Trending

Monday‘s higher stock prices don‘t mean that the sky is the limit now – there were quite a few signs of weakness in related markets as well. The put/call ratio moved lower agains, and so did VIX. But it‘s the market internals that are the giveaway sign – technology has been the predictable upswing driver, reflecting my yesterday‘s thoughts on the rising yields pressure:

(…) One daily move doesn‘t make a trend change likely though, especially since the Mar pace of TLT decline is on par with Feb‘s and higher than in Jan. While Treasuries paused in early Mar, they‘re now once again as extended vs. their 50-day moving average as before.

And that poses a challenge for interest rate sensitive stocks and to some degree also for tech - while I expect value to continue to lead over growth, technology would recover some of the lost ground on rates stabilization. And it‘s true that the $UST10Y move has been a very sharp one, more than tripling from the Aug 2020 lows.

We got that reprieve yesterday, and tech jumped on board enthusiastically, while other usual beneficiaries didn‘t – utilities didn‘t move, but at least consumer staples swung higher. Coupled with the value stocks mostly treading water yesterday, it makes for a weak daily market breadth.

The key events of today and tomorrow are the Congress testimonies – while Powell is set to downplay inflation, inflation expectations and still overall elevated / rising long-dated Treasury yields, it‘s my view that the market is again squaring the bets, best seen in the commodities lately (think Thursday and today) – but I look for the Fed to project the same messaging it did on Wednesday, and perhaps double down on it.

I don‘t view the market as in danger of a deflationary collapse, not when the stimulus avalanche is hitting and the Fed is reluctant to change course. I am not looking for them to telegraphs such a turn today or in the weeks to come, and that would mean recovery in the commodity prices.

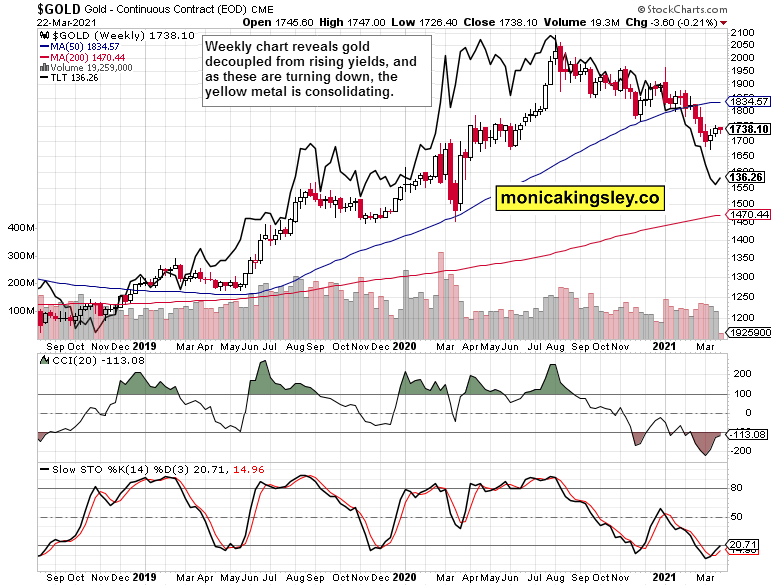

Gold is an island of relative, temporary peace, but the miners are concerningly weakening – both gold and silver ones. Darkening clouds here regardless of the support the copper to 10-year Treasury yields can offer. Still, the yellow metal has decoupled from rising nominal yields to a remarkable degree lately.

Let‘s quote yesterday‘s observations:

(…) As gold is arguably the first asset to move in advance of a key policy move, it might be sensing the Fed being forced (i.e. the markets betting against the Fed) to moderate its accomodative policy. Twist, taper – there are many ways short of raising the Fed funds rate that would help put pressure off the sliding long-dated Treasuries, not that these wouldn‘t be susceptible to move higher from oversold levels. And just like the yellow metal frontrunned the Fed before the repo crisis of autumn 2019, we might be seeing the same dynamic today as well.

For the cynical and clairvoyant ones, we might sit here in 3-6 months over my notes on „the decoupling that wasn‘t“ - all because rates might snap back from the current almost 1.8% on the 10-year bond.

Let‘s move right into the charts (all courtesy of www.stockcharts.com).

S&P 500 Outlook

Both the volume and upper knot are short-term suspect on yesterday‘s S&P 500 upswing – I wouldn‘t be surprised by continued consolidation unless the testimonies today and tomorrow, bring a game changer.

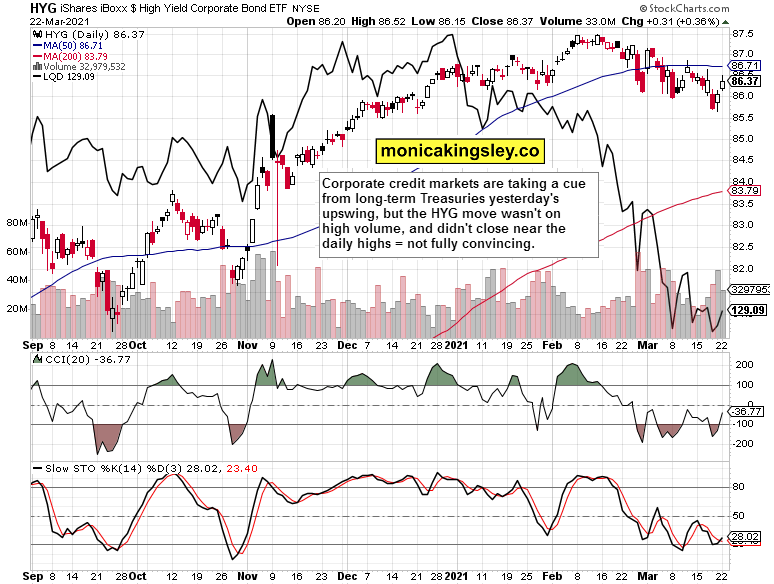

Credit Markets

High yield corporate bonds (HYG ETF), and the volume comparison to preceding day looks here better than in stocks. Still, it can‘t be said the move either in HYG or in investment grade corporate bonds (LQD) was a bullish rush. These two markets merely joined in the long-dated Treasuries recovery, not signalling return of animal spirits.

Technology, Financials and Utilities

Such a sectoral view of rising tech (XLK ETF), for a few sessions weakening financials (XLF ETF) and unconvinced utilities (XLU ETF) isn‘t a bullish constellation to drive the 500-strong index reliably ahead at breakneck speed really.

Gold in the Spotlight

Similarly to Mar 12, the precious metals upswing is being challenged – miners (GDX ETF) are underperforming. Today‘s session will tell whether we‘re witnessing consolidation, or a renewed rollover to the downside, the chances of which have risen yesterday.

The weekly view remains positive – the pace of gold‘s decline became less sensitive to nominal yields move, turning higher before these did, and currently not making much headway. Still, that‘s arguably the clearest sign of the turning tide in the gold market.

Silver, Silver Miners and Copper

Silver is getting under pressure on rising volume, and its miners are declining too, highlighting increasing risks to the white metal. Disregarding today‘s premarket action, that alone makes it worthwhile to dial back (take profits off the table) in the long silver short gold spread I introduced you to on Feb 12. It‘s that the degree of momentary commodities underperformance looks like taking a meaningful toll on the white metal (and that concerns oil as well, which would turn short-term bearish with a breakdown below $57 to $57.50 on a closing basis and on high volume without a prominent lower knot.

Summary

S&P 500 upswing isn‘t as strong as it might seem, and today‘s deceptively small downswing has the potential to turn ugly on Fed missteps. Seeing these happen, I don‘t view as a leading scenario for today or tomorrow, however.

Thank you for having read today‘s free analysis, which is available in full at my homesite. There, you can subscribe to the free Monica‘s Insider Club, which features real-time trade calls and intraday updates for both Stock Trading Signals and Gold Trading Signals.

Related: The Tide Is Turning in Stocks and Gold

The views and opinions expressed in this article are those of the contributor, and do not represent the views of IRIS Media Works and Advisorpedia. Readers should not consider statements made by the contributor as formal recommendations and should consult their financial advisor before making any investment decisions. To read our full disclosure, please click here.