Trending

Once again, due to the ongoing lack of fiscal responsibility in Washington, the markets and the economy faced a Government shutdown. After a day of theatrics, Congress passed a “stopgap” measure that will keep the Government operating for 45 days. But is that a good thing?

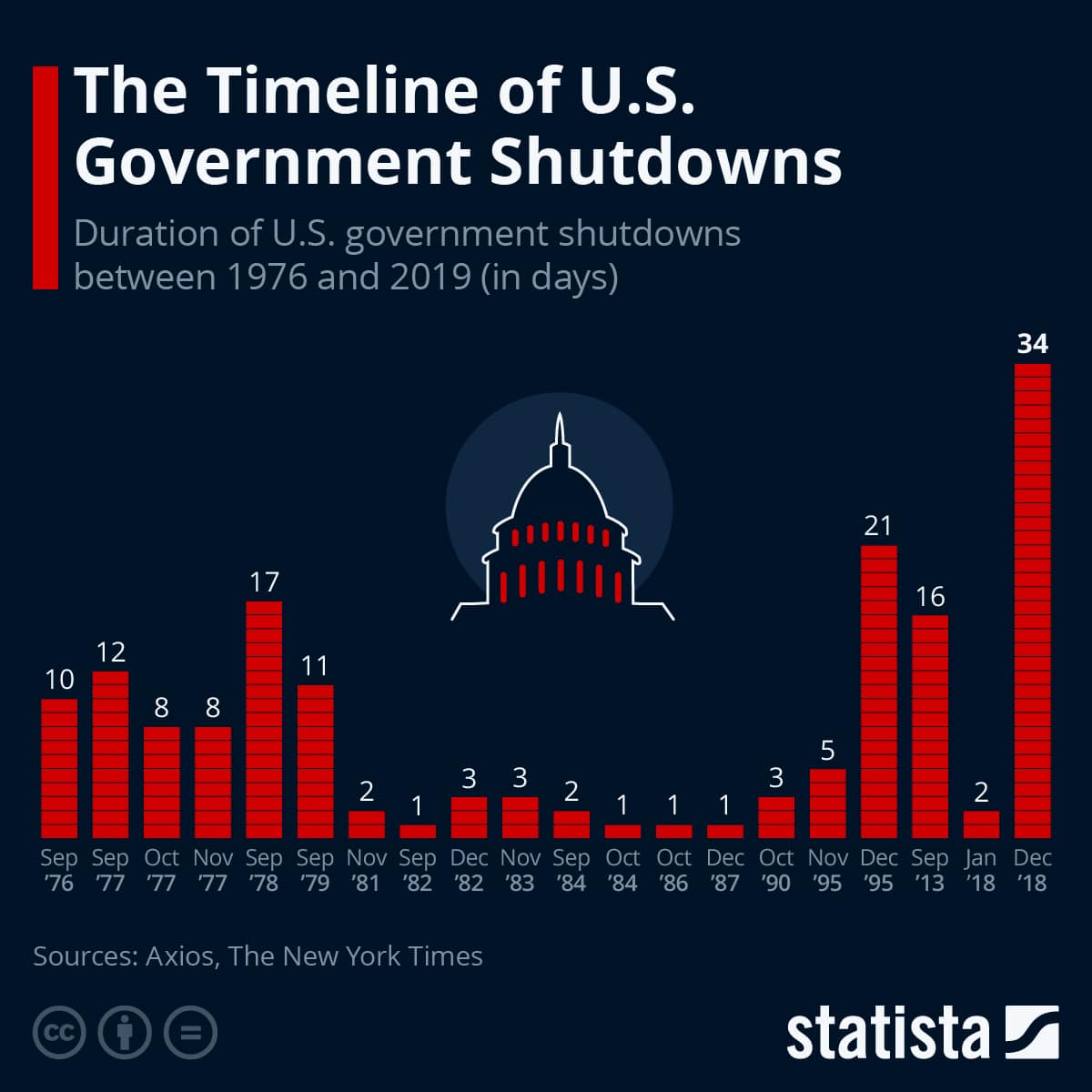

First of all, while much media hyperbole surrounds Government shutdowns, much like the debt ceiling, there is a long history of shutdowns going back to the 70s. As Katherine Buchholz of Statista recently penned:

“The 2018/19 Government shutdown was the longest in recent U.S. history at 34 days. A timeline shows that government shutdowns have been getting longer in the last three decades, with the second and the fourth-longest Government shutdowns taking place in 1995 and 2013, respectively. Throughout the 1980s, shutdowns were numerous but shorter, while in the 1970s, they also ran somewhat longer but only surpassed two weeks once, in 1978. Government shutdowns aren’t all that rare: Since 1976, there have been 20 shutdowns that lasted an average of 8 days.“

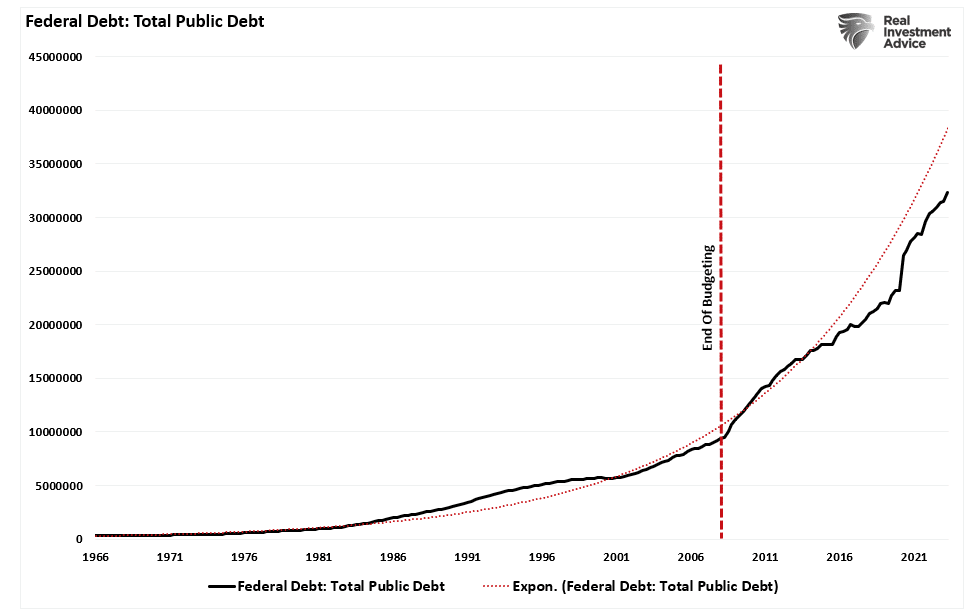

While the latest measure provides funding, we will likely deal with this again in mid-November. What is notable, however, is that the Government has stopped functioning normally since 2008. Before the Obama administration, the Government operated on an annual fiscal budget. The House of Representatives would put together a budget for spending, the Senate would make its modifications, and then it would go back to the House for reconciliation. Once complete, it would move to the President for signature. Funding would then be allocated accordingly.

Compound Spending

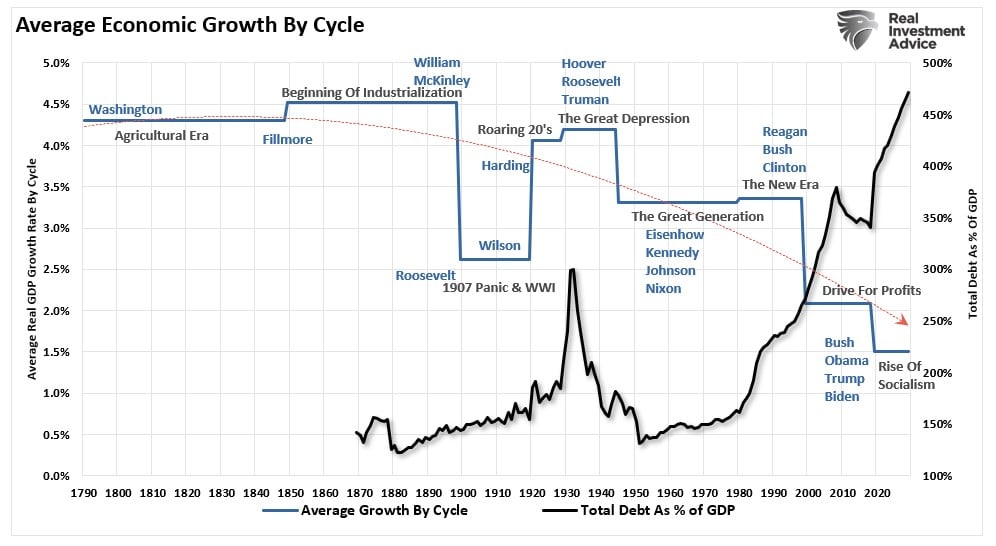

However, since 2008, the Government has continued to operate without a budget. Rather than passing a budget each year, a “Continuing Resolution” is passed to fund spending. The problem with using “Continuing Resolutions” is that it uses the previous spending levels and increases that spending by 8%. Such is why, since 2008, the debt has exploded as spending is compounding annually.

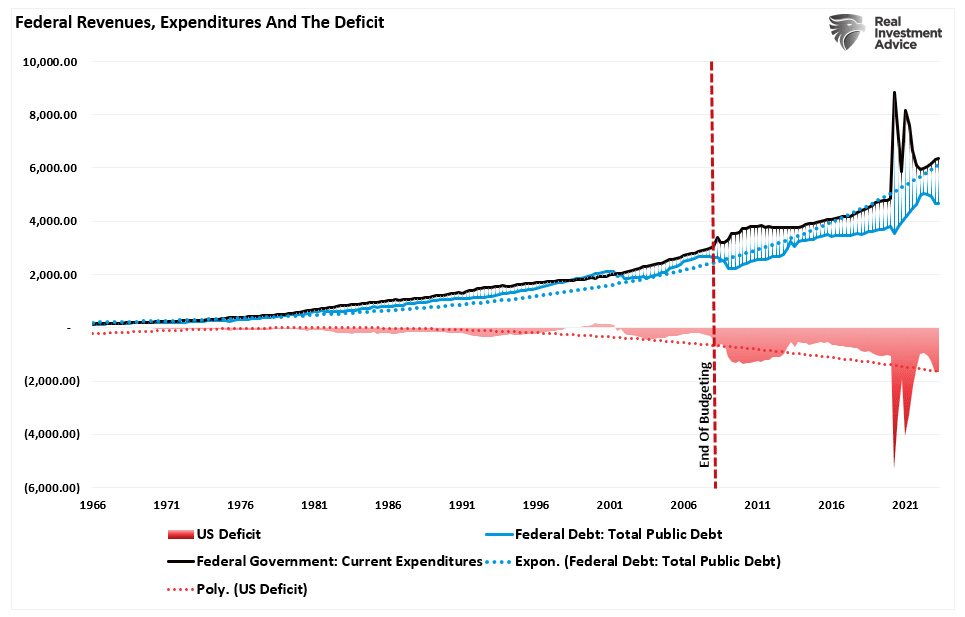

Of course, given the massive surge in spending, revenues cannot keep up the pace, leading to a rapid increase in debt issuance and a trending deficit.

It is worth noting that before 2008, revenues were greater than the running growth trend of public debt. However, post-2008, such has not been the case. Subsequently, the growth in the deficit continues to accelerate.

However, does this mean a calamity is at hand with the Government now shut down?

A Temporary Delay Doesn’t Solve The Problem

While the media and Government officials will declare victory over avoiding a Government shutdown, is it a victory? Washington, D.C., has a long history of “kicking the can” to avoid doing its “job” of governing. That job sometimes includes making unpopular decisions that cause short-term pain for a healthier economy in the years ahead.

Rather than taking the easy path, it is essential to understand what occurs during a Government shutdown. Yes, roughly 900,000 “non-essential” workers will be furloughed. While their salaries will accrue during the furlough, the lack of income will impact economic growth. That impact would be relatively minor, and based on past shutdowns, Goldman Sachs estimated a reduction of annualized growth by around 0.2% for each week it lasted after accounting for modest private-sector effects.

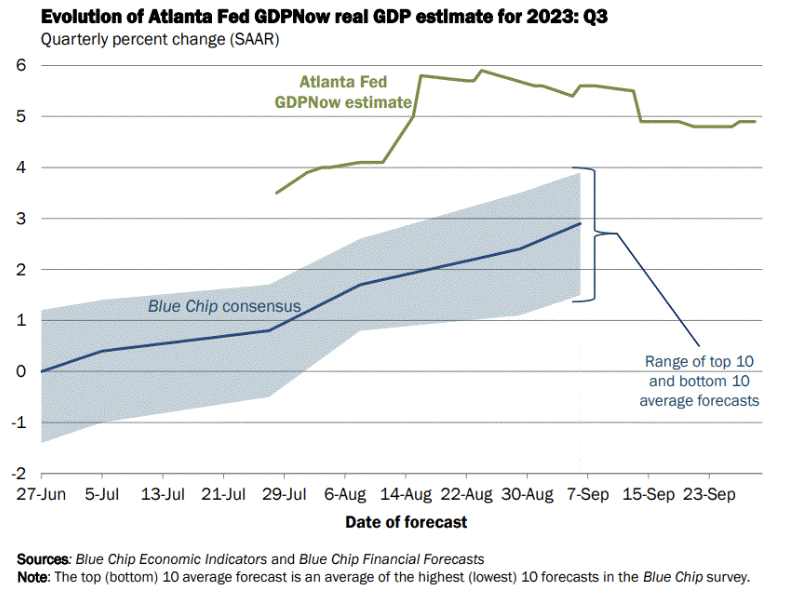

Given that the longest shutdown lasted 35 days, as shown above, you can estimate the impact on economic growth could be roughly as much as 1%. Yes, that is certainly concerning, but with economic growth running near 5% according to the latest Atlanta Fed GDPNow, such is not a recessionary concern.

Shutdowns Are About Discretionary Spending

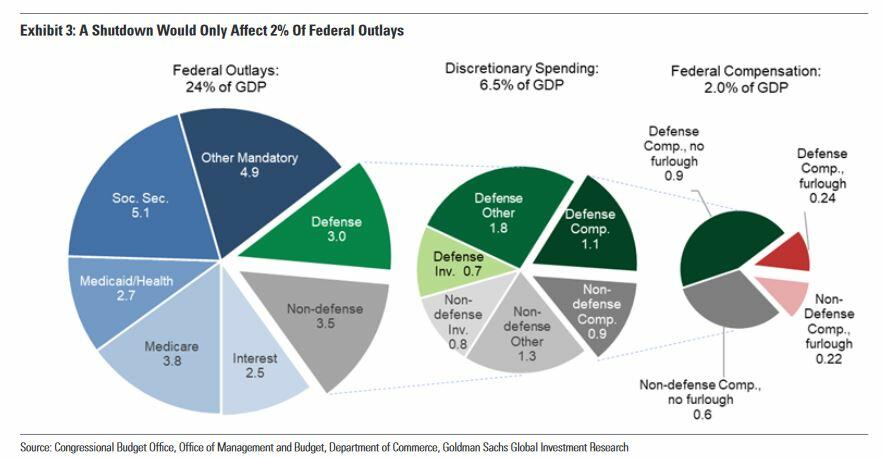

What is critical to understand about Government shutdowns is that mandatory spending (social security, welfare, interest on the debt) continues as needed. Shutdowns are primarily about discretionary spending. Such is why it mainly involves Government employment and the shuttering of national parks and monuments. According to Goldman Sachs, the shutdown would have only impacted about 2% of Federal spending overall. Notice that the vast majority of Government spending is directly a function of the social welfare system and interest on the debt.

The above chart shows spending as a percent of GDP. However, using the 2023 data from the Center On Budget Policy, we can better understand why we have a problem with our welfare system.

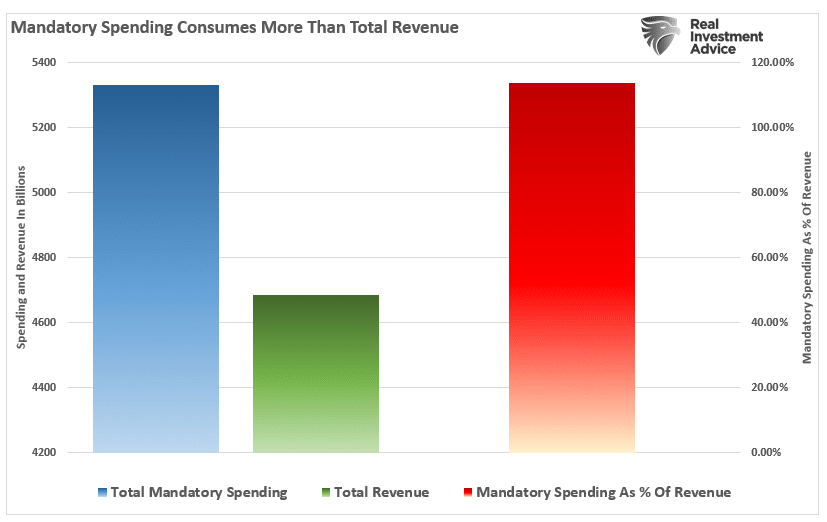

As of the latest annual data, through the end of Q2-2023, the Government spent $6.3 Trillion, of which $5.3 Trillion went to mandatory expenses. In other words, it currently requires 113% of every $1 of revenue to pay for social welfare and interest on the debt. Everything else must come from debt issuance.

While a Government shutdown would undoubtedly create a minor negative impact on economic growth, maybe such would be an acceptable price to return the Government to some form of fiscal responsibility.

What A Shutdown Would Mean For The Markets?

But what impact would a shutdown have on the financial markets?

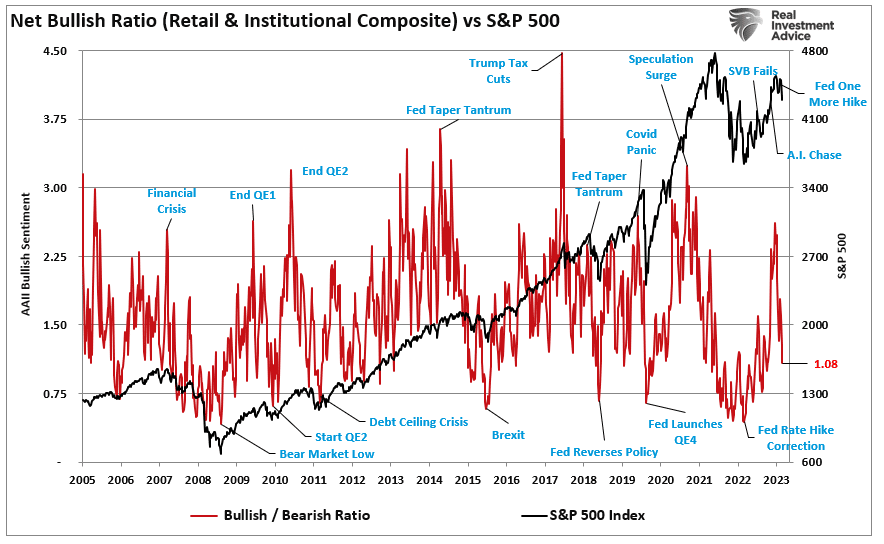

This past weekend’s newsletter discussed why the recent summer weakness laid the groundwork for a potential year-end rally. To wit:

“As a contrarian investor, excesses get built when everyone is on the same side of the trade. With that said, everyone is so bearish the markets could respond in a manner no one expects. The chart below shows the relatively sharp decline from the more exuberant bullish sentiment we saw in June and July. Historically, when the combined readings of retail and professional sentiment reached current levels, such formed the basis for a reflexive rally.“

A Government shutdown would undoubtedly impact the financial markets as investors remain skittish about committing capital into an uncertain environment. However, as noted by Zerohedge recently:

“What’s more, market reactions to government shutdowns have become increasingly muted given that despite the high odds of a shutdown, funding typically arrives at the 11th hour via a ‘continuing resolution’ to provide temporary funding at the start of the Oct. 1 fiscal year, which eventually translates to longer-term spending bills. A failure to do either leads to a shutdown – which looks likely at this point.”

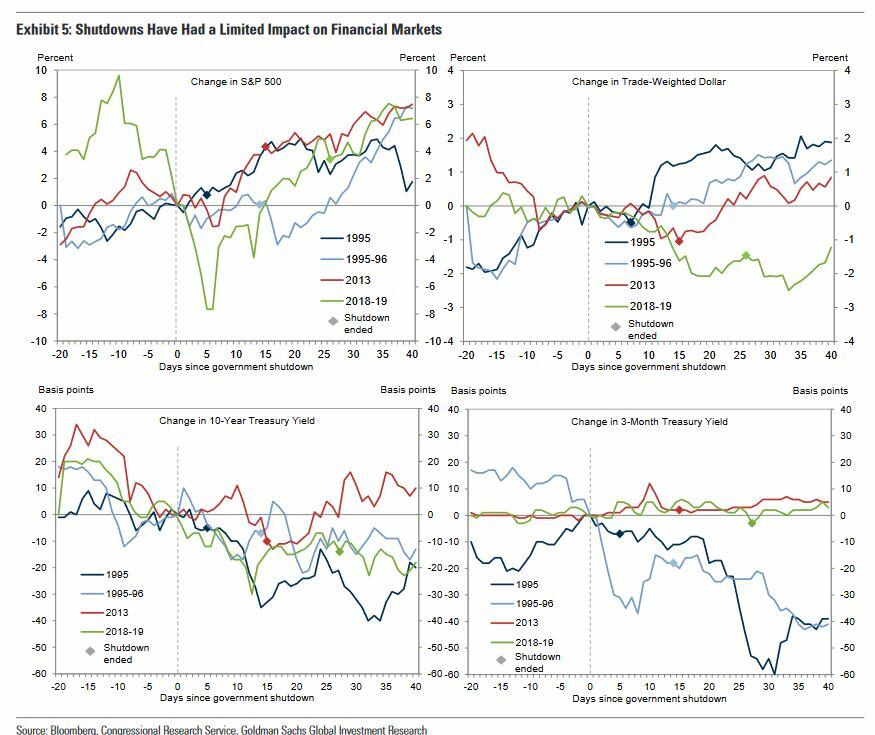

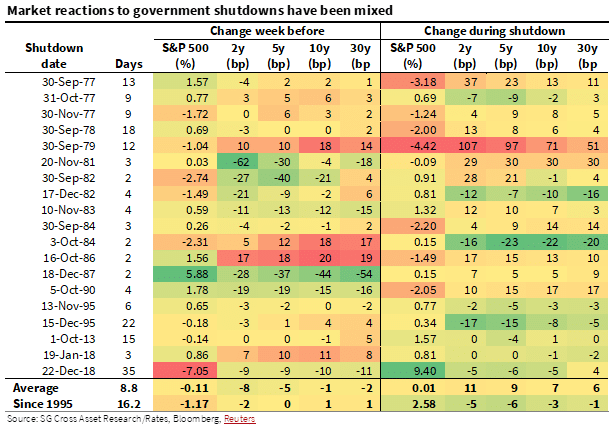

As shown in the table below, since 1995, markets tend to wobble heading into and during the Government shutdown but tend to post positive returns overall.

While the mainstream media’s hyperbole about Government shutdowns is undoubtedly concerning, the reality is that they have little impact on both the economy and the financial markets.

The fiscal irresponsibility in Washington, D.C., which continues to erode economic growth, prosperity, and a stronger middle class, should be of more concern.

As we concluded in “Debts, Deficits, and Why $32 Trillion Matters,”

“{The debt] is one of the primary reasons why economic growth will continue to run at lower levels. Changes in structural employment, demographics, and deflationary pressures derived from changes in productivity will magnify these problems.“

Like a forest fire cleanses and fertilizes the soil, making the forest healthier, maybe a Government shutdown that returns some fiscal responsibility to Washington might be a good thing.

Related: “Soft Landing” Hope by the Fed Is Likely Optimistic