Trending

As widely expected, the Fed cut the Fed Funds rate by 25bps, to 4.25-4.50%, at this week’s FOMC meeting. Moreover, they intimated that after cutting rates by 1% since September, they are likely to be more data-dependent, which may slow the pace of further rate cuts. They want to see inflation trend lower again and/or the unemployment rate tick higher before cutting rates again. Beth Hammack from the Cleveland Fed was the lone dissenter.

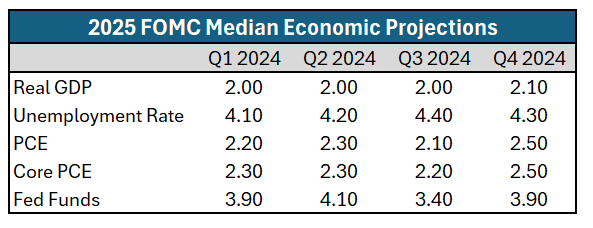

Their posture toward more rate cuts and future policy was probably more important for investors than its rate decision. To help better assess their updated views, the meeting included the Fed’s fourth-quarter economic projections. The Fed now expects to cut rates by only .50% throughout 2025. Three months ago, they thought they would lower them by 1%. The market is now on the same page as the Fed, as it was expecting two 25bps rate cuts in 2025 before yesterday’s meeting.

The table below shows the evolution of the Fed’s 2025 economic projections over the last four quarters. The Fed raised its inflation forecast from last quarter to 2.50% for PCE and Core PCE. Currently, PCE is 2.3%, and Core PCE is 2.8%. More importantly, the increase implies that the Fed believes inflation may be stuck at current levels for 2025. However, their inflation forecasts beyond 2025 are intact at around 2%.

What To Watch

Earnings

Economy

Market Trading Update

In yesterday’s commentary, we discussed the market’s bad breadth, which typically precedes short—to intermediate-term corrections and consolidations. Will bad breadth spoil the “Santa Claus” rally? Maybe. However, yesterday, that bad breadth collided with a more hawkish Fed, causing a sharp decline across all asset markets. Tomorrow morning, we will analyze the carnage and see if the Fed just “Stole Christmas” or if the bulls can regain control at year’s end.

In today’s commentary, I would like to discuss the recent rise in bond yields, which have been the subject of many email questions lately. As we discussed previously, bond yields are tied to economic growth, wages, and inflation. However, in the short term, bond yields reflect sentiment. As we head into year-end, bonds have been under pressure as managers tax loss harvest the losses in bonds, and there are concerns about the “stickiness” of inflation as of late. However, in the longer term, yields will track economic growth lower, coinciding with lower inflation rates.

Two things to note are as follows. First, when the risk premium of bonds is positive, as it is now, such has historically coincided with a peak in yields.

Secondly, it is not uncommon that when the Fed begins to cut rates, bond yields rise somewhat as markets evaluate market risk. Also, historically, when the Fed started to cut rates, the economy has not yet fully reflected the slowdown in activity. However, as the Fed continues to cut rates and the economy slows, longer-term yields will follow suit. Such will be the same in the future.

With the bond risk premium elevated, the longer-term outlook (next 24-36 months) remains very bond positive. That also inherently suggests that stocks will likely underperform over the same period as valuations correct to align with a slowdown in earnings growth.

That is just what we are watching.

A Different Twist On Consumer Confidence

Personal consumption accounts for two-thirds of economic activity. Therefore, consumer sentiment and consumers’ collective desire to spend are outsized determinents in economic forecasting. Unlike surveys, which have flaws, consumer confidence is more effectively assessed by analyzing retail sales, such as where and how consumers spend their money. Within retail sales, restaurants and bars have a high correlation with confidence. Simply put, it’s easy to cut back on going out for a meal or drink if your financial confidence is lacking. Conversely, going out for dinner or drinks is common if your confidence improves.

The graph below charts retail sales of food services and drinking places since 1995. The red dotted line is the non-recessionary average from 1995 through 2019. The current annual growth in this retail sales sector is a mere 1.92%. Such is probably less than the rate of inflation for restaurants and bars. Bottom line: Consumers tell us with their wallets that they have little economic confidence. If this continues, the economy could likely slow substantially.

Global Conditions Portend A Catch-Down In America

China, Britain, Europe, and other countries and regions are experiencing sluggish economic growth and, in some cases, contraction. At the same time, the US continues its strong post-pandemic growth pace. Has the US economy diverged from the global economy, or are a lot of economic canaries in coalmines keeling over and warning the US is soon to catch down?

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Related: Are Global Shifts Signaling a U.S. Economic Slowdown?