Trending

Many believe Winston Churchill coined the phrase: “Never let a good crisis go to waste.” Others think it was President Obama’s Chief of Staff, Rahm Emanual, who said, “You never want to let a serious crisis go to waste” during the financial crisis. Regardless of who first spoke those words and whether the crisis is “good” or “serious,” the Fed may be planning on heeding their crisis advice.

On February 19, 2025, the Fed made a confounding statement about QT, aka balance sheet reduction. Per its latest FOMC minutes: “several participants suggest halting or slowing balance sheet reduction pending debt ceiling resolution.”

If the government were to stop issuing debt because of a debt ceiling impasse, financial liquidity would increase as the Treasury would spend down its roughly $800 billion piggy bank known as the Treasury General Account (TGA). Due to its positive impact on liquidity, some people call a potential TGA withdrawal “Not QE, QE.”

Thus, if a government shutdown results in additional, albeit temporary, liquidity to the financial system, why halt or slow QT, which drains liquidity?

The timing of the Fed’s confounding statement aligns with an essential gauge of excess liquidity. Might the Fed be offering investors a liquidity warning cloaked as a reaction to a fiscal crisis?

To help answer the question, we review two popular liquidity gauges. In the postscript, following our summary, we share some measures of liquidity and reserves the Federal Reserve monitors.

What Is Water?

Before progressing, it is worth emphasizing how vital and underappreciated liquidity is to the financial markets. We lean on Chris Cole at Artemis Capital to help you appreciate liquidity.

In his piece, What Is Water In The Markets, Cole uses a commencement speech by David Foster Wallace to make an analogy between liquidity in the financial markets and water for a fish. Likely, fish don’t pay attention to the water that surrounds them. Similarly, how often do we think about the air we breathe?

Financial markets, like fish and humans, exist in a medium that sustains its being. Yet, despite the grave importance of liquidity, the market medium, few investors pay much attention to it. Without water, a fish will die. When liquidity fades, volatility often spikes, and market fragilities are exposed. Thus, measuring liquidity, the medium investors struggle to quantify and rarely discuss, is warranted.

The Roots Of The Current Liquidity Omen

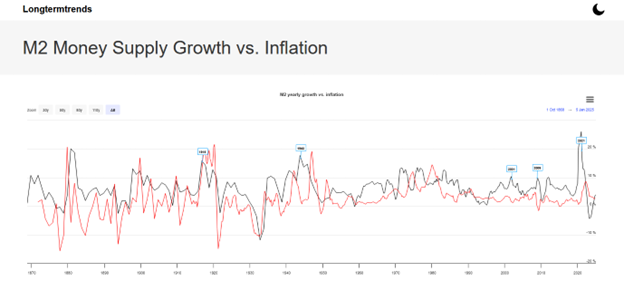

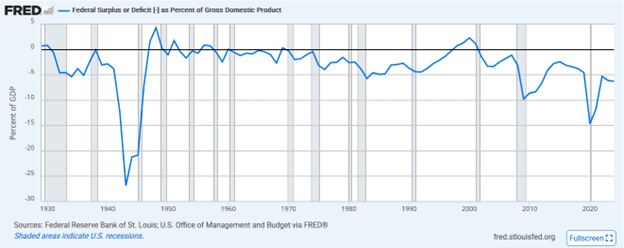

In the pandemic crisis of March 2020, the Federal Reserve and the government opened the liquidity floodgates to combat the shuttering of the global economy. As we share in the first graph below, courtesy of Longtermtrends, in 2020, the percentage growth of M2 money supply (black) grew at a higher rate than at any time in history. The second graph shows that deficit spending as a percentage of GDP was 15% in 2020. The only time since 1930 it was higher was during World War II.

The covid crisis shut down the global economy and sent financial markets plummeting. Liquidity fled the markets, and significant volatility ensued. Consequently, the Fed and government did everything possible to restore economic and market liquidity.

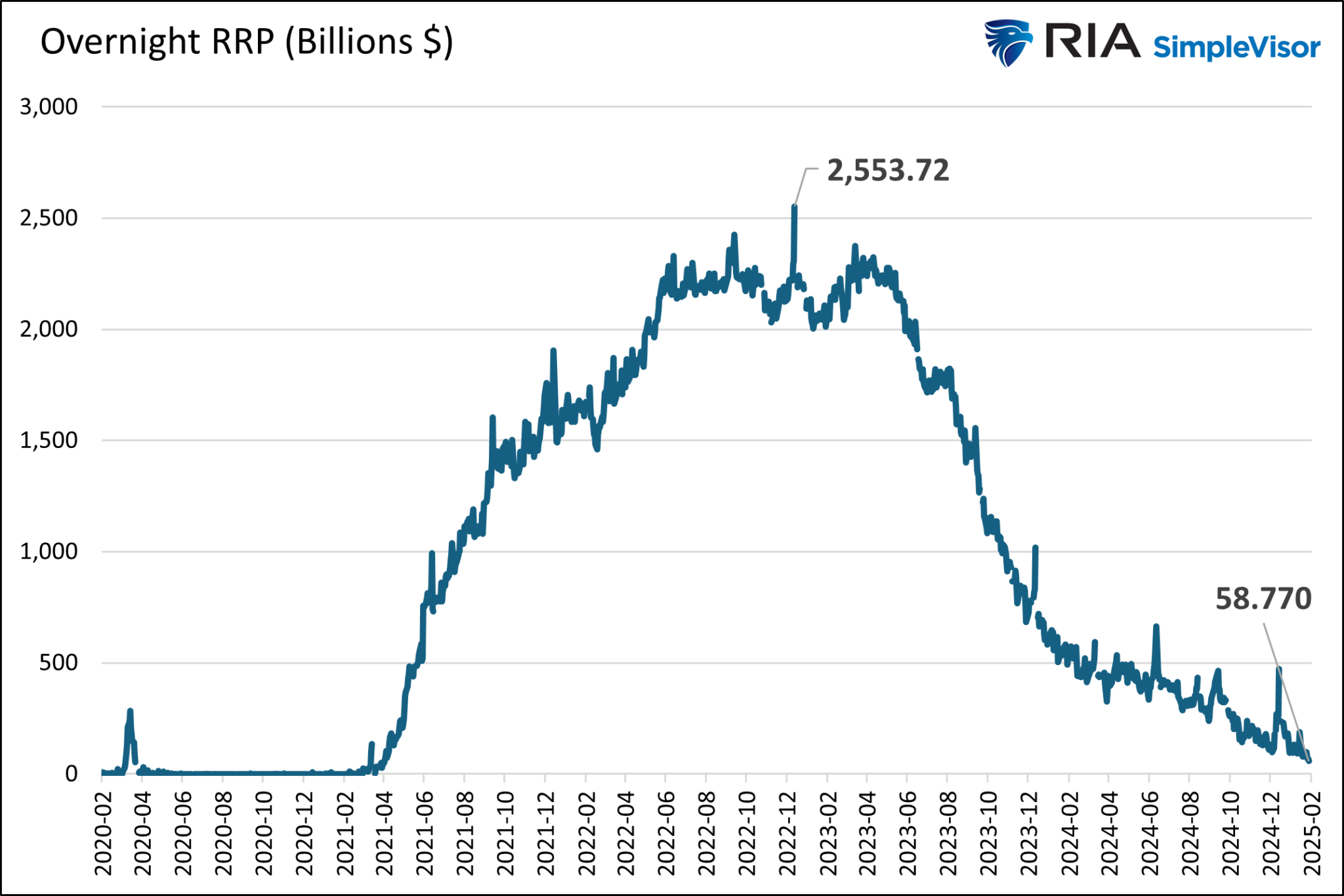

What is now most important to grasp is how much of that extra liquidity still exists. One big clue is the Fed’s Reverse Repurchase Program (RRP).

Reverse Repurchase Program (RRP)

Had the Fed not managed excess liquidity, its monetary policy in 2020 and 2021 would have sent short-term interest rates well into negative territory. The Fed’s RRP was employed to soak up the extra liquidity.

The program allows banks and money markets to lend money to the Fed, and in exchange, the Fed provides them with risk-free Treasury collateral. The “risk-free” money market surrogate effectively met the massive demand for short-term investments and kept rates positive.

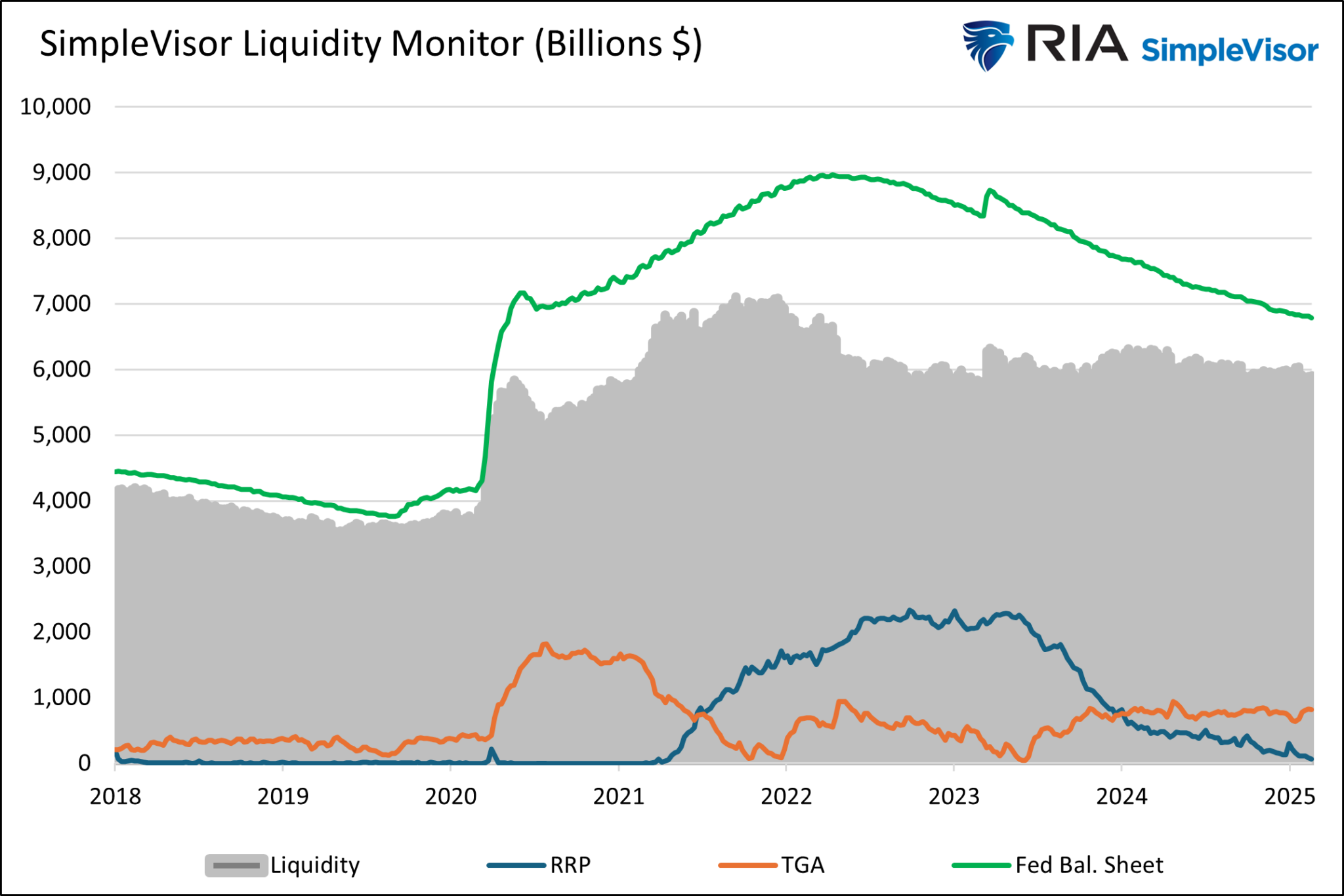

We should consider the RRP balance as the financial market’s excess liquidity. The liquidity warning we allude to in the opening is the current negligible RRP balance. As shown below, the once $2.55 trillion storer of excess liquidity has dwindled to near zero. While liquidity may not be an issue today, there is no longer a massive bank of liquidity for the market to draw on.

With RRP largely evaporated, tracking liquidity becomes much more critical.

Market Monitors of Liquidity

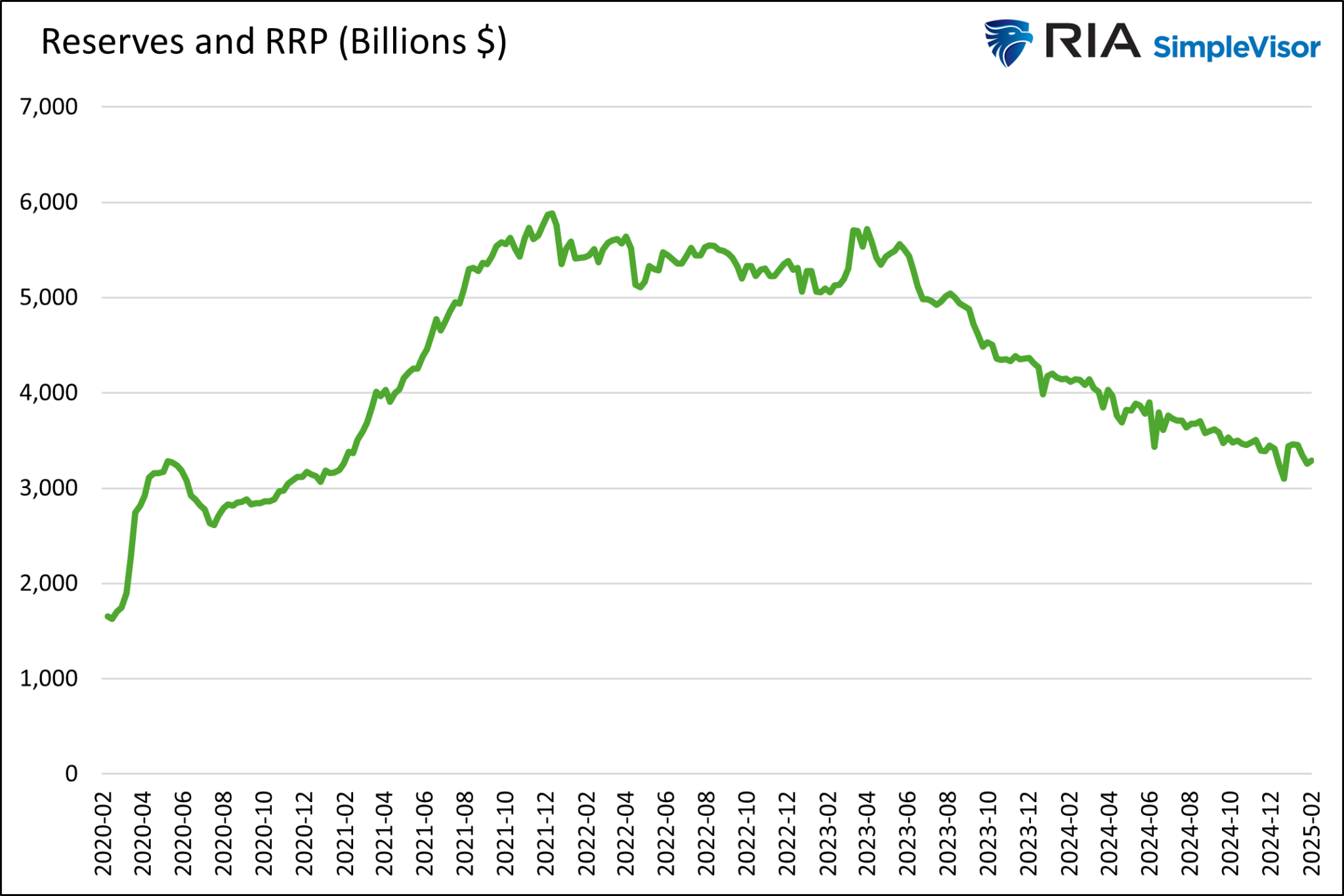

One of the more straightforward gauges of liquidity is the sum of the RRP balances and bank reserves held at the Fed. Bank reserves approximate the potential liquidity banks could provide.

As the data below shows, liquidity, using this measure, is steadily declining. However, it is still well above pre-pandemic levels. The question worth asking but lacking an answer is how much more liquidity our economy and markets require today than before the pandemic.

We use a similar liquidity model that takes the size of the Fed’s balance sheet and subtracts the total of the RRP balances and the Treasury General Account (TGA). The graph below shows that the amount of liquidity (gray), using this measure, has been constant for the last two years. The liquidity from declining RRP balances have thus far offset the Fed’s QT liquidity removal.

With little excess liquidity remaining in the RRP program, this measure of liquidity should start to decline as QT will no longer be offset. However, liquidity could temporarily rise if the Treasury drains its TGA account to help fund the government. Such an increase would be relatively short-lived, thus postponing, not canceling, the eventual decline of liquidity due to QT.

Summary

We surmise the Fed follows the gauges we share and profoundly understands that the potential for a liquidity shortfall will increase as the RRP disappears. Consequently, they may not let the debt ceiling “crisis” go to waste and could use it as an excuse to stop QT.

They need a reasonable justification to end QT because of the term premium embedded in bond yields. Without such a “crisis”, bond investors might assume that ending QT is dovish, thus inflationary, and push yields higher.

Before concluding, it is imperative to state that there is no perfect liquidity gauge. It is incredibly complex and goes beyond the identifiable data we share in this article.

Postscript: Fed Measures of Reserves

If you want to learn more about the banking system and liquidity generation, the following postscript summarizes a recent white paper from the New York Fed.

Bank reserves are the funds a bank keeps on hand, either in its vaults or deposited with the Fed, to meet withdrawal demands and comply with regulatory requirements. Simply, the amount of reserves a bank has corresponds directly with its ability to lend money. Thus, the amount of liquidity they can provide.

In late 2024, Roberto Perli of the New York Fed outlined five measures of bank reserves. They are worth a quick scan to appreciate the state of banking reserves.

The following quotes and graphs are from Perli’s speech entitled Balance Sheet Normalization: Monitoring Reserve Conditions And Understanding Repo Market Pressures. Our comments are added.

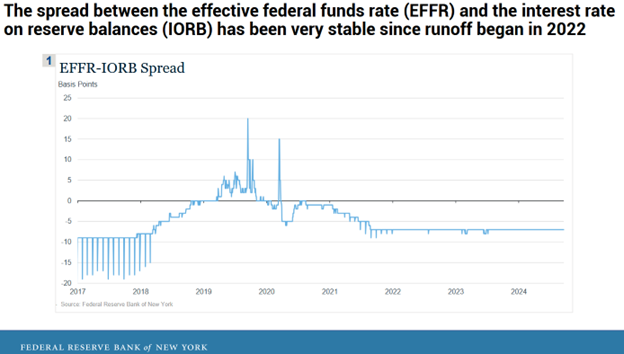

Fed Funds vs. Rate On Reserve Balances

A good starting point is to look at the spread between the effective federal funds rate (EFFR) and the interest rate on reserve balances (IORB). When reserves become less abundant, the cost to borrow federal funds tends to increase relative to IORB.

As the graph below shows, there is nothing to worry about with this metric.

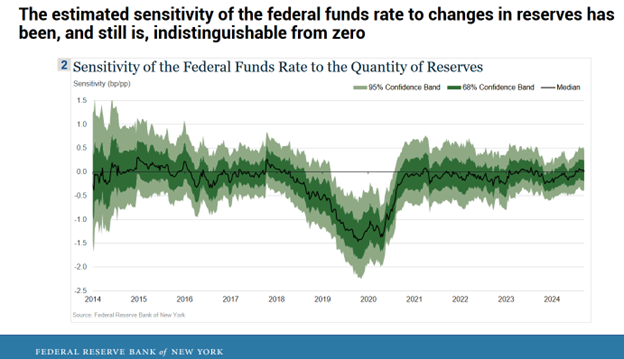

The Sensitivity of Fed Funds To Changes In Reserves

When reserves are abundant, the demand curve is flat, meaning the federal funds rate is insensitive to short term changes in reserve supply. When reserves approach the ample level, that curve should start gently sloping down, and the federal funds rate will start to show some sensitivity to changes in reserves.

Like the first graph, nothing here warrants concern about the level of reserves in the banking system.

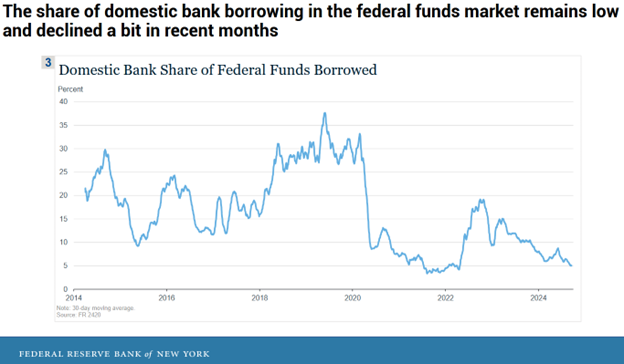

Domestic Bank Borrowing In The Fed Funds Market

We also carefully monitor the share of domestic bank borrowing in the federal funds market. Because domestic banks tend to borrow federal funds when they need liquidity, increased activity on their part would be a sign of reserves becoming less abundant.

The percentage of domestic bank borrowing is declining. Therefore, this, too, provides little reason for concern.

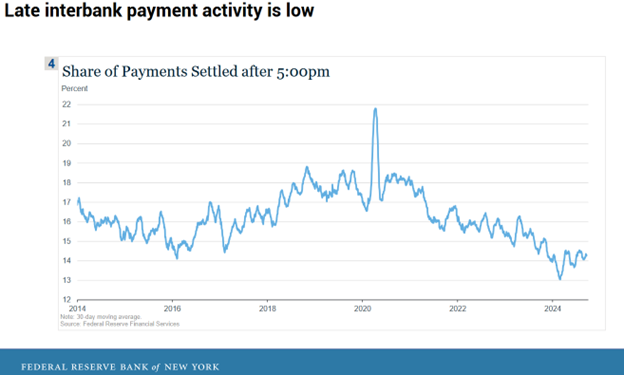

Late Interbank Payments

The timing of interbank payments is another useful metric. When reserves, which are the settlement instrument for these payments, are less abundant, banks will tend to tactically delay payments to keep their balance from dropping to uncomfortably low levels in the middle of the day. Therefore, late payment activity may be a useful indicator of the ampleness of reserve supply.

The chart below doesn’t point to any financial stress.

Average Intraday Overdrafts

Daylight overdrafts occur when short-term shifts in payment activity result in a temporarily negative balance in a bank’s reserve account. Higher average overdrafts are an indication that reserves are harder to come by in amounts needed to facilitate payments without intraday credit from the Federal Reserve. While peak intraday overdraft activity has occasionally spiked, average overdrafts have remained low and actually have declined in recent months.

The average remains near ten-year lows, thus denoting little to no stress.

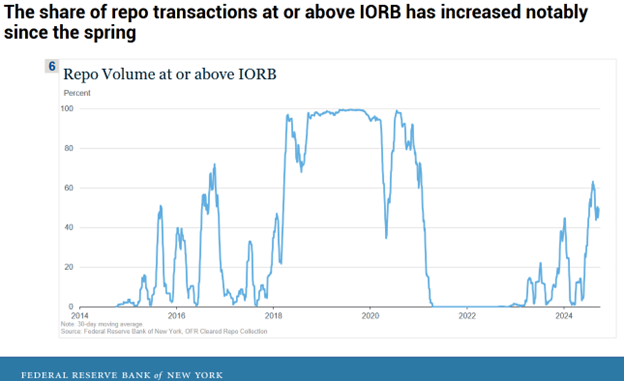

Repo Market Pressure

Three of Perli’s gauges are focused on the Fed Funds rate. Accordingly, it’s important to monitor factors that may impact that rate. This next gauge indicates that the Fed Funds gauges could start causing those measures to change.

Because repo is collateralized, it should generally trade at or below the uncollateralized IORB rate. Thus, if many transactions occur at a premium to IORB, there could be a problem. That is the case, as the graph below shows. But Perli helps explain why this is occurring and why it may not be problematic.

In recent years, there has obviously been a large increase in securities issued by the Treasury. And while there is no lack of demand for those securities, many investors need financing to acquire them. The ongoing shrinking of the Federal Reserve’s SOMA portfolio also contributes to the higher demand for repo financing because it results in private investors absorbing (and potentially financing) more Treasury securities. But it also contributes to a diminished supply of repo financing because a smaller SOMA portfolio implies that less overall liquidity is available to the financial system.

There appears to be also a second important cause for higher repo rates—namely, frictions that have developed in the market that are interfering with the liquidity redistribution process….In other words, repo supply can be limited by counterparty risk limits.

2018-2019

In the graphs above, reserves started to show stress in 2018 and 2019. If you recall, in September 2019, liquidity dried up, and the repo market essentially broke. Despite stable financial markets and a solid economy, the Fed had to provide liquidity/reserves to the banking system via lower rates and QE.

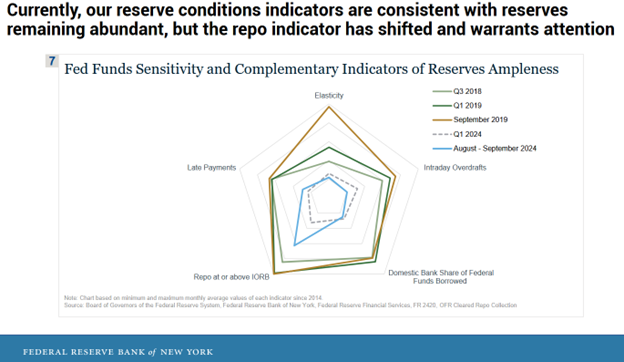

The current situation does not show the same slow degradation in liquidity conditions as we saw in 2018 and 2019. We share the graph below summarizing the Fed gauges to highlight the difference further. The closer to the center of the circle represents the most abundant reserve conditions. Conversely, as you move out, reserves become scarce.

Comparing the current conditions (blue) to those in September 2019 (gold) highlights that reserves are abundant today. But will that change rapidly with the RRP balances no longer providing a ballast?

Related: Trump’s Crypto Reserve: A Game-Changer or Just an Industry Boost?