Trending

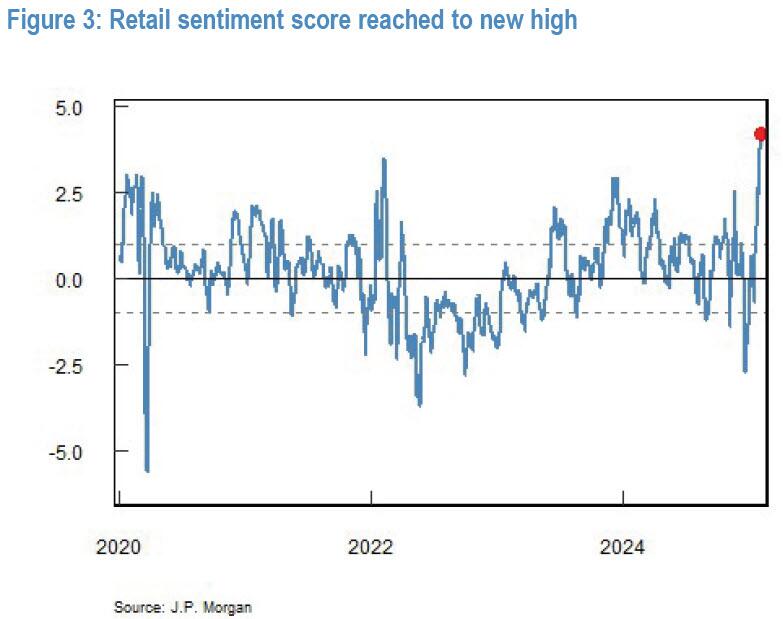

Last week, we discussed the surge in retail exuberance in the market following the election of President Trump.

“The market defies more negative news because retail investors continue to step in and “buy the dip.” In our recent Bull Bear reports, we discussed the push by retail investors, but looking at retail sentiment is quite remarkable. Since the pandemic, retail investors have never been this bullish on the stock market. Such is amazing, given that their mailboxes are not being stuffed with government stimulus checks.”

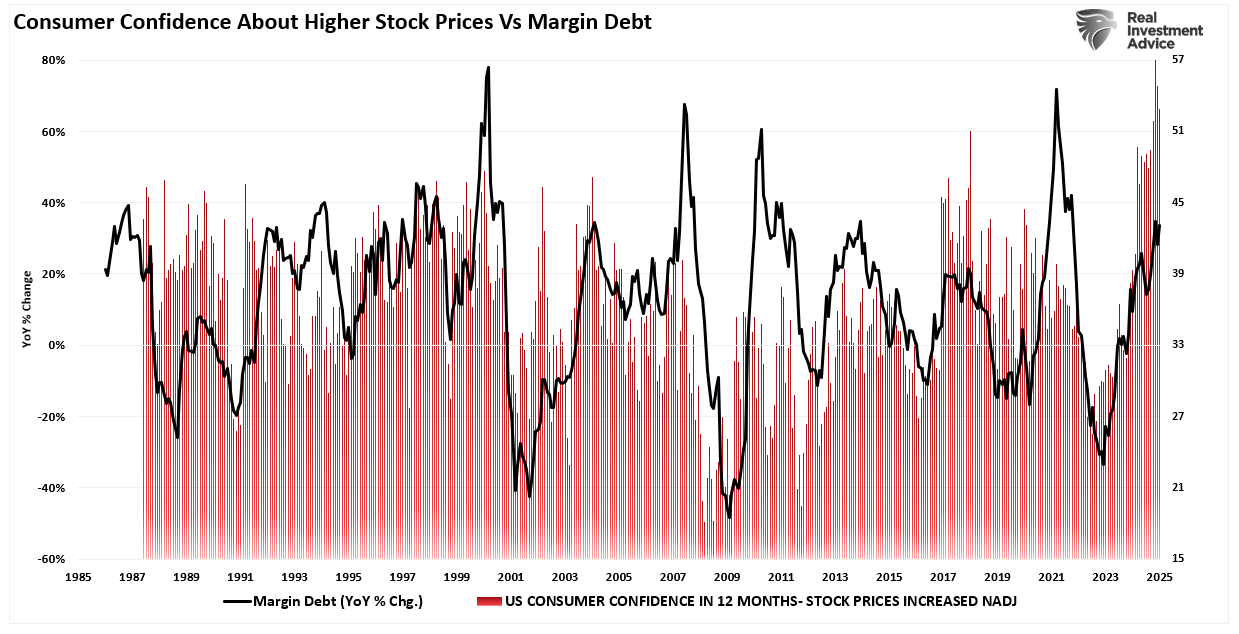

Retail investors are expected to become more bullish about increasing equity exposure when markets rise. However, the more extended markets become, the more confident investors are about increasing speculative risk. In other words, “success breeds confidence.” One way we can view retail exuberance is through the use of leverage. As investors become increasingly confident about higher stock prices in the future, they are willing to borrow money to take on more risk. We see this by comparing investor confidence in higher stock prices to the annual rate of change in margin debt.

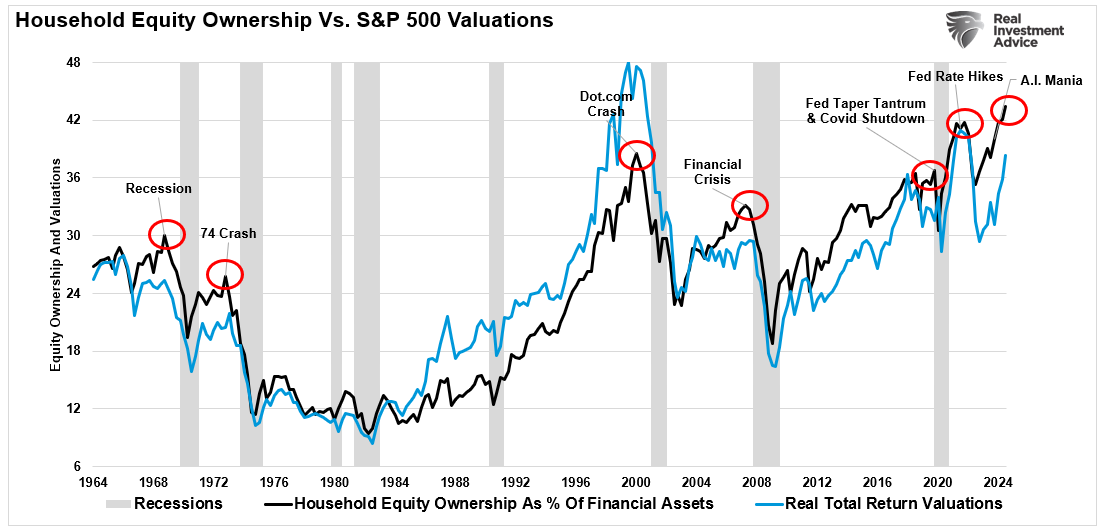

The “Fear Of Missing Out” or “F.O.M.O.” is a compelling motivation for retail investors to chase stocks higher. This is reflected in the current household equity allocations record level, which explains the market’s high valuation levels.

As Howard Marks noted in a December 2020 Bloomberg interview:

“Fear of missing out has taken over from the fear of losing money. If people are risk-tolerant and afraid of being out of the market, they buy aggressively, in which case you can’t find any bargains. That’s where we are now. That’s what the Fed engineered by putting rates at zero…we are back to where we were a year ago—uncertainty, prospective returns that are even lower than they were a year ago, and higher asset prices than a year ago. People are back to having to take on more risk to get return. At Oaktree, we are back to a cautious approach. This is not the kind of environment in which you would be buying with both hands.

The prospective returns are low on everything.”

As shown, Howard was eventually right. In 2022, the decline wiped out all of the previous year’s gains and then some. However, this is a critical point about margin debt and leverage in general.

Margin debt represents the amount of speculation occurring in the market. In other words, margin debt is the “gasoline,” which drives markets higher as the leverage provides for the additional purchasing power of assets. However, leverage also works in reverse, as it supplies the accelerant for more significant declines as lenders “force” the sale of assets to cover credit lines without regard to the borrower’s position.

The last sentence is the most important. The issue with margin debt is that the unwinding of leverage is NOT at the investor’s discretion. That process is at the discretion of the broker-dealers that extended that leverage in the first place. (In other words, if you don’t sell to cover, the broker-dealer will do it for you.) When lenders fear they may not recoup their credit lines, they force the borrower to put in more cash or sell assets to cover the debt. The problem is that “margin calls” generally happen simultaneously, as falling asset prices impact all lenders simultaneously.

Margin debt is NOT an issue – until it is.

So, where are we currently?

Margin Debt Confirms The Exuberance

We have noted recently that retail exuberance is evident as they take on leverage through measures not recorded by broker-dealer margin levels. Whether it is through a surge in options trading or through leveraged ETFs, investors have figured out ways to increase their risk/return profile.

However, when we specifically look at margin debt, a loan against underlying collateral in brokerage accounts, those debt levels have surged to a record. As shown above, the year-over-year rate of change in debt is rising sharply but certainly can go further if retail exuberance continues.

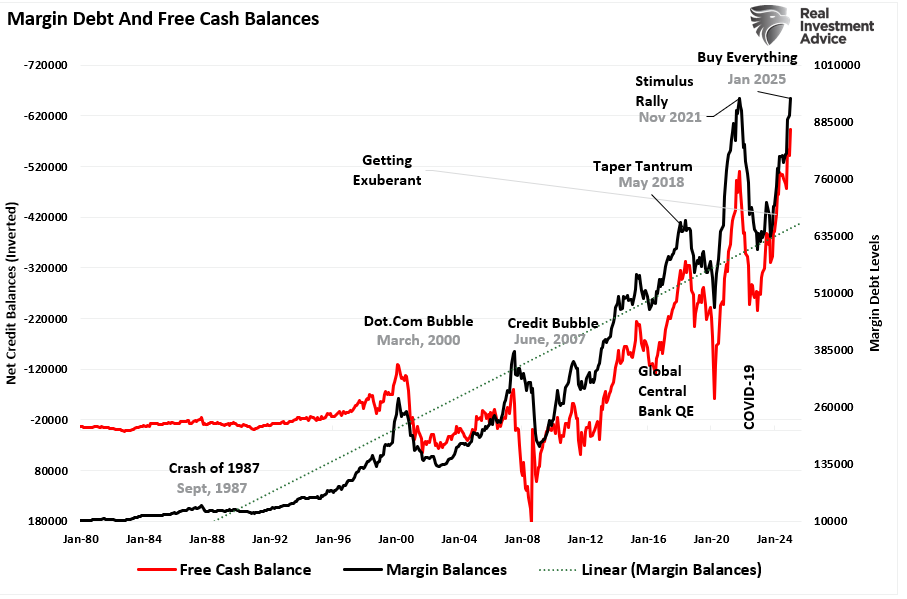

However, look at the red line, “free cash balances.” As noted, margin debt supports the advance when markets rise as investors can leverage additional leverage to increase buying power. Therefore, the recent rise in margin debt is unsurprising as investor exuberance climbs. The chart below shows the relationship between cash balances and the market. I have inverted free cash balances, so the relationship between increases in margin debt and the market is better represented. (Free cash balances are the difference between margin balances less cash and credit balances in margin accounts.).

Note that during the 1987 correction, the 2015-2016 “Brexit/Taper Tantrum,” the 2018 “Rate Hike Mistake,” and the “COVID Dip,” the market never broke its uptrend, AND cash balances never turned positive. Both a break of the rising bullish trend and positive free cash balances were the 2000 and 2008 bear market hallmarks. With negative cash balances at another all-time high, the next downturn could be another “correction.” However, if, or when, the long-term bullish trend is broken, the unwinding of margin debt will add “fuel to the fire.”

As noted, rising leverage is the “fuel” for bull market advances. What makes rising margin debt levels more dangerous is when retail exuberance feeds into all risk assets simultaneously.

All Correlations Go To One

An old saying states that “what goes up must come down.” During speculative market frenzies, investors rush to allocate risk to rising prices. As prices increase, investors become less concerned about underlying risk and begin to rationalize why “this time is different.” However, whatever the rationalization is, prices rise due to one simplistic factor: supply and demand. In the current market, there is just “too much money and leverage, chasing too few assets.”

We have seen that inherent risk play out in previous history. This is particularly the case when correlations between risk assets rise to more extreme levels. For instance, as shown, the correlation between the S&P 500 index and emerging and international markets is near one. (1.00 is a perfectly positive correlation, and -1.00 is a perfectly negative non-correlation.)

There are many narratives surrounding Bitcoin and cryptocurrencies in general. However, due to its price volatility, Bitcoin has been an effective “leveraged” bet on rising asset markets.

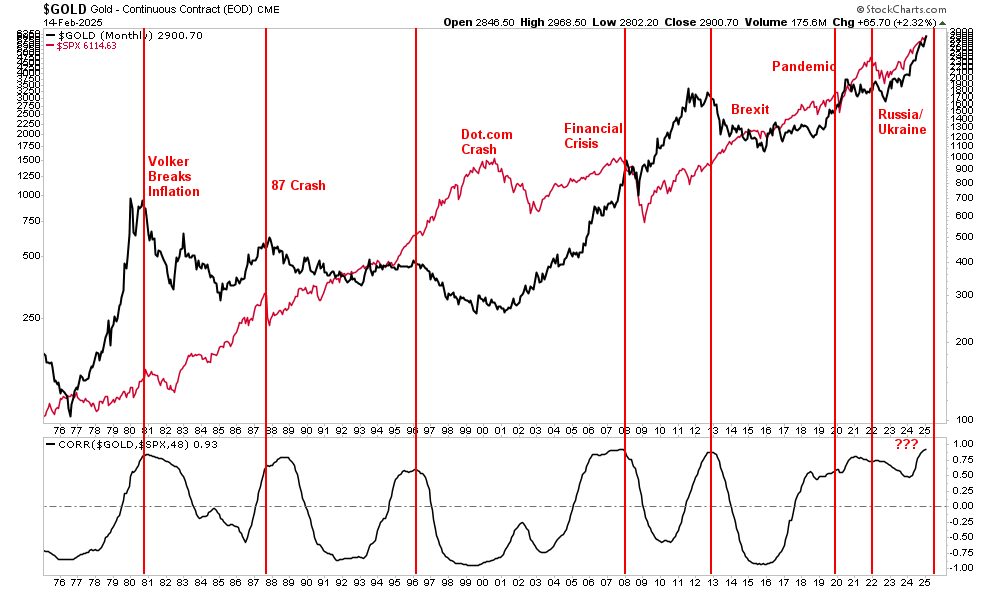

Interestingly, gold, while often considered a hedge for inflation, has also seen a sharp increase in its correlation to equity prices. Historically, when the correlation of gold to the S&P 500 index reaches 1.00, such has been a peak in gold prices. However, except for the late 90s, the peak correlation between gold and the S&P 500 was also near the peaks of financial markets. Such is because the speculative frenzy to chase all assets simultaneously undermined the value of portfolio diversification. As such, when markets eventually cracked, and leverage was unwound, all assets were sold simultaneously.

Conclusion

While the immediate response to this analysis will be, “But Lance, margin debt is only slightly higher than in 2021,” there are many differences between then and today. The lack of stimulus payments, zero interest rates, and $120 billion in monthly “Quantitative Easing” are just a few. However, some glaring similarities exist, including the surge in negative cash balances and extreme deviations from long-term means.

Does this mean the markets are about to suffer a significant mean reverting event? No.

It suggests only that with leverage elevated, correlations across asset classes are high, and bullish sentiment is rampant. The ingredients of a reversion are undoubtedly present, but the catalyst is absent.

In the short term, exuberance is infectious. The more the market rallies, the more risk investors want to take on. The issue with margin debt is that when an event eventually occurs, it creates a rush to liquidate holdings. Since margin debt is a function of the value of the underlying “collateral,” the forced sale of assets will reduce the value of the collateral. The decline in value then triggers further margin calls, triggering more selling, forcing more margin calls, and so forth.

Margin debt levels, like valuations, are not helpful as a market-timing device. However, they are a valuable indicator of market exuberance.

While it may “feel” like the market “just won’t go down,” it is worth remembering Warren Buffett’s sage words.

“The market is a lot like sex, it feels best at the end.”

Currently, the market feels exceptionally good.

Related: Why Tariffs Aren't as Bearish as Expected: A Surprising Outlook