Trending

Understanding the trajectory of corporate earnings is crucial for investors, as these earnings significantly influence stock valuations and market performance. Economic indicators such as Gross Domestic Product (GDP), the Institute for Supply Management (ISM) Manufacturing Index, and the Chicago Fed National Activity Index (CFNAI) provide valuable insights into the economic environment that shapes company profitability. These indicators can also help investors evaluate whether Wall Street’s earnings estimates are realistic.

During raging bull markets, exuberance about the market can detach from the underlying economic fundamentals. During these periods, it is not uncommon for Wall Street analysts to continually increase forward estimates on the hopes that the economy will catch up to reality. However, there is a symbiotic relationship between economic indicators and the trajectory of earnings that we will explore.

Let’s start with the economy itself.

Gross Domestic Product (GDP)

GDP measures the total value of goods and services produced within a country. It is a reliable gauge of overall economic health. A growing GDP indicates increased economic activity, typically driving higher corporate earnings due to greater consumer spending and business investment. Conversely, a contracting GDP suggests an economic slowdown, often dampening corporate profits.

That data supports this concept. Historically, GDP growth has closely correlated with corporate earnings growth. Data from the Federal Reserve shows that, since 1948, a 1% increase in real GDP growth has translated to roughly a 6% increase in S&P 500 earnings on average. This relationship underscores why GDP is a cornerstone for assessing earnings trends. We can also see this visually.

“Since 1947, earnings per share have grown at 7.7% annually, while the economy expanded by 6.40% annually. That close relationship in growth rates should be logical, particularly given the significant role that consumer spending has in the GDP equation.” – Market Forecasts Are Very Bullish

A better way to visualize this data is to look at the correlation between the annual change in earnings growth and inflation-adjusted GDP. There are periods when earnings deviate from underlying economic activity. However, those periods are due to pre- or post-recession earnings fluctuations. Currently, economic and earnings growth are very close to the long-term correlation.

However, as we discussed previously, there is also a high correlation between the market and the corporate profits to GDP ratio. As is the case currently, markets can detach from underlying economic realities due to momentum and psychology for brief periods. However, those deviations are unsustainable in the long term, and corporate profitability, as discussed, is derived from underlying economic activity.

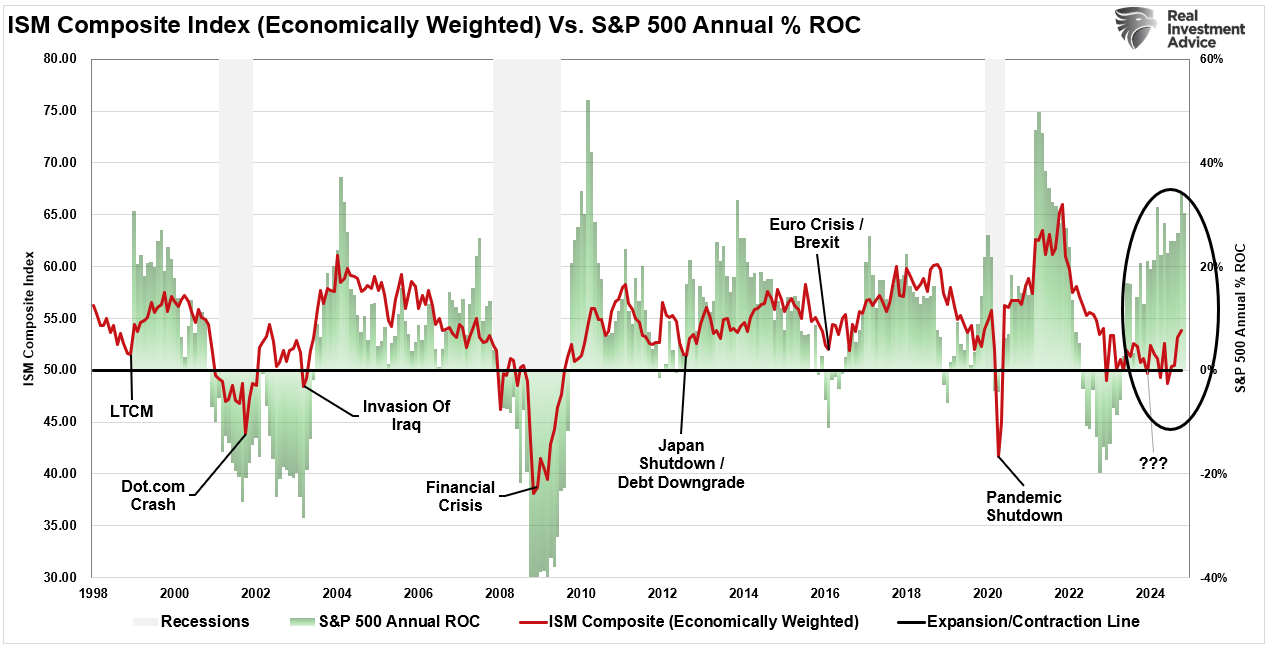

The ISM Composite Index can also give us clues as to where earnings will likely be in 2025.

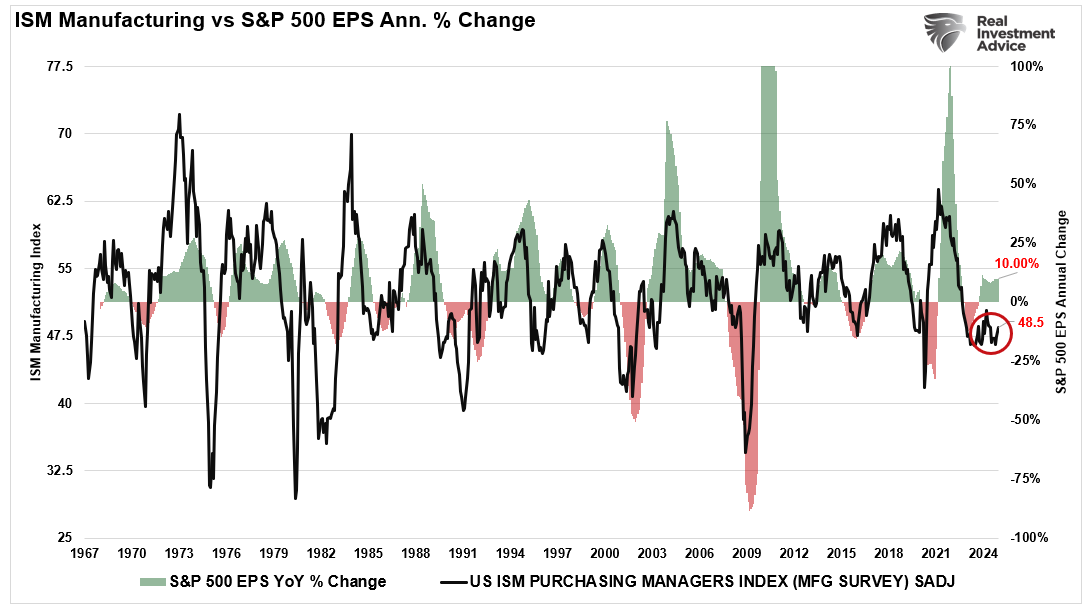

ISM Manufacturing Index

The ISM Manufacturing Index is a widely followed leading indicator of economic activity in the manufacturing sector. It surveys purchasing managers on critical metrics like new orders, production levels, and employment.

- A reading above 50 signals expansion, which tends to support earnings growth.

- A reading below 50 suggests contraction, often foreshadowing economic weakness and declining corporate profits.

As of late 2024, the ISM Manufacturing Index has been consistently below 50, marking a manufacturing recession. This data aligns with declining new orders and softer demand, raising concerns about corporate earnings resilience in 2025. However, while manufacturing only accounts for about 20% of U.S. GDP, it has a outsized influence that extends across supply chains, amplifying the impact on broader economic activity.

As shown, corporate earnings growth, which correlates with economic indicators like the ISM Manufacturing index, suggests some caution in the more optimistic Wall Street estimates. However, even if we include the services side of the index, which comprises the bulk of economic growth, and weight it accordingly, we see that the stock market has far outpaced underlying economic activity. Historically, such outsized returns were unsustainable as earnings growth could not meet expectations.

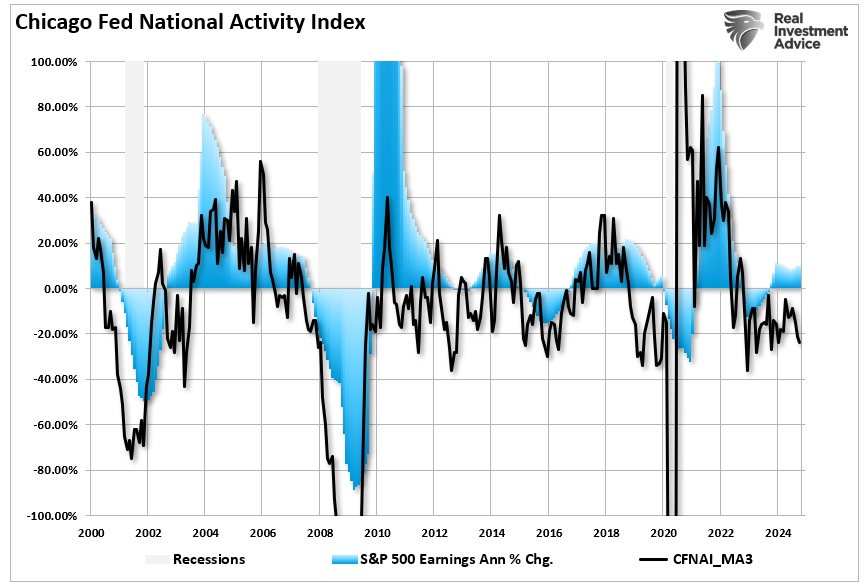

However, one of the better economic indicators to pay attention to is the Chicago Fed National Activity Index, which is a very broad measure of the economy but does not receive much attention.

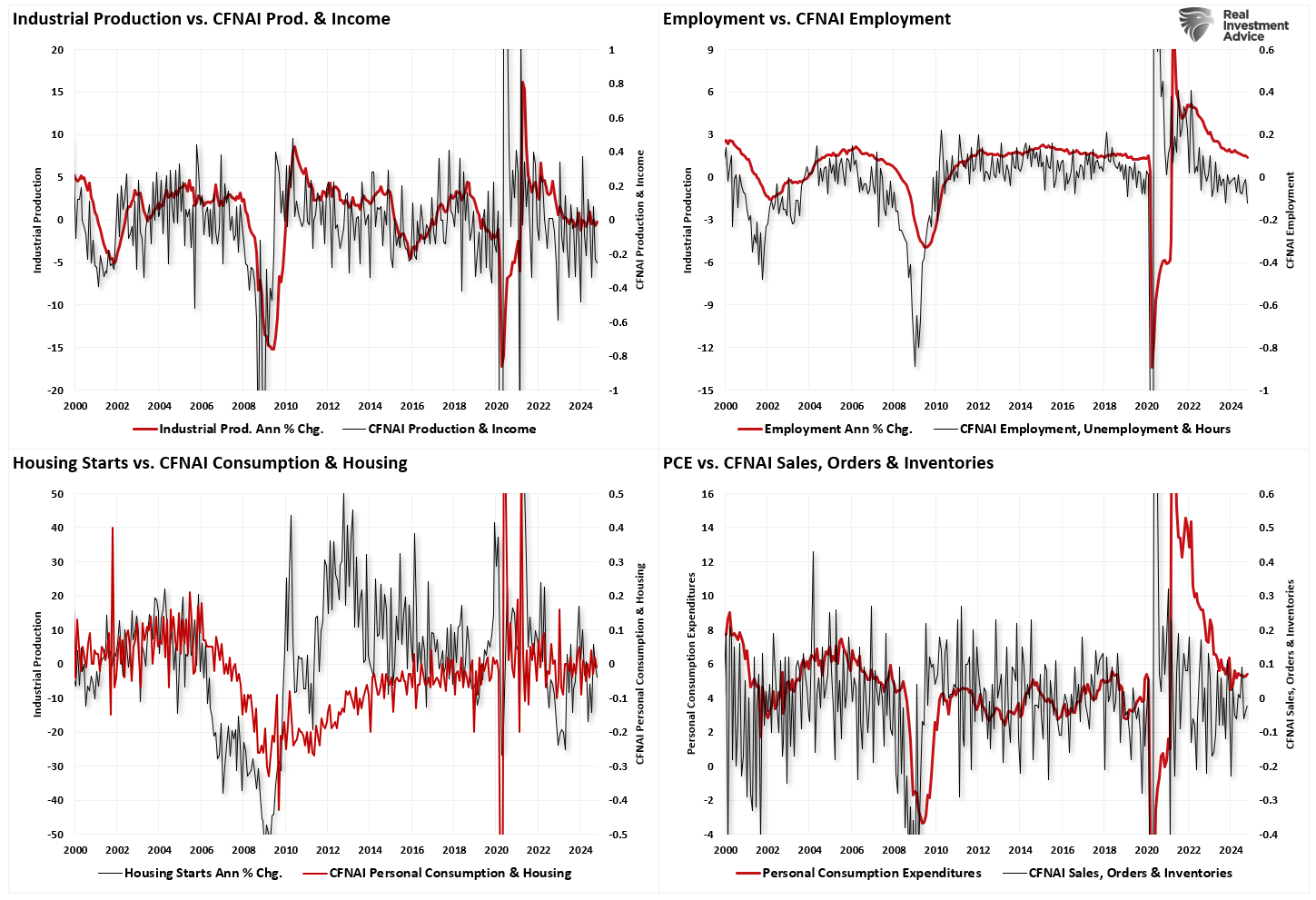

Chicago Fed National Activity Index (CFNAI)

The CFNAI aggregates 85 monthly economic indicators from four categories:

- Production and income.

- Employment, unemployment, and hours worked.

- Personal consumption and housing.

- Sales, orders, and inventories.

A CFNAI reading above zero indicates above-trend economic growth, while below zero suggests below-trend growth. In October 2024, the CFNAI registered at -0.15, reflecting subdued economic activity. Prolonged readings in negative territory often signal a rising risk of recession. Notably, the employment measure suggests that the annual rate of change in employment will continue to decline, industrial production will slow, and personal consumption will moderate lower.

The CFNAI’s broad scope provides a nuanced view of how various economic forces combine to affect corporate earnings. With production and employment metrics deteriorating, the outlook for robust earnings in 2025 appears increasingly strained. As shown, a high but volatile historical correlation exists between the CFNAI and corporate earnings.

While these are the major indicators to pay attention to heading into 2025, there are others.

- Consumer Spending: This accounts for nearly 70% of U.S. GDP. Recent data shows retail sales growth has slowed, indicating cautious consumer behavior amid inflationary pressures and higher interest rates. Lower spending reduces revenue prospects for consumer-focused companies.

- Labor Market Trends: While the unemployment rate remains low, job openings and wage growth are moderating. A weakening labor market could hinder disposable income growth, further challenging consumer-driven earnings.

- Corporate Margins: Rising costs for raw materials, labor, and borrowing are compressing profit margins. If these trends persist, corporate earnings in 2025 could be weaker than anticipated.

Wall Street Earnings Estimates for 2025

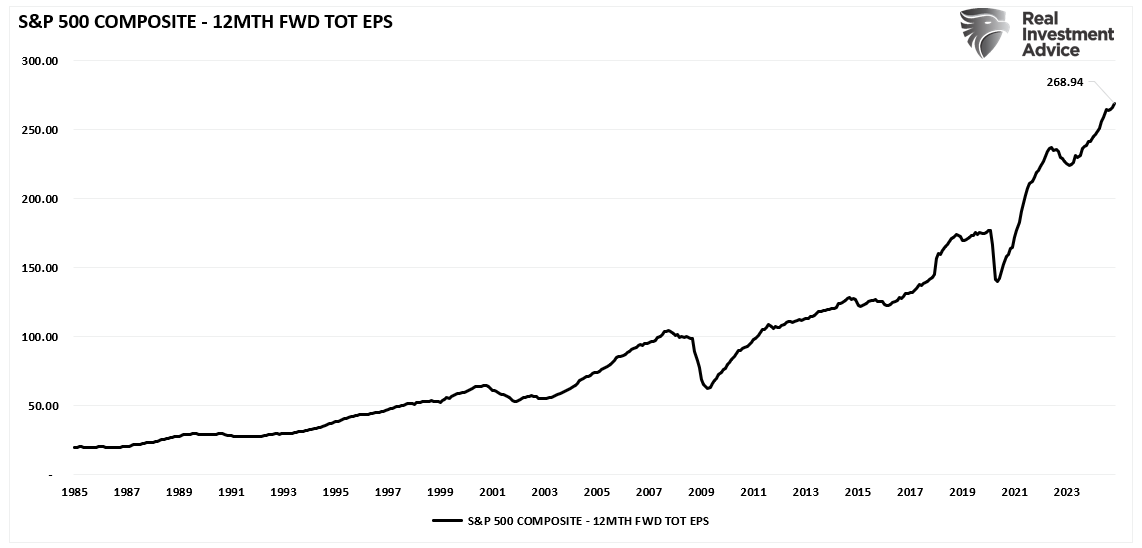

Currently, Wall Street analysts project record corporate earnings for 2025. The bottom-up earnings-per-share (EPS) estimate for the S&P 500 stands at $268.94, reflecting an annual growth of over 10%. If realized, this would mark the highest EPS in history.

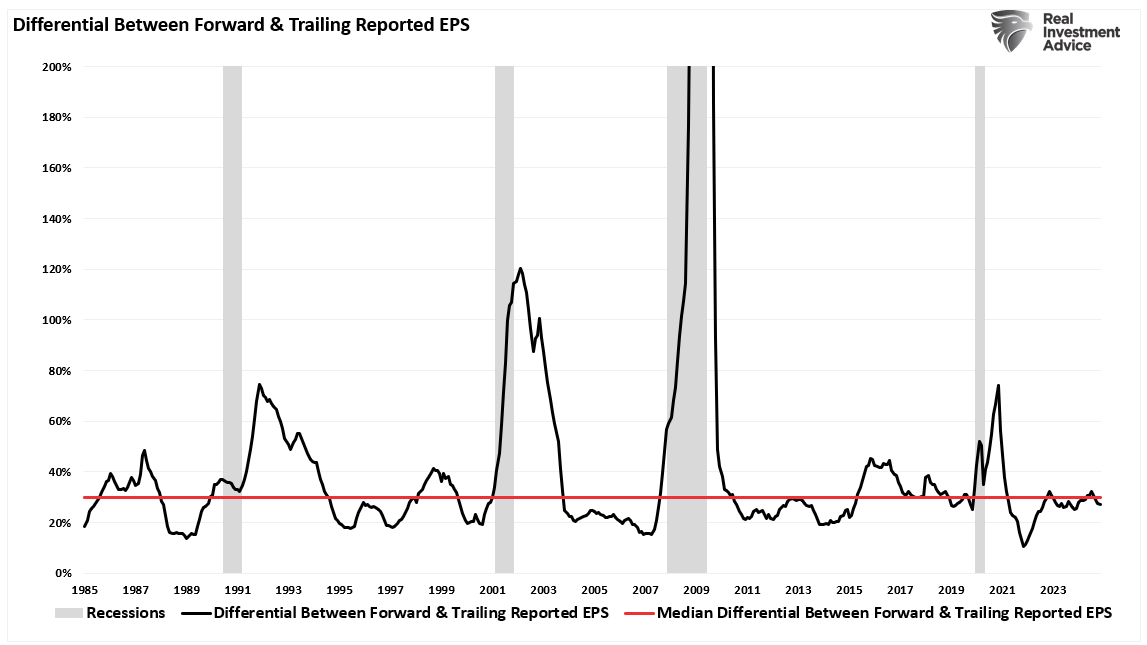

However, historical patterns suggest caution: analysts tend to overestimate earnings by roughly 30% (the median) one year in advance. With economic data signaling a slowdown, these estimates may be overly optimistic. Current trends in leading indicators like ISM Manufacturing and CFNAI support a more conservative outlook.

One key risk lies in valuation metrics. The S&P 500 trades at approximately 22.43 times forward earnings, well above the historical average of 15.8 times. If earnings fall short of estimates, stocks could face downward pressure as investors reassess valuations.

Based on current economic data, it seems likely that Wall Street’s earnings estimates for 2025 are higher than expected. Subdued manufacturing activity, slowing GDP growth, and cautious consumer behavior all point to an economic environment less supportive of aggressive earnings growth. As such, investors must carefully navigate the disconnect between high Wall Street expectations and softening economic conditions. Here are some strategies to consider:

- Diversification: Spread investments across sectors to mitigate risks tied to specific industries, particularly those heavily reliant on consumer spending or manufacturing.

- Focus on Quality: Prioritize companies with strong balance sheets, consistent cash flows, and defensible market positions. Quality companies tend to weather economic slowdowns better than their peers.

- Monitor Leading Indicators: To anticipate earnings revisions, pay close attention to ISM Manufacturing, CFNAI, and consumer spending trends.

- Prepare for Volatility: Elevated valuations leave little margin for error. If earnings fall short of expectations, expect heightened market volatility.

If these headwinds persist, corporate earnings may grow much slower or even contract slightly compared to Wall Street’s current projections. For investors, this scenario could mean lower returns from equities, particularly in high-growth sectors more sensitive to earnings disappointments.

We will continue to monitor these data points, as well as credit spreads, for increases in market risks. However, bullish optimism and extreme consumer confidence in high stock prices dominate market dynamics. While that can remain the case for much longer than logic suggests, that complacency will eventually give way to economic fundamentals.

While we cannot consistently effectively “time the market” over long periods of time, we can manage portfolio risk by paying attention to what drives markets. Sentiment, credit spreads, earnings, and real-time economic data will provide the clues needed to navigate the markets effectively.

Related: CPI Delivers as Expected: A Green Light for the Fed