Trending

“Geopolitical Risk” could well be a reason for the Fed to slow-roll tightening monetary policy in March. With Russia invading Ukraine, such would not be the first time that the Fed used “geopolitical risk” to remain cautious on changes to monetary policy.

“Weak global demand and geopolitical risks also argue for going slow, Mr. Powell said, as well as a lower long-run neutral federal-funds rate and the “apparently elevated sensitivity to financial conditions to monetary policy.” – WSJ, May 2016

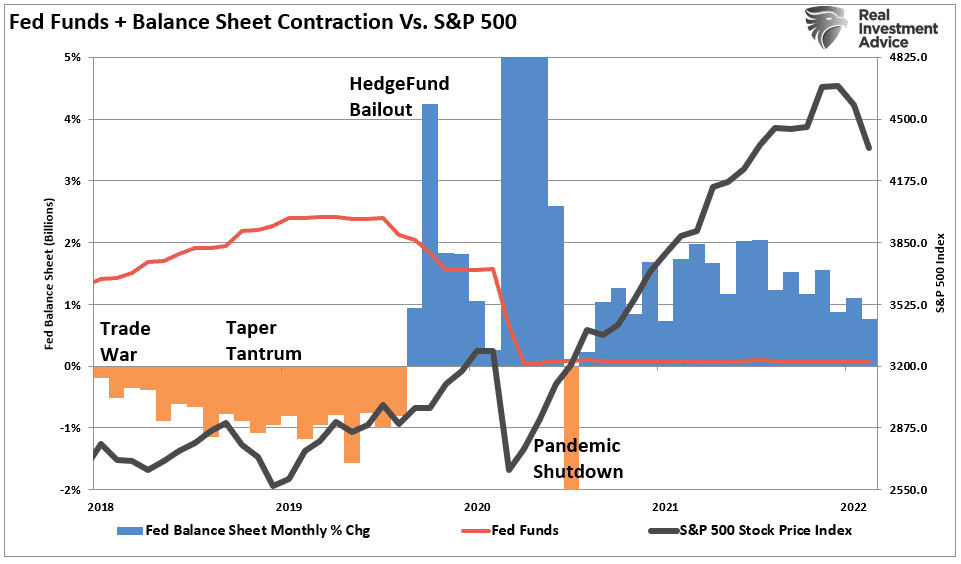

In 2018, the Fed was hiking rates and tapering their balance sheet. Then, with the market under duress, rising geopolitical risks with China began to soften the Fed’s more hawkish stance. Not long after, the Fed started cutting rates and bailed out hedge funds through an “unofficial QE” program. That was all before the 2020 “pandemic-shutdown” bailout of everything.

While the Fed suggests it will hike rates at its March meeting to combat current inflation, they face several challenges from falling consumer confidence, weak markets, and very bearish investor confidence. It wasn’t surprising to see Fed member Mary Daly suggest the FOMC “must navigate geopolitical uncertainty.”

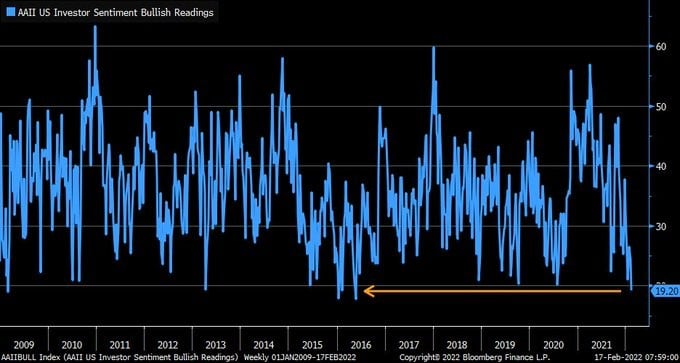

With markets sliding and investors more bearish than in 2016, just before global central banks went “full QE” to offset Brexit, the Fed is now faced with “financial instability.”

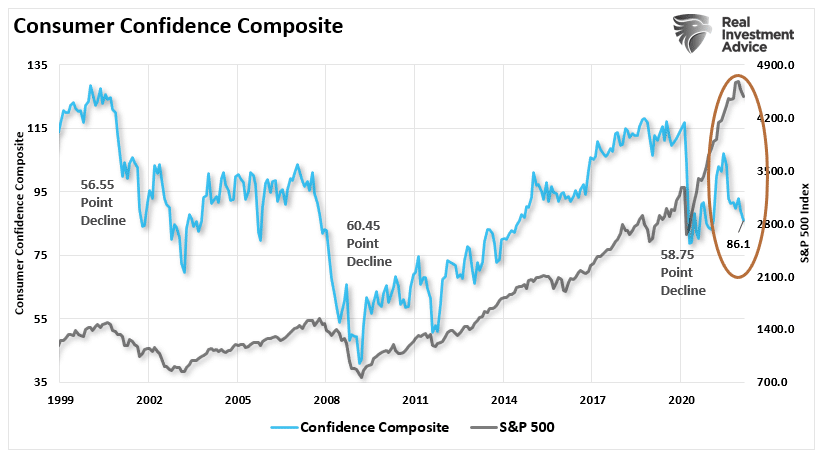

The fallout of the current Russia/Ukraine standoff is not only impacting markets but undercutting consumer confidence as well.

The Consumer Confidence Key

In the U.S., consumers drive 70% of economic growth. Such is why “price stability” is so crucial to the Fed.

To understand why confidence is so vital, we need to revisit what Ben Bernanke said in 2010 as he launched the second round of QE:

“Easier financial conditions will promote economic growth. For example, lower mortgage rates will make housing more affordable and allow more homeowners to refinance. Lower corporate bond rates will encourage investment. And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending.”

The problem is the economy is no longer a “productive” one but rather a “financial” one. A point made by Ellen Brown previously:

“The financialized economy – including stocks, corporate bonds and real estate – is now booming. Meanwhile, the bulk of the population struggles to meet daily expenses. The world’s 500 richest people got $12 trillion richer in 2019, while 45% of Americans have no savings, and nearly 70% could not come up with $1,000 in an emergency without borrowing.=

Central bank policies intended to boost the real economy have had the effect only of boosting the financial economy. The policies’ stated purpose is to increase spending by increasing lending by banks, which are supposed to be the vehicles for liquidity to flow from the financial to the real economy. But this transmission mechanism isn’t working, because consumers are tapped out.”

If consumption retrenches, so does the economy.

The problem for the Fed is that consumer confidence is already declining, tightening monetary policy will exacerbate the decline.

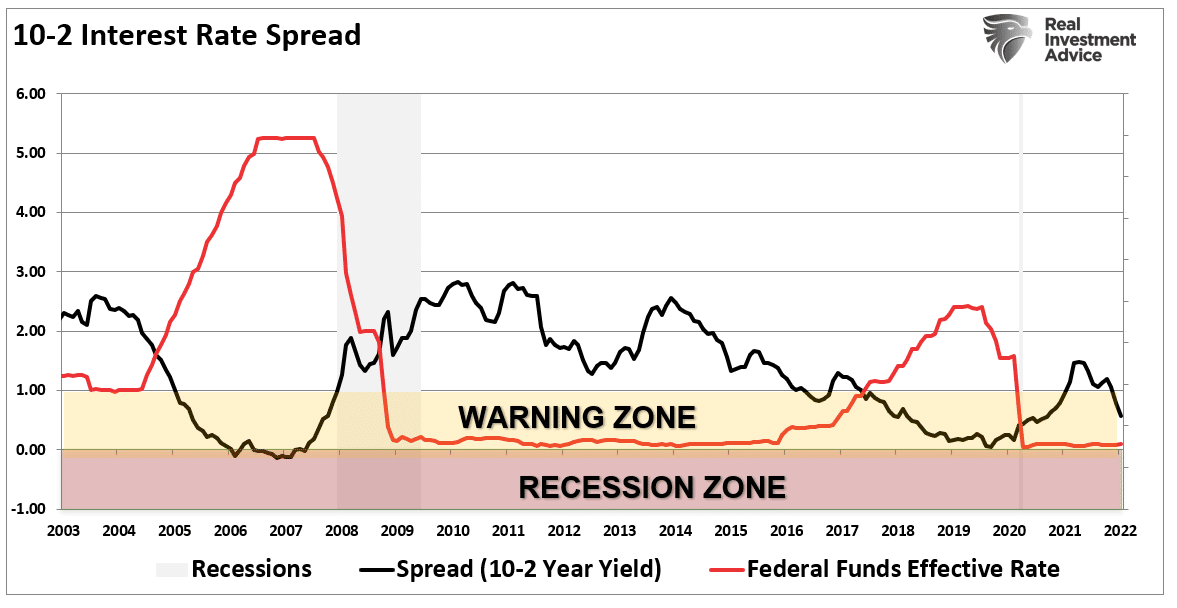

But it isn’t just consumer confidence that’s a problem. The forward yield curve suggests the Fed is already trapped.

The Forward Yield Curve

One of the most accurate indicators of the onset of a recession is an “inversion” of the yield curve. As noted in Potemkin Economy:

“The most significant risk is the Fed becoming aggressive with tightening monetary policy to the point something breaks. That concern will manifest itself as a disinflationary impulse that pushes the economy towards a recession. The yield curve may be telling us this already.”

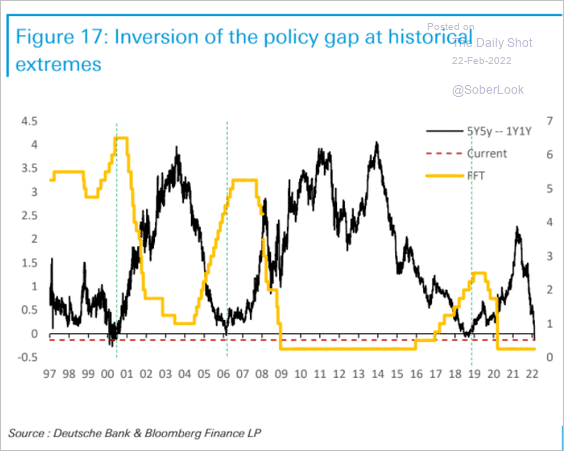

While the yield curve suggests the economy is already weakening, a different yield curve suggests the Fed may be too late. The chart below shows the difference in yields between the 5-year and 1-year forward yields. This particular yield curve indicates that deflation and economic weakness will arrive over the 12-months.

Importantly, note that when this “forward” yield curve becomes inverted, the Fed was close to a peak in their rate hiking cycle. The obvious problem is that the forward yield curve is inverted, and rates remain at zero.

The Fed has little room for error between an inverted forward curve, declining consumer confidence, and increasing geopolitical risk.

While they will try to hike rates, we suspect they will wind up “breaking something.”

History Suggests The Fed Will Make A Mistake

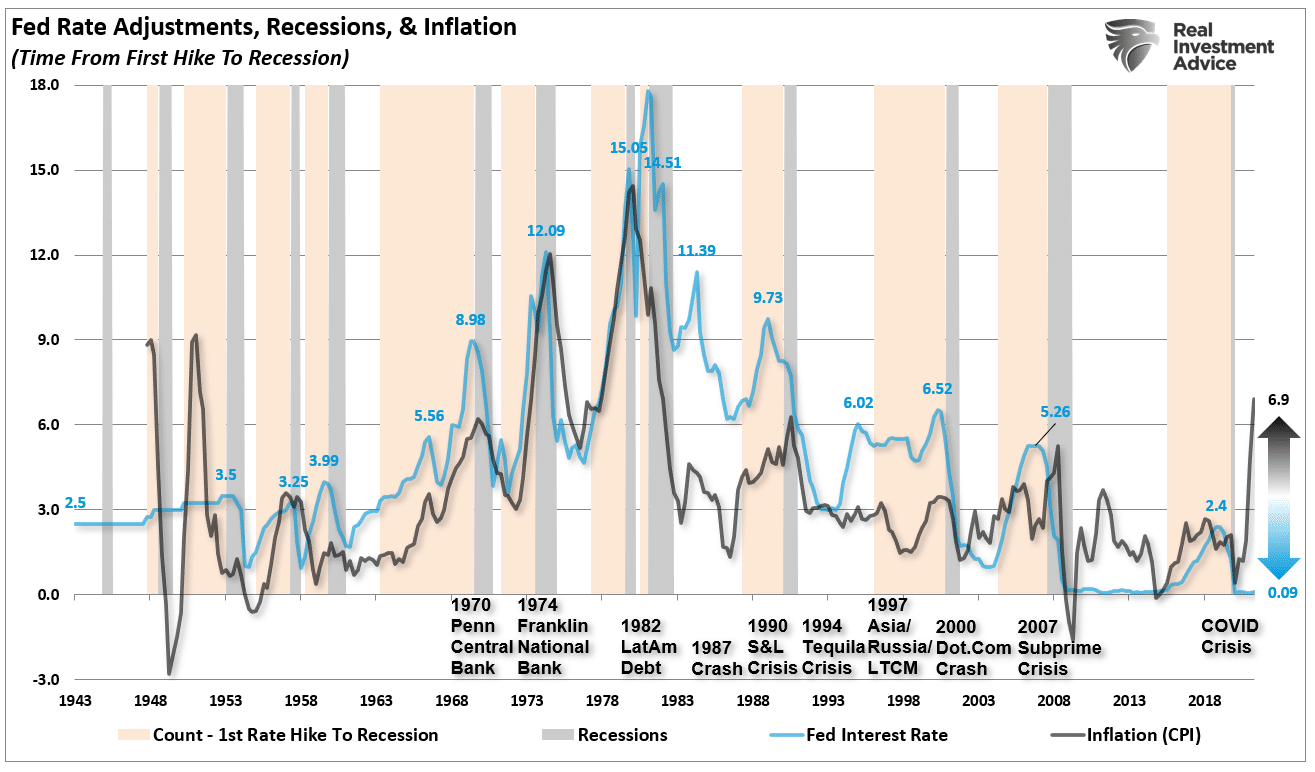

Since 1980, every time the Fed tightened monetary policy by hiking rates, inflation remained “well contained.” The chart below shows the Fed funds rate compared to the consumer price index (CPI) as a proxy for inflation.

There are three essential points in the chart above.

- The Fed tends to hike rates along with inflation, to the point it “breaks something” in the market.

- For the majority of the last 30-years the Fed has operated with inflation averaging well below 3%.

- The current spread between inflation and the Fed funds rate is the largest on record.

Historically, the Fed hiked rates to combat inflation by slowing economic growth.

However, this time the Fed is hiking rates after short-term fiscal stimulus pulled-forward demand, creating an artificial inflation surge.

Importantly, many of those crisis points were credit-related. With debt and leverage near historic high levels, increasing interest rates inevitably causes a problem. As Former Fed Governor Randall Kroszner previously said:

“The big debts that governments are racking up are going to make it difficult for central banks to raise rates when they feel the need to do so because that will increase borrowing costs.”

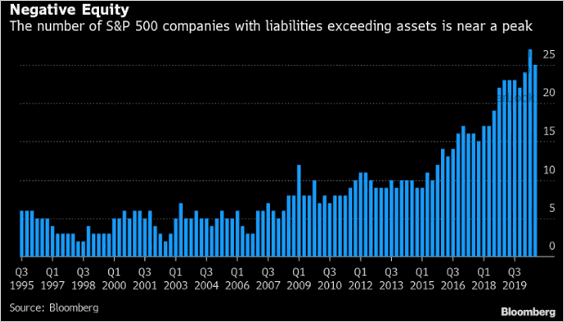

In an economy laden by more than $75 Trillion in debt, a record number of “Zombie” companies kept alive by low borrowing costs, and a near-record number of companies with negative equity, higher rates will be a problem. The only question is when?

As noted above, the last time that “geopolitical risks” were of concern to the Fed was in 2018 and 2019. Currently, the market is mapping out much the same course.

We will not be surprised to see the Fed soften its position on rate hikes in March for all of these reasons.

The 2018 analog may already be telling us the same.

Related: The Consequences of the Russian Attack for the Markets and the Economy