Trending

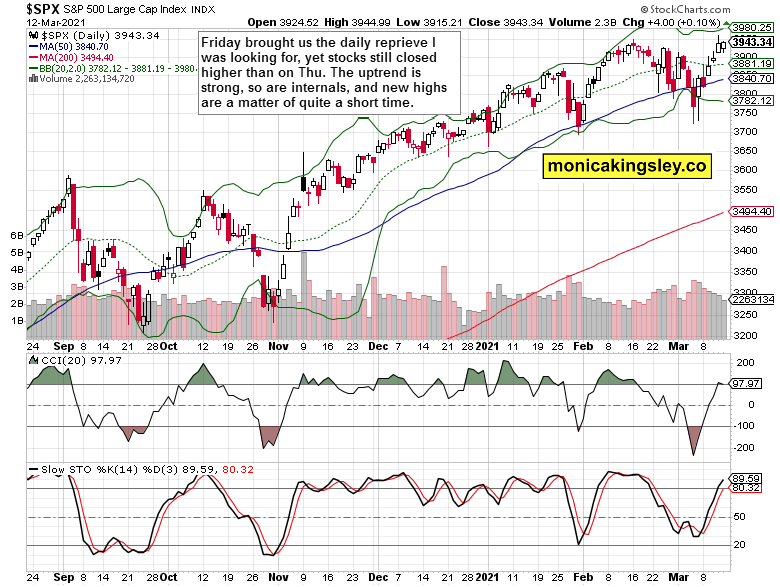

Now that stocks closed at new all time highs, the correction is officially over. And what little rest stock bulls could claim last week, arrived on Friday. Yet, the bull is strong enough to defend the 3,900 zone, and charge higher the same day.

Who could be surprised, given the modern monetary theory ruling the economic landscape? The Fed amply accomodative, one $1.9T stimulus bill just in, and a $2T infrastructure one in the making. That‘s after the prior Trump stimulus, and who would have forgotten how it all started in April 2020? The old congressional saying „a billion here, a billion there, and pretty soon you‘re talking real money“, needs updating.

Stocks are readying another upswing as the volatility index is approaching 20 again, and the put/call ratio shows complacent readings. The sectoral examination supports higher highs as tech has reversed intraday losses, closing half of the opening bearish gap. Value stocks naturally powered to new highs, with industrials, energy and financial performing best. Real estate keeps showing remarkable momentum, and has been among the best performers off correction‘s lows.

These all have happened while long-term Treasury yields have broken to new highs. Are they stopping to be the boogeyman?

As I‘ll show you, inflation expectations are rising – and the bond market is reflecting that. The market‘s discounting mechanism is at work, mirroring the future virtually ascertained CPI rise, if you look carefully into the PPI entrails. This inflation won‘t be as temporary as the Fed proclaims it would – but it still hasn‘t arrived in full force. We‘re merely at the stage of financial assets rising, because that‘s where the newly minted money is chiefly going.

As regards gold, let‘s recall my Thursday‘s words:

(…) At the moment, evaluating the strength and internals of precious metals rebound, is the way to go as we might very well have seen the gold bottom, with the timid $1,670 zone test being all the bears could muster. Time and my dutiful reporting will tell.

Let‘s move right into the charts (all courtesy of www.stockcharts.com).

S&P 500 Outlook

The S&P 500 upswing took a little breath, and at the same time continued unchallenged. The path of least resistance simply remains higher.

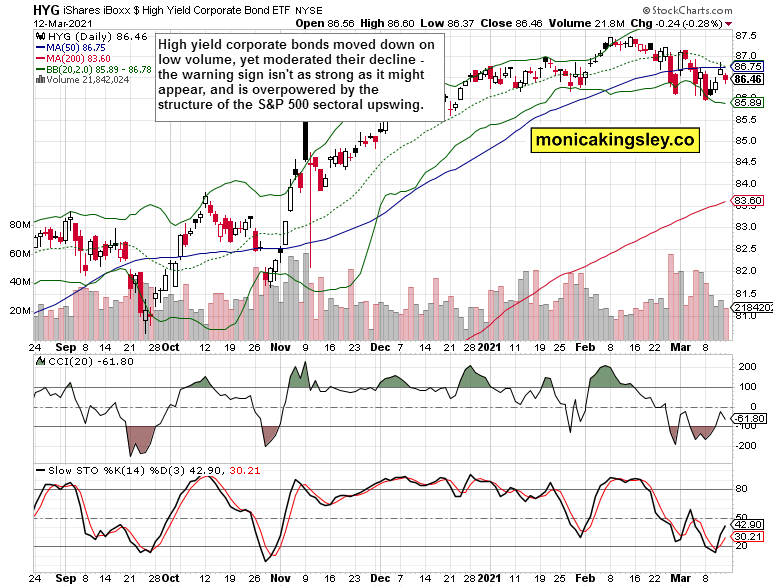

Credit Markets

High yield corporate bonds (HYG ETF) have declined, but don‘t give the impression of readying a breakdown. I understand it as a daily weakness, because the whole bond market was under pressure on Friday, with investment grade corporate bonds (LQD ETF) taking it on the chin as well.

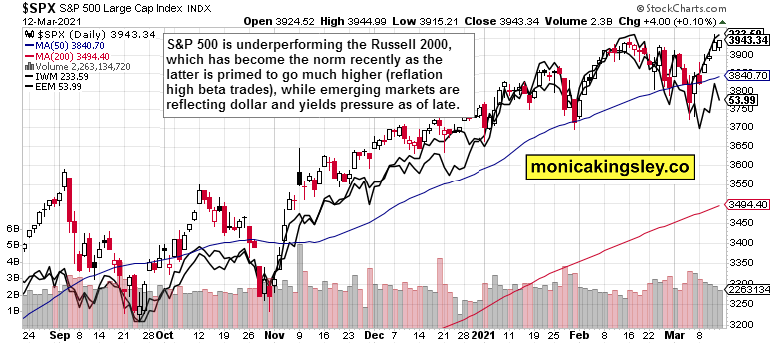

Russell 2000 and Emerging Markets

Russell 2000 keeps doing better than the 500-strong index, which is natural and expected given the prevailing investment themes doing well, value stocks rising, and euphoric speculation running rampant. Emerging market weakness needs to be viewed through the strains stronger dollar and rising rates cause abroad. That‘s why I am not viewing EEM underperformance as a warning sign for U.S. equity markets.

Inflation Expectations and Yields

Quite a relentless rise in my favorite metric of forward looking inflation, isn‘t it? Treasury inflation protected securities to long-dated Treasuries (TIP:TLT) have been relentlessly rising off the corona crash lows, and their accent in 2021 has accelerated just as steeply as the nominal rates reflect (see below).

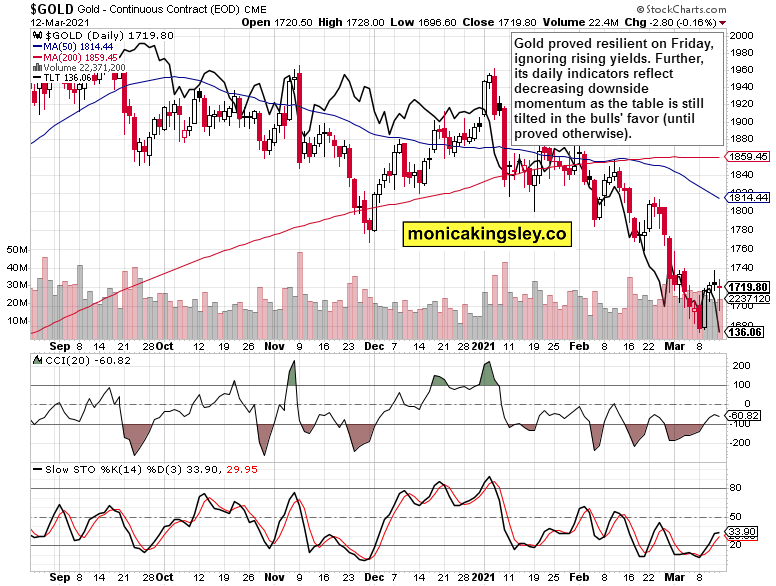

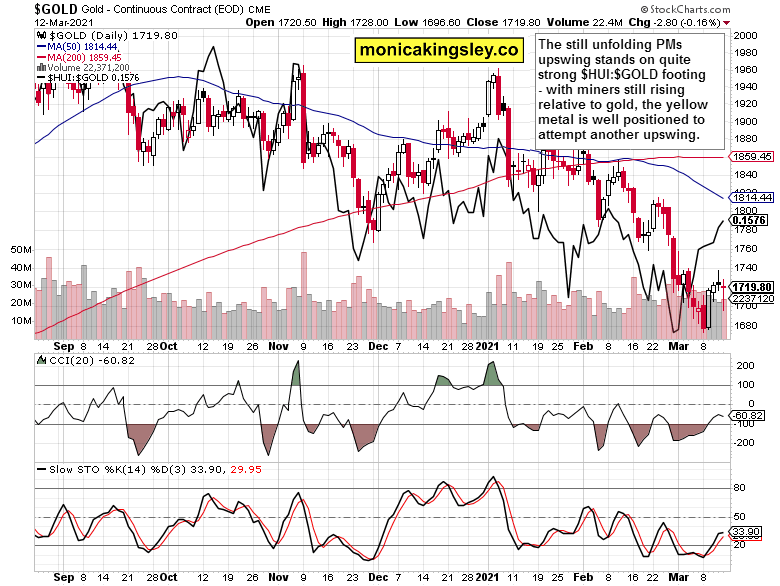

Gold Upswing Anatomy

Gold refused the premarket losses, and has rebounded to close almost unchanged on the day. Is that sign of strength or weakness?

The miners to gold ratio provides a clear answer, and it‘s a bullish one to open the week. Finally, the gold market is showing signs of life on a prolonged basis, which I started talking on Tuesday. Regardless of Friday‘s weakness in the yellow metal, it‘s so far so good as the miners keep leading the charge.

Silver weakness in the course of the upswing isn‘t a too worrying sign – silver miners outperforming as well, is a more important signal. Smacks of broadening leadership in the unfolding precious metals upswing.

Summary

The consolidation of S&P 500 gains was and remains bound to be a short-term affair as the bulls take on new highs and surge well past them in the days and weeks ahead. The top is very far off as this still nascent recovery gets so much stimulus fuel that overheating becomes a very real possibility this year already.

Gold has turned an important corner on Friday, and so have the miners – be they gold or silver ones. The precious metals upswing is unfolding, and decreased sensitivity to rising yields is a pleasant sight for the bulls. Well, that‘s exactly what I had been writing about transitioning to a higher inflation environment exactly one week ago.

Thank you for having read today‘s free analysis, which is available in full at my homesite. There, you can subscribe to the free Monica‘s Insider Club, which features real-time trade calls and intraday updates for both Stock Trading Signals and Gold Trading Signals.

Related: Resting Stock Bulls and Gold Question Marks

The views and opinions expressed in this article are those of the contributor, and do not represent the views of IRIS Media Works and Advisorpedia. Readers should not consider statements made by the contributor as formal recommendations and should consult their financial advisor before making any investment decisions. To read our full disclosure, please click here.