Trending

Written By: David Trainer In recent weeks, we’ve shown how investors who use traditional valuation metrics like price-to-book and price-to-earnings are led to buy low-quality, overvalued stocks. These aren’t the only problematic metrics though. EBITDA, and its more troublesome derivative, adjusted EBITDA, can be even more damaging to an investor’s search for quality stocks.Both of these companies highlight their adjusted EBITDA growth to investors and tie executive compensation to the metric. However, their economic earnings , the true cash flows of the business, reveal growing losses. Teladoc Health (TDOC) and Integer Holdings () are in the Danger Zone .

Why Adjusted EBITDA Cannot Be Trusted

The problems with EBITDA stem from its starting point, accounting earnings, which fail to capture the true profitability of a firm. EBITDA then ignores the real cost of capital needed to maintain a business through its removal of depreciation and amortization.Even worse, the calculation of adjusted EBITDA is often left entirely up to management, i.e. the same people whose bonuses are tied to adjusted EBITDA targets. Wouldn’t it be nice to pick and choose what gets included and excluded in your own performance measurement? We’ve outlined even more issues with adjusted EBITDA here.Teladoc Health ( TDOC )

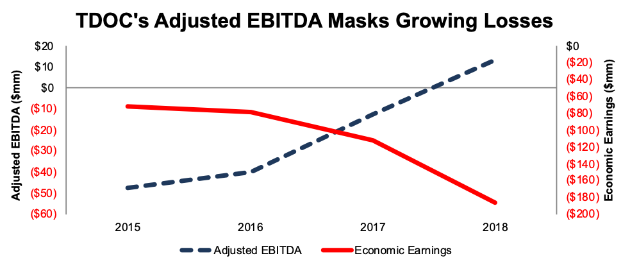

Teladoc, a virtual healthcare service provider, boasts impressive revenue growth and reported its first year of positive adjusted EBITDA in 2018. However, when we perform real diligence to get at the true profitability of the firm, we find the situation isn’t as rosy as management would have investors believe.TDOC’s adjusted EBITDA has grown from -$47 million in 2015 to $13 million in 2018. Economic earnings have fallen from -$72 million to -$186 million over the same time. See Figure 1. Figure 1: TDOC’s Misleading Adjusted EBITDA Image Source: New Constructs, LLCSources: New Constructs, LLC and company filings.Given the company’s rapidly declining economic earnings, it should come as no surprise that TDOC would rather investors focus on adjusted EBITDA. In its 4Q18 press release, TDOC noted, “We utilize Adjusted EBITDA as the primary measure of our performance,” which highlights the importance management places on this metric.However, by placing heavy emphasis on such a flawed metric, management is (1) ignoring real costs of doing business when presenting its results and (2) giving investors an incomplete picture of the company’s financials. Here are just a few of the items TDOC removes when calculating adjusted EBITDA:

Image Source: New Constructs, LLCSources: New Constructs, LLC and company filings.Given the company’s rapidly declining economic earnings, it should come as no surprise that TDOC would rather investors focus on adjusted EBITDA. In its 4Q18 press release, TDOC noted, “We utilize Adjusted EBITDA as the primary measure of our performance,” which highlights the importance management places on this metric.However, by placing heavy emphasis on such a flawed metric, management is (1) ignoring real costs of doing business when presenting its results and (2) giving investors an incomplete picture of the company’s financials. Here are just a few of the items TDOC removes when calculating adjusted EBITDA:Exec Comp Plan Only Compounds the Issues

The discretion taken to remove real expenses when calculating adjusted EBITDA is bad enough by itself, but it’s made worse when one considers (1) management’s recognition of the failings of adjusted EBITDA, and (2) TDOC’s executive compensation plan is tied to adjusted EBITDA targets.In its earnings press release, TDOC outlines the shortcomings of its adjusted EBITDA metric. Some of the limitations the company lists are:Shares Are Significantly Overvalued Given the True Profitability of the Firm

We believe that that the 22% increase in TDOC’s stock price since the beginning of the year has been driven by noise traders fooled by the company’s positive adjusted EBITDA. When we remove the accounting distortions and look at the expectations implied by the stock price, TDOC appears significantly overvalued.To justify its current price of $60/share, TDOC must achieve an 8% NOPAT margin (double the average of its peer group currently under coverage, compared to -15% in 2018) and grow revenue by 30% compounded annually for the next 13 years. See the math behind this dynamic DCF scenario. For reference, P&S Market Research, an industry research provider, estimates the entire telemedicine market will grow by 15% compounded annually over the next five years. In other words, TDOC must immediately and drastically improve margins and grow at double the industry rate for over a decade to justify its current share price.Even if TDOC can cut marketing and other costs enough to achieve an 8% NOPAT margin and grow NOPAT by 20% compounded annually (still above industry expectations) for the next decade, the stock is worth just $11/share today – an 82% downside. See the math behind this dynamic DCF scenario.Integer Holdings Corp ( ITGR )

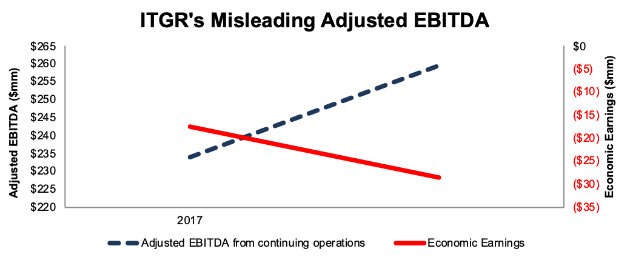

Integer Holdings, a medical device manufacturer, reports rising adjusted EBITDA and looks undervalued by traditional metrics. However, as with TDOC above, economic earnings tell a different storyIn 2018, ITGR’s adjusted EBITDA grew by 11% year-over-year (YoY) while economic earnings fell from -$29 million to -$57 million, per Figure 2. Figure 2: ITGR’s Adjusted EBITDA Rises While Economic Earnings Fall Image Source: New Constructs, LLCSources: New Constructs, LLC and company filings.When calculating its adjusted EBITDA, ITGR removes many common items, such as stock-based compensation ($10 million in 2018 – 6% of GAAP net income) and acquisition and integration expenses (none in 2018, $11 million in 2017). In addition, the company removes some more unique items:

Image Source: New Constructs, LLCSources: New Constructs, LLC and company filings.When calculating its adjusted EBITDA, ITGR removes many common items, such as stock-based compensation ($10 million in 2018 – 6% of GAAP net income) and acquisition and integration expenses (none in 2018, $11 million in 2017). In addition, the company removes some more unique items:Exec Comp Plan Incentivizes Poor Capital Allocation

Executives at ITGR have 75% of their annual performance based incentives tied to adjusted EBITDA and 25% tied to revenue. As with TDOC above, ITGR’s management team is incentivized to grow revenue, and through the heavy use of adjusted EBITDA, can remove the costs of achieving or acquiring that revenue growth.Instead of incentivizing executives with a metric that is directly correlated with creating shareholder value, such as return on invested capital ( ROIC), ITGR chooses to use metrics that predominantly mislead investors and enrich executives.Significant Downside Risk in Owning ITGR

ITGR has outperformed the market over the past two years (+50% vs. S&P +2%). However, because 2018 earnings were inflated due to $121 million in income from discontinued operations, and management reported growing adjusted EBITDA, those using flawed traditional valuation metricswould believe ITGR is still a value.At its current price of $86/share, ITGR has a price-to-earnings (P/E) ratio of 16.7, well below the overall Healthcare industry average of 38.6 and the S&P 500 average of 20.1. ITGR also has an enterprise value to EBITDA (EV/EBITDA) ratio of 15.3, which is well below the market cap weighted average of 22.8 for the 99 Healthcare Equipment & Supplies firms under coverage. We’ve covered the shortcomings of EV/EBITDA here.ITGR may look cheap by traditional metrics, but when we analyze the cash flow expectations baked into the stock price, we see that ITGR is significantly overvalued.To justify its current price of $86/share, ITGR must maintain its 2018 NOPAT margin of 11% (highest in the company’s history) and grow NOPAT by 10% compounded annually for the next 12 years. See the math behind this dynamic DCF scenario. Such a scenario implies ITGR can grow revenue by more than double consensus expectations (5% in both 2019 and 2020). Furthermore, since acquiring Lake Region Medical Holdings in late 2015, the company has grown NOPAT by just 5% compounded annually .Even if ITGR can maintain current NOPAT margins (11%) and grow NOPAT by 5% compounded annually for the next decade, the stock is worth just $39/share today – a 55% downside. See the math behind this dynamic DCF scenario.Relying on Adjusted EBITDA Has a History of Ending Badly

Many of our most successful Danger Zone picks use or have used adjusted EBITDA as a performance metric in executive compensation. See Figure 3. Figure 3: Successful Danger Zone Picks Relying on Adjusted EBITDA Image Source: New Constructs, LLCSources: New Constructs, LLC and company filings.These firms can report misleading adjusted EBITDA only for so long. Eventually, the real economics of the business catch up.There is good news though. Investors no longer have to settle for flawed valuation and profitability metrics. Our machine learning and Robo-Analyst technology [1] helps investors get the best fundamental research [2] that Wall Street insiders use. Our technology enables us to deliver fundamental diligence at a previously impossible scale. We believe this research is necessary to uncover the true profitability of a firm and make sound investment decisions. [1] Harvard Business School features the powerful impact of our research automation technology in the case study New Constructs: Disrupting Fundamental Analysis with Robo-Analysts. [2] Ernst & Young’s recent white paper, “ Getting ROIC Right”, proves the superiority of our holdings research and analytics.

Image Source: New Constructs, LLCSources: New Constructs, LLC and company filings.These firms can report misleading adjusted EBITDA only for so long. Eventually, the real economics of the business catch up.There is good news though. Investors no longer have to settle for flawed valuation and profitability metrics. Our machine learning and Robo-Analyst technology [1] helps investors get the best fundamental research [2] that Wall Street insiders use. Our technology enables us to deliver fundamental diligence at a previously impossible scale. We believe this research is necessary to uncover the true profitability of a firm and make sound investment decisions. [1] Harvard Business School features the powerful impact of our research automation technology in the case study New Constructs: Disrupting Fundamental Analysis with Robo-Analysts. [2] Ernst & Young’s recent white paper, “ Getting ROIC Right”, proves the superiority of our holdings research and analytics.