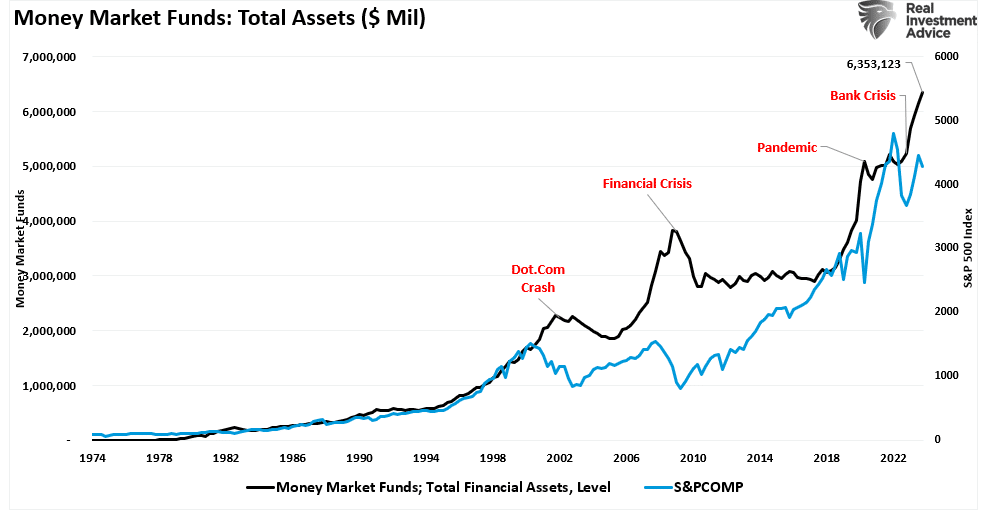

There is a superficial, glib appeal to the idea. After all, lots of people hold money on deposit at the bank, and they could use that money to buy stocks, right? After all, the latest financial data from the Office of Financial Research shows more than $6.3 Trillion sitting in money market accounts.

So what’s to prevent some of that money “coming into the market?”

Simple. The fallacy of composition. This was the point we made previously:

“Every transaction in the market requires both a buyer and a seller, with the only differentiating factor being the transaction’s price. Since this is required for there to be equilibrium in the markets, there can be no “sidelines.”

Think of this dynamic like a football game. Each team must field 11 players despite having over 50 players. If a player comes off the sidelines to replace a player on the field, the player being replaced will join the ranks of the 40 or so other players on the sidelines. At all times, there will only be 11 players per team on the field. This is true if teams expand to 100 or even 1000 players.”

Less Cash Than You Think

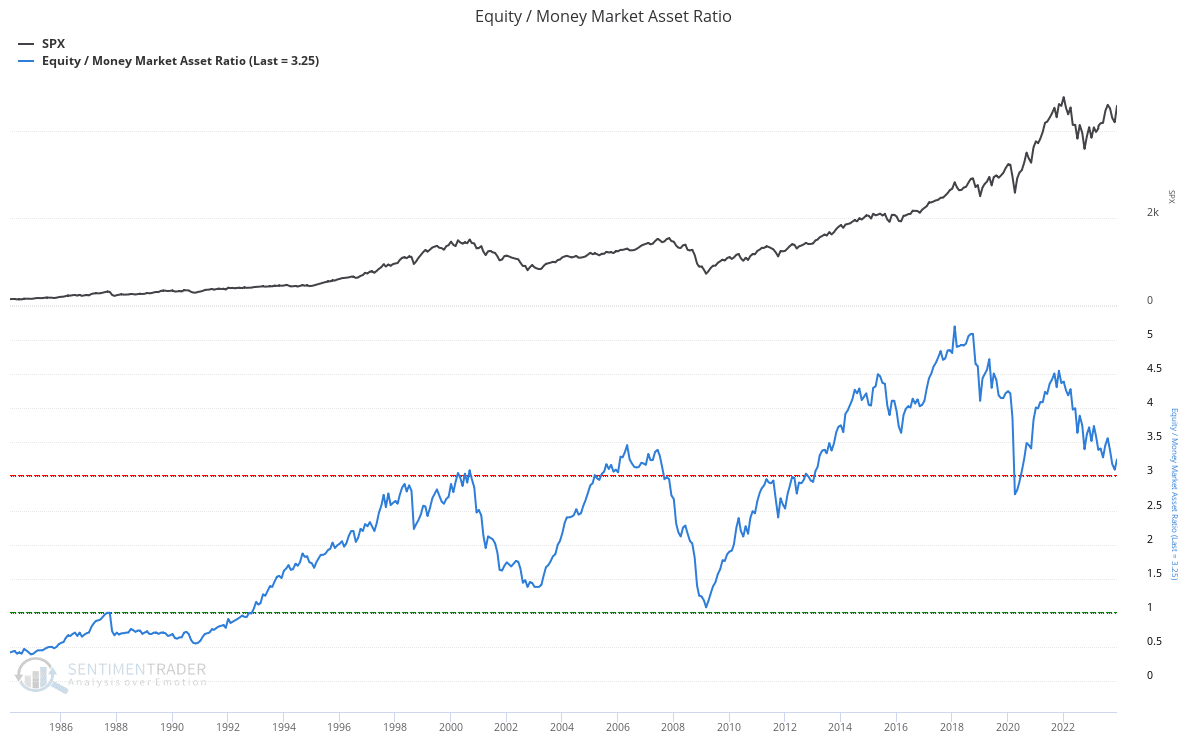

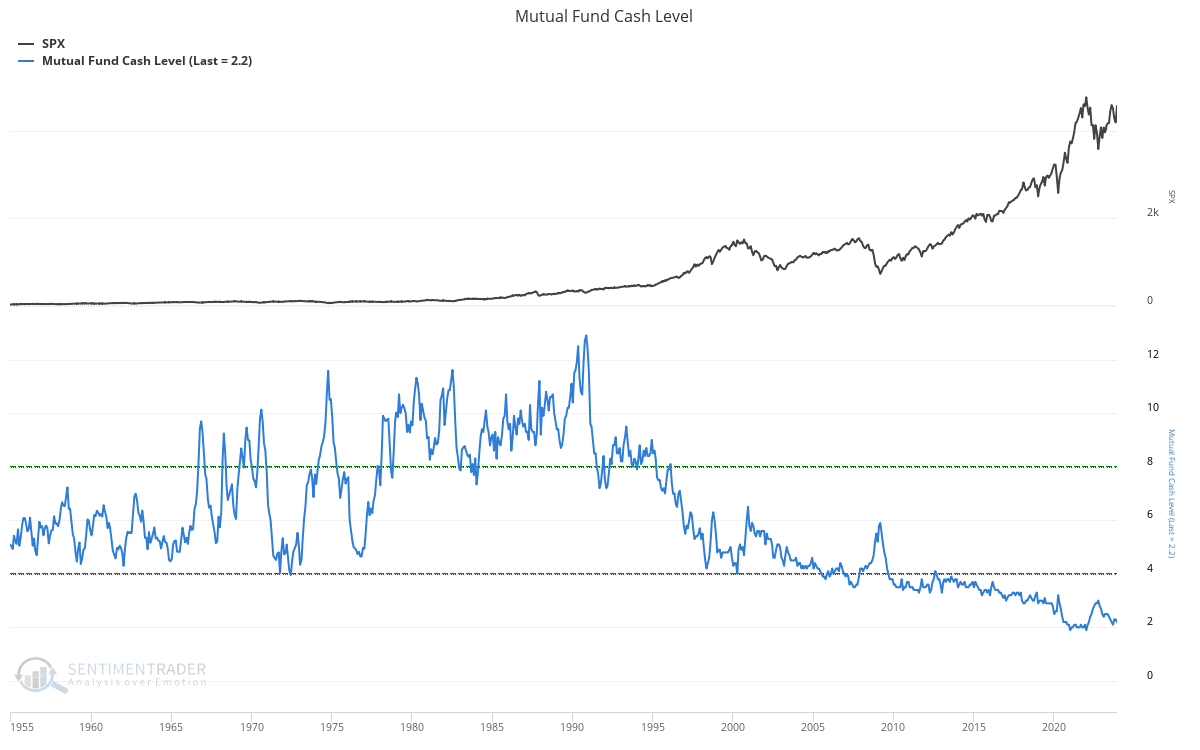

Furthermore, despite this very salient point, looking at the stock-to-cash ratios (cash as a percentage of investment portfolios) also suggests very little buying power for investors. As shown in the chart from Sentimentrader.com, as asset prices have escalated, so have individuals’ appetite to chase risk. The current equity to money market asset ratio, although down from its record, is still above all pre-financial crisis peaks.

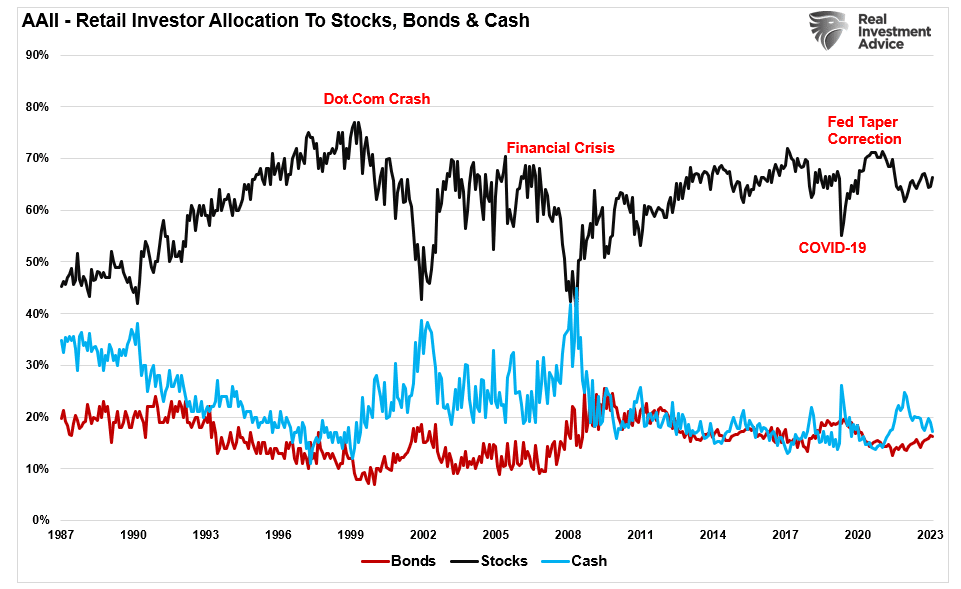

If we look specifically at retail investors, their cash levels have been at the lowest level since 2014 and are not far from record lows. At the same time, equity allocations are not far from the levels in 2007.

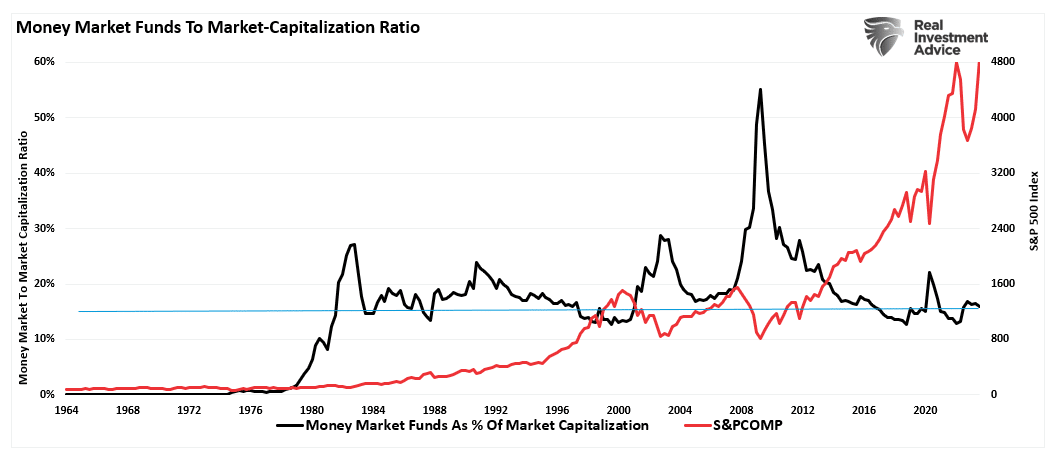

The same is valid with money market levels relative to the market capitalization of the S&P 500 index. The ratio is currently near its lowest since 1980, which suggests that even if the cash did come into the market, it would not move the needle much.

With net exposure to equity risk by individuals at very high levels it suggests two things:

- There is little buying left from individuals to push markets marginally higher, and

- The stock/cash ratio, shown below, is near levels that generally coincide with market peaks.

But it isn’t just individual investors that are “all in,” but professionals as well.

So, if retail and professional investors are already primarily allocated to equity exposure, with very little “cash on the sidelines,” who has all this cash?

So, Where Is All This Cash, Then?

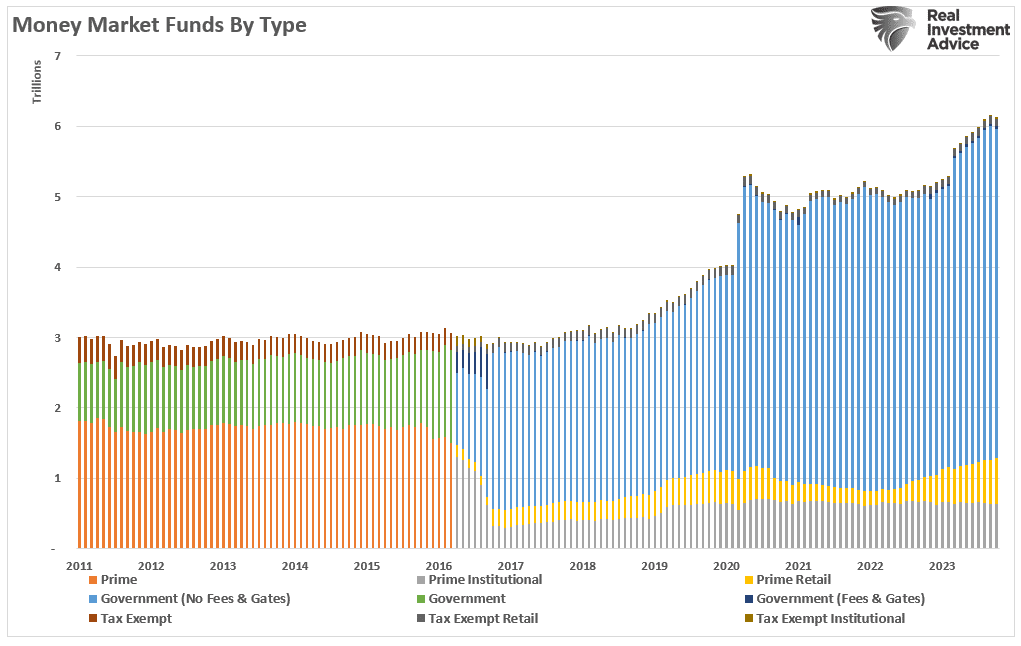

To understand who is holding all the cash currently in money market funds, we can break the Office Of Financial Research data down by category.

There are a few things we need to consider about money market funds.

- Just because I have money in a money market account doesn’t mean I am saving it for investing purposes. It could be an emergency savings account, a down payment for a house, or a vacation fund on which I want to earn a higher interest rate.

- Also, corporations use money markets to store cash for payroll, capital expenditures, operations, and other uses unrelated to investing in the stock market.

- Foreign entities also store cash in the U.S. for transactions processed in the United States, which they may not want to repatriate back into their country of origin immediately.

The list goes on, but you get the idea.

Furthermore, you will notice the bulk of the money is in Government Money Market funds. These particular types of money market funds often have much higher account minimums (from $100,000 to $1 million), suggesting these funds are not retail investors. (Those would be the smaller balances of prime retail funds.)

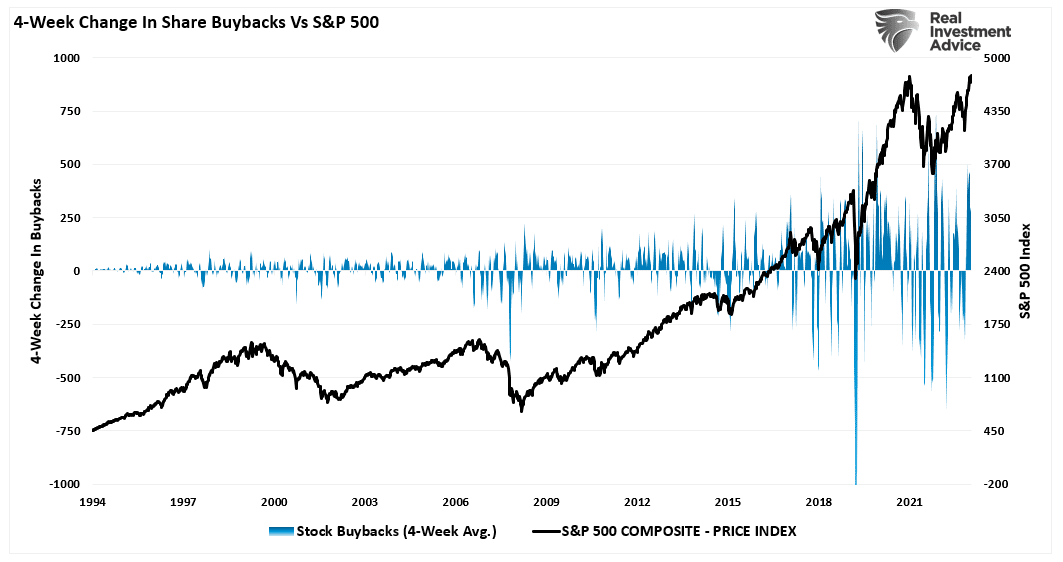

Of course, since the “Great Financial Crisis,” one of the primary uses of corporate “cash on the sidelines” has been for share repurchases to boost earnings. As noted previously, as much as 40% of the bull market since 2012 can be attributed to share buybacks alone.

What Changes The Game

As noted above, the stock market is always a function of buyers and sellers, each negotiating to make a transaction. While there is a buyer for every seller, the question is always at “what price?”

In the current bull market, few people are willing to sell, so buyers must keep bidding up prices to attract a seller to make a transaction. As long as this remains the case and exuberance exceeds logic, buyers will continue to pay higher prices to get into the positions they want to own.

Such is the very definition of the “greater fool” theory.

However, at some point, for whatever reason, this dynamic will change. Buyers will become more scarce as they refuse to pay a higher price. When sellers realize the change, there will be a rush to sell to a diminishing pool of buyers. Eventually, sellers begin to “panic sell” as buyers evaporate and prices plunge.

Sellers live higher. Buyers live lower.

What causes that change? No one knows.

But for now, we need to put the myth of “cash on the sidelines” to rest.

Related: Profit Margins Are Normalizing