Trending

Written By: David Trainer

Recap from September’s Picks

The best performing stock in the portfolio was up 6%. Overall, four out of the 15 Exec Comp Aligned with ROIC Stocks outperformed the S&P in September.The success of this Model Portfolio highlights the value of our Robo-Analyst technology [1], which scales our forensic accounting expertise ( featured in Barron’s) across thousands of stocks.This Model Portfolio only includes stocks that earn an Attractive or Very Attractive rating and align executive compensation with improving ROIC. We think this combination provides a uniquely well-screened list of long ideas because return on invested capital ( ROIC) is the primary driver of shareholder value creation. [2]New Stock Feature for October: NVR Inc. (NVR)

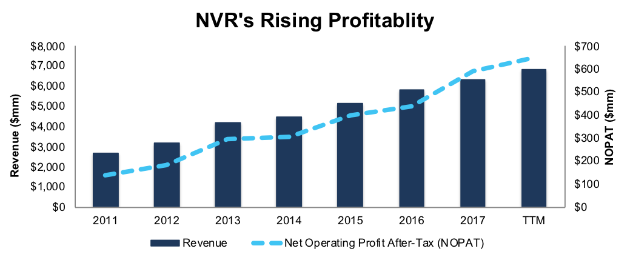

NVR Inc.( NVR[NYE] - $2,242.04 ) is the featured stock in October’s Exec Comp Aligned with ROIC Model Portfolio. NVR was previously featured as a Long Idea in April 2017 and reiterated in November 2017. The stock has fallen in recent months as homebuilding has slowed, and the market underappreciates NVR’s rising profitability.Since 2011, NVR has grown revenue by 15% compounded annually and after-tax operating profit ( NOPAT) by 27% compounded annually, to $589 million in 2017, per Figure 1. NOPAT has increased further, to $651 million, over the trailing twelve months (TTM), which is up 23% over the prior TTM period. NVR’s NOPAT margin has improved from 5% in 2011 to 10% TTM. Figure 1: NVR Revenue & NOPAT Since 2011 Sources: New Constructs, LLC and company filings

Sources: New Constructs, LLC and company filingsExecutive Compensation Plan Helps Drive Shareholder Value Creation

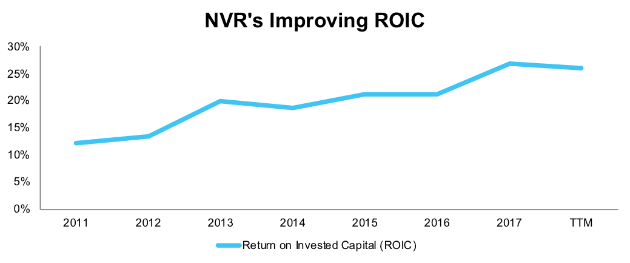

NVR has included return on capital as a performance metric in its executive compensation plan since 2014. Last year, 50% of equity grants were tied to return on capital performance. For performance-based options, vesting is subject to NVR’s return on capital relative to its peer group.Related: Skilled Traders Can Find Profits In Small CapsThe focus on return on capital helps ensure executives are aligned with shareholders’ interests. Since adding return on capital to its compensation plan in 2014, NVR has grown ROIC from 19% to 26% TTM. This improvement follows a long-term trend, in which ROIC has improved from 12% in 2011, per Figure 2. NVR’s executive compensation plan lowers the risk of investing in the company’s stock because we know executives’ interests are tied to shareholders’ interests. Figure 2: NVR’s ROIC Since 2011 Sources: New Constructs, LLC and company filings

Sources: New Constructs, LLC and company filings