Written by: Lance Roberts

Last Friday, I discussed that without much fanfare or public discussion, Congress decided to push the U.S. into deeper fiscal irresponsibility with the

passage of another Continuing Resolution ( CR). To wit:“The House on Wednesday passed an $854 billion spending bill to avert an October shutdown, funding large swaths of the government while pushing the funding deadline for others until Dec. 7.The bill passed by 361-61, a week after the Senate passed an identical measure by a vote of 93-7.”Without the passage of the C.R. the government was facing a “shut-down” just prior to the mid-term elections. So, rather than doing what is fiscally responsible for the long-term solvency and financial health of the country, not to mention the generations to come,

they decided it was far more important to get re-elected into office. As I noted last week:

“For almost a decade, Congress has failed to pass, and operate, underneath a budget. Of course, without any repercussions from voters in demanding that Congress ‘does their job,’ the path to fiscal insolvency continues to grow.The Committee For A Responsible Federal Budget made the following statement:“We’re pleased policymakers have likely avoided a shutdown and actually appropriated most of this year’s discretionary budget on time.

But let’s not forget that Congress did so without a budget and had to grease the wheels with $153 billion to pass these bills. That isn’t function; it’s a fiscal free-for-all.”Of course, with trillion-dollar deficits just around the corner, the negative impact from unbridled spending and debt increases will begin to reverse the positive effects from deregulation and tax reform.”With the end of the Fiscal year for the government ending September 30th,

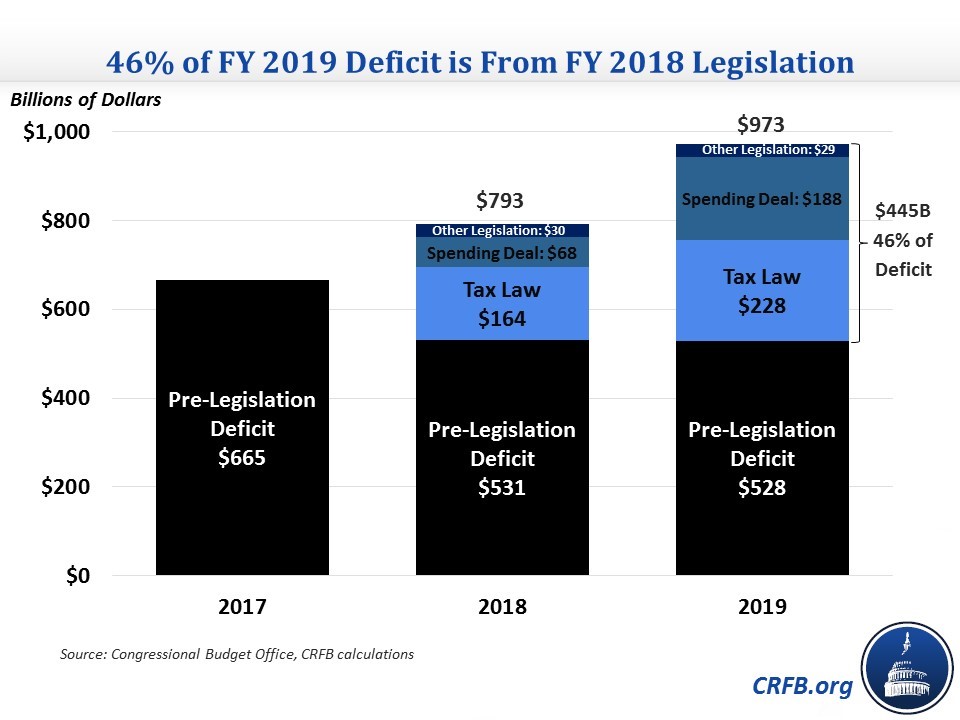

the government now marches into 2019 after having added $2,423,000,000,000 to the debt over the next decade. Of course, that debt was the result of the fiscally irresponsible legislation passed last year which will also add a minimum of another $445 billion to the deficit in the coming year.

As the CRFB notes:

“Two pieces of deficit-financed legislation explain the vast majority of this increased borrowing – the Tax Cuts and Jobs Act of 2017 (TCJA) and the Bipartisan Budget Act of 2018 (BBA18). Looking at next year alone, TCJA is projected to add about $230 billion to the deficit, including its effects on interest costs and economic growth. BBA18 is projected to add another $190 billion. Other legislation, including to delay health-related taxes, provide for disaster relief, and fund the government, is projected to add about $30 billion.”

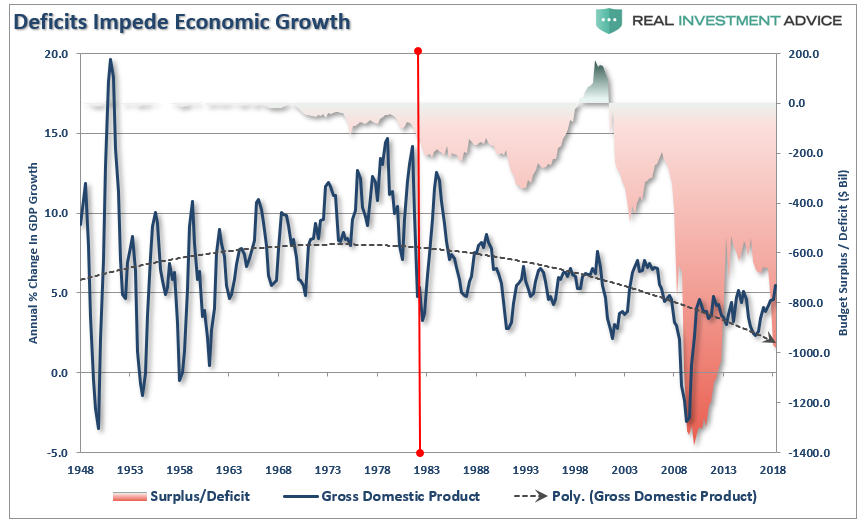

While the markets have been the beneficiary of the tax cut legislation, which gave a short-term boost to corporate profitability, the economy has enjoyed a boost from the massive increases to spending from what should have been more aptly termed the “Bipartisan Non-Budget Act of 2018.” Notice in the chart below the pickup in economic activity has coincided with a surge in the deficit. Spending on natural disasters and defense spending increases “pull forward” future economic growth which is an illusion of an economic turn.

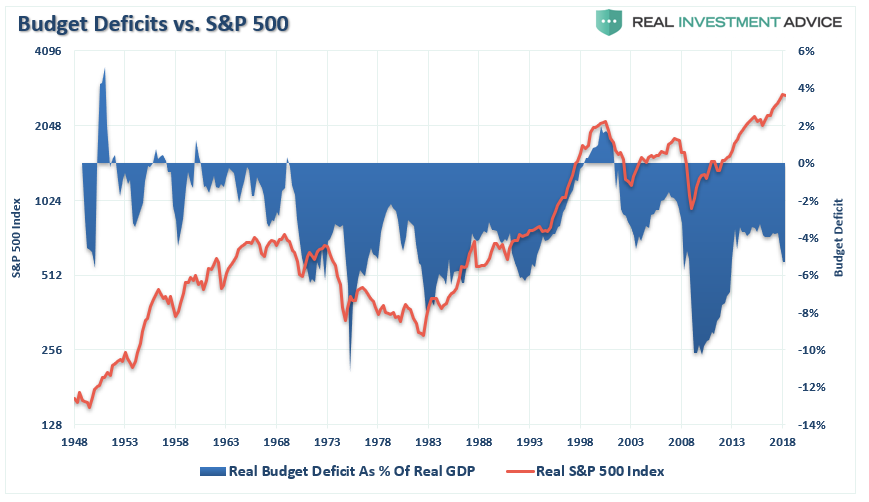

Importantly, surges in budget deficits as a percentage of GDP, are normally associated with “recessionary” activity in the economy.

Importantly, surges in budget deficits as a percentage of GDP, are normally associated with “recessionary” activity in the economy. As noted, the increases in Federal spending create a temporary boost to economic growth which supports higher asset prices.

Currently, the government is running one of the largest deficits, in both dollar terms, and as a percentage of GDP, in history. This is occurring at a time when the economy is “booming” and deficits should be reduced for the next “rainy day.”

Furthermore, with sequester-level budget caps returning next year, the budgetary issues in Washington will become even more complicated. The last time budget-caps came into play Ben Bernanke launched QE-3 to offset the economic drag from expected reductions in government spending.

However, given the recent track record of the “conservative” Congress, it is highly likely spending will be increased further in the months ahead. Look for an even larger “C.R.” in December when the current resolution runs out.Related:

Featured Stock in October’s Exec Comp and ROIC Model PortfolioThe

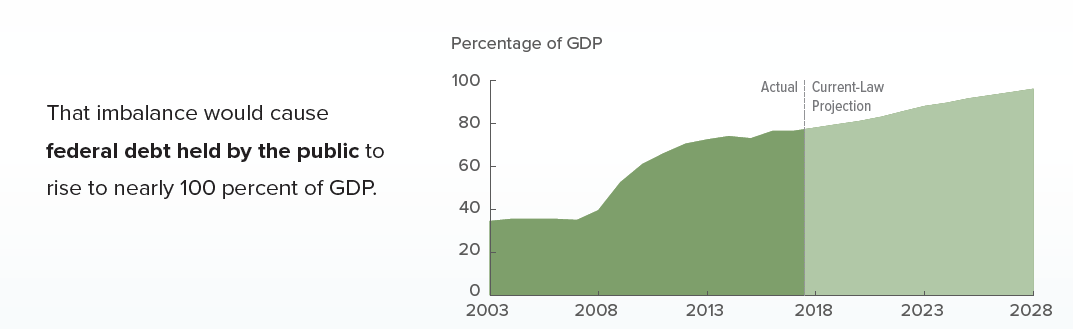

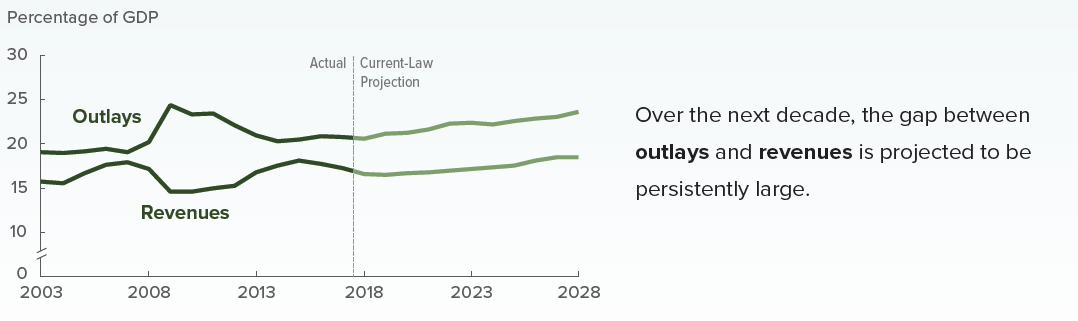

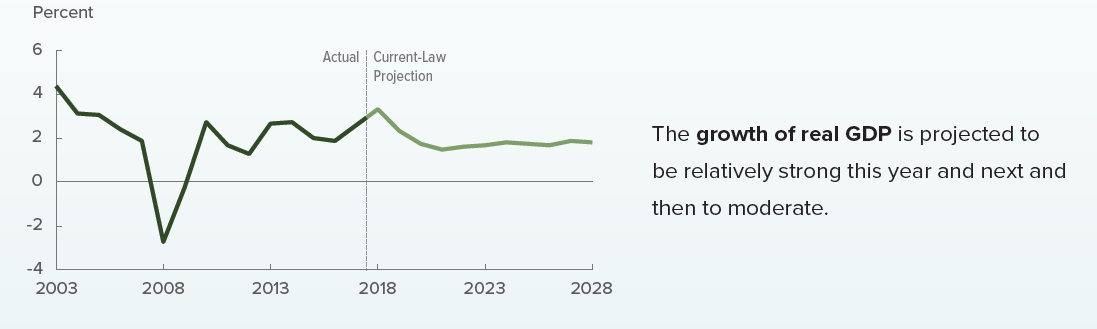

Congressional Budget Office recently estimated the outlook for the economy over the next decade.

First, let me shown you their estimates.

Debt to GDP will rise to nearly 100% of GDP.  The deficit will remain large but won’t widen.

The deficit will remain large but won’t widen.  The growth of real GDP will remain around 2% over the next decade

The growth of real GDP will remain around 2% over the next decade (in line with Fed Reserve estimates.)

The problem is that it is pure fantasy.

It is highly likely the CBO will be incorrect in their assumptions, as they almost always are, because there are many items the CBO is forced to exclude in its calculations.First, the CBO’s governing statutes essentially require a distorted view of the finances by not allowing for an accounting of the tax breaks Congress routinely extends. As

William Gale from the Tax Policy Institute explained:“Here’s the bad part: Under current law, CBO projects that the debt – currently 77 percent as large as annual GDP – will rise to 96 percent of GDP by 2028. And that’s if Congress does nothing. If instead, Congress votes to extend expiring tax provisions – such as the many temporary tax cuts in the 2017 tax overhaul – and maintain spending levels enacted in the budget deal (which is called the “current policy” baseline), debt is projected to rise to 105 percent of GDP by 2028, the highest level ever except for one year during World War II (when it was 106 percent).”So, once you understand what the CBO isn’t allowed to calculate or show, it is not surprising their predictions have consistently overstated reality over time.

However, it’s how Congress wants the projections reported so they can continue to ignore their fiscal responsibilities.Secondly, a big problem David Stockman, former head of Government Accountability Office, pointed out:“Whereas the CBO report already forecasts cumulative deficits of

$12.5 trillion during the next decade, you’d get

$20 trillion of cumulative deficits

if you set aside Rosy Scenario and remove the crooked accounting from the CBO baseline.In a word, what was a

$20 trillion national debt when the Donald arrived in the White House is no longer. Now it’s barreling toward

$40 trillion within the next decade.We have no ideas how much economic carnage that will cause, but we are quite sure it will not make America Great Again.”Besides those flaws, the CBO gives

NO WEIGHT to either a potential for an economic “slowdown” or “recession.” Nor is consideration given to the structural changes which will continue to plague economic growth going forward.

Spending Hikes Demographics Surging health care costs Structural employment shifts Technological innovations Globalization Financialization Global debtThese factors will continue to send the debt to GDP ratios to record levels. The debt, combined with these numerous challenges, will continue to weigh on economic growth, wages and standards of living into the foreseeable future.

As a result, incremental tax and policy changes going forward will have a more muted effect on the economy as well. Conclusion

The CBO’s latest budget projections confirm what we, and the CRFB, have been warning about.

The current Administration has taken a path of fiscal irresponsibility which will take an already dismal fiscal situation and made it worse.While the previous Administration was continually chastised by “conservative” Republicans for running trillion-dollar deficits, the Republicans have now decided trillion dollar deficits are acceptable.

That is simply hypocritical.Given the flaws in the CBO’s calculations, their current projections of just

$1 trillion in deficits next year, and only slightly exceeding that mark every year after, will likely turn out to be overly optimistic. Even the CBO’s Alternative Fiscal Scenario of

$2 trillion deficits over the next decade could turn out worse.As the Committee for a Responsible Federal Budget

previously stated: Debt Is Rising Unsustainably . Spending Is Growing Faster Than Revenue . Recent Legislation Will Substantially Worsen the Long-Term Outlook if Extended. High And Rising Debt Will Have Adverse and Potentially Dangerous Consequences (Will lead to another financial crisis.) Major Trust Funds Are Headed Toward Insolvency. Fixing the Debt Will Get Harder the Longer Policymakers Wait. While the CRFB suggests that lawmakers need to work together to address this bleak fiscal picture now, so problems do not compound any further, there is little hope that such will actually be the case given the deep partisanship currently running the country.As I have stated before, choices will have to be made either by choice or force.The CRFB agrees with my assessment.“CBO continues to remind us what we’ve known for a while and seem to be ignoring: the federal budget is on an unsustainable course, particularly over the long term.

If policymakers make the tough decisions now –

rather than wait until there’s a crisis point for action – the solutions will be fairer and less painful.”But William Gale summed up the entirety of the problem nicely.“Here’s the worse part: The conventional comparison is misleading. The projected budget deficits in the coming decade are essentially ‘full-employment’ deficits.

This is significant because, while budget deficits can be helpful in recessions by providing an economic stimulus, there are good reasons we should be retrenching during good economic times, including the one we are in now. In fact, CBO projects that, over the 2018-2028 period, actual and potential GDP will be equal.As President Kennedy once said ‘the time to repair the roof is when the sun is shining.’

Instead, we are punching more holes in the fiscal roof. In order to do an ‘apples to apples’ comparison, we should compare our projected Federal budget deficits to full employment deficits. From 1965-2017, full employment deficits averaged just 2.3 percent of GDP, far lower than either our current deficit or the ones projected for the future.

The fact that debt and deficits are rising under conditions of full employment suggests a deeper underlying fiscal problem.”The CBO’s budget projections are a harsh reminder the fiscal largesse that Congress and the Administration lavished on the country in the recent legislation is not a free lunch.It is just a function of time until the economic “train is derailed.”

DISCLOSURE: The views and opinions expressed in this article are those of the authors, and do not represent the views of

equities.com. Readers should not consider statements made by the author as formal recommendations and should consult their financial advisor before making any investment decisions. To read our full disclosure, please go to:

http://www.equities.com/disclaimer