Trending

Written by: Meera Pandit

Sentiment towards real estate investing has been nothing but doom and gloom since the Fed began raising rates, but as the old adage goes, it’s always darkest before dawn. After a significant pricing reset, private real estate could be on the verge of a rebound due to a few key drivers:

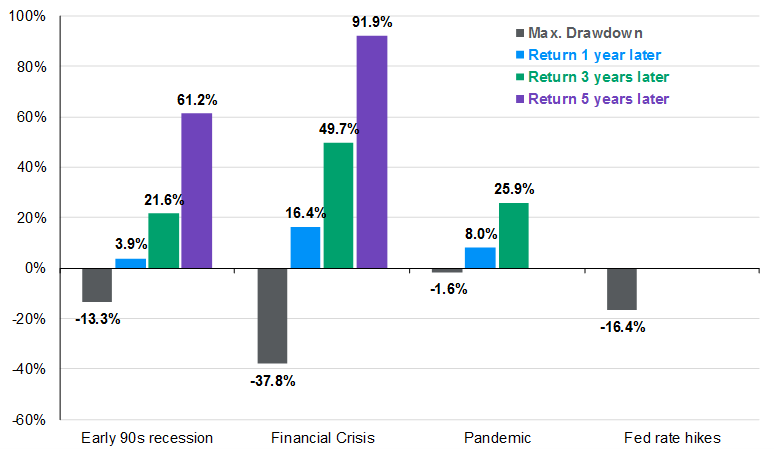

- Pricing dislocation – Real estate downturns have been surprisingly infrequent over the last 45 years. These downturns also tend to be short-lived compared to the period of appreciation between them. Of the three that have occurred since the late 1970s, they’ve lasted an average of 18 months, compared to the subsequent expansion of 110 months, with the pandemic experiencing just one calendar quarter of price depreciation compared to the 27 months of appreciation that followed. In addition, income not only provides cash flows to investors, but also serves as a buffer. Without it, there would have been periods of price declines during both the early and mid-80s, the tech wreck, and after Fed rate hikes in 2019. Instead, income offset those price declines. Public REITs typically rebound before direct real estate, and although the sample size is small, public REITs fell on average roughly 20%-pts more than direct real estate during the last three real estate downturns. Currently, direct real estate is down 16.4% from its peak, while REITs fell 31.4% from end of 2021 through October 2023. Therefore, pricing could be finding a floor in most sectors outside of office, presenting a compelling entry point. Of the three downturns since the late 1970s, all have been followed by robust subsequent returns, highlighted in the chart below.

- Rates – The sharp rise in interest rates has had a dramatic impact on real estate flows. Monthly fundraising of non-listed REITs fell two-thirds over the course of 2022, and average monthly fundraising fell 69% from 2022 to 2023. However, declines began to plateau in 2H23 as the Fed paused. Historically, excluding large fund raises into newly launched non-listed REITs, the category saw a drop in fundraising of 32% in 2018 as the Fed finished raising rates, but then a swift reversal back to 2017 levels when the Fed cut in 2019. If the Fed cuts rates this year, a similar reversal could occur.

- Investor sentiment – Although it’s still early to tell, green shoots are emerging in investor sentiment. Gross fundraising in private real estate was up 40% in 4Q23, measured by the NCREIF ODCE index, which typically reflects institutional investors. An inflection in investor sentiment has presaged a recovery in performance in the past: In 4Q09, flows finally began to grow with a massive influx in 1Q10. Performance turned positive in 1Q10.

Real estate has been an effective source of stable income and diversification for portfolios over time. Although sentiment towards commercial real estate has been extremely pessimistic since the Fed began raising rates, the reset in pricing, lower rates on the horizon, and a forthcoming inflection point in investor sentiment could augur well for real estate ahead.

Direct real estate drawdowns and subsequent returns

NCREIF ODCE Total Return index, cumulative returns %

Source: NCREIF, J.P. Morgan Asset Management. Maximum drawdown peak to trough dates: Early 90s recession (9/30/1990-6/30/1993); Financial crisis (6/30/2008-12/31/2009); Pandemic (3/31/2020-6/30/2020); Fed rate hikes (9/30/22-current). Data through 12/30/2023.

Related: Exploring Opportunities Beyond the 'Magnificent 7' and Beyond U.S. Borders