Trending

The economic slowdown is understandably causing concern among investors. However, while slower growth in China will impact the global economy and financial markets, we think the short-term pain is necessary to avoid bigger problems down the road. China’s economy is in the early stages of a long-term transition away from an export-driven, investment-led model toward a more balanced one with more domestic consumption.

During these large transitions, slowing growth is almost inevitable and—from a long-term perspective—desirable.

A Much Bigger Economy Today…and One in Transition

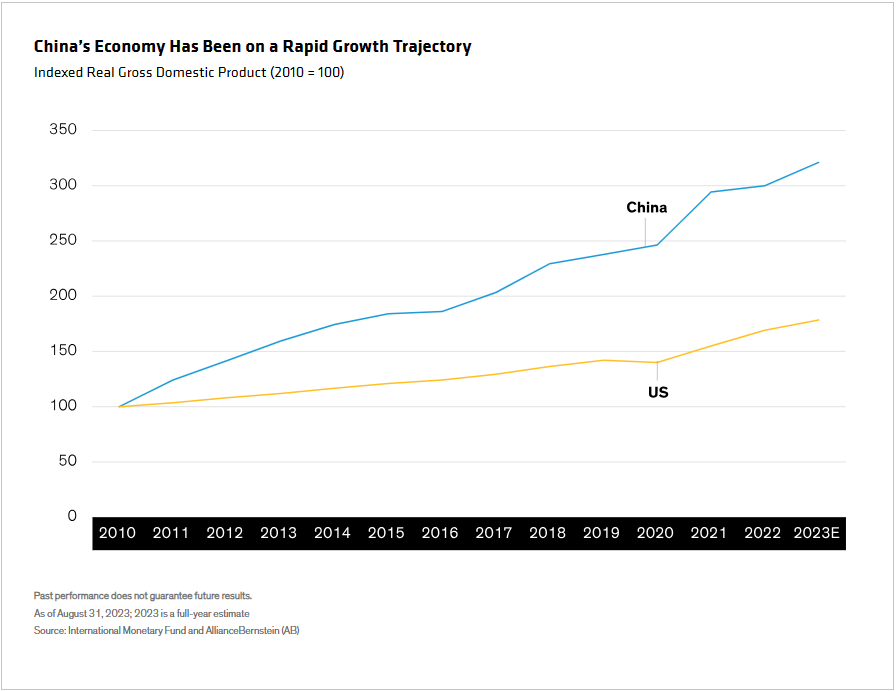

Part of the growth downshift is simple math. China’s economy has roughly tripled in size since the Global Financial Crisis (Display), making it much harder to sustain high growth rates. In fact, trying to boost growth could lead to excessive leverage and, in the case of China, overreliance on sectors with high economic multipliers, such as housing. That would only intensify existing imbalances in China’s system, so we believe that slower, but more sustainable growth is a healthier medium-term path.

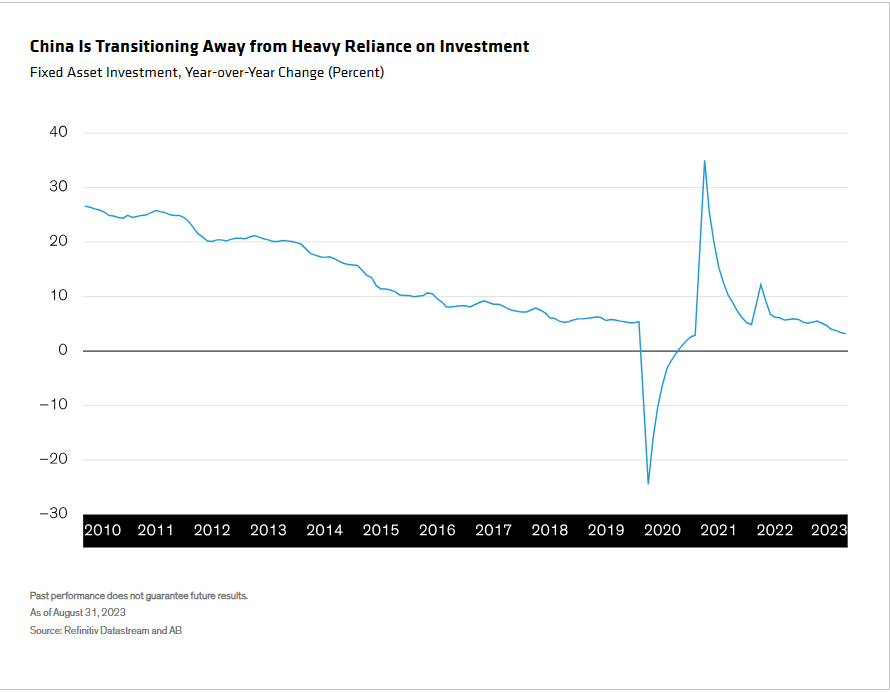

The other main driver of slower growth is the transition away from a heavier reliance on physical investment (Display) and exports toward a more balanced economic framework. Because so many resources have been devoted to these industries, they have excess capacity today. Trapped capital translates into lower prices as spare capacity is absorbed, and it results in slower growth as wasted, or wasting, resources are eliminated or redeployed.

Meanwhile, sectors with more positive medium-term outlooks continue to thrive, including consumer-facing staples, such as travel and restaurants. Solar and wind power projects are also humming, as are electric vehicle production and other high-tech and green products. It will take time for these industries to replace lost activity in real estate and heavy investment, which is why overall growth is slowing.

A Shift in Global Growth Dynamics

How should markets and the rest of the world process China’s growth outlook?

We think it’s important to avoid focusing too much on the government’s growth target—roughly 5% this year. Even if the economy grows at that pace, it won’t feel like “good” growth to those outside China. The country’s best-performing industries won’t likely fuel expansion abroad as much as they have before. It takes massive commodity imports to build roads and bridges; selling movie tickets and restaurant meals doesn’t.

All this means that China’s economy won’t be as big an engine of global growth as it’s been in the past. For markets, this evolution may seem disorienting—and is understandably causing jitters among many investors. Slower growth in the world’s second most important economy likely means lower overall global growth, even more so because China’s growth is becoming more domestically focused.

Expect Targeted, Gradual Stimulus

Much of the anxiety focuses on risks from the transition. Highly levered Chinese firms, particularly in property sectors, will likely feel stress, and policymakers won’t be inclined to deliver large-scale support, because it would exacerbate imbalances and delay the transition. Property-developer defaults could become severe enough to imperil the banking sector or local government finances—but that’s not our base case. The transmission mechanism from China’s financial system to the world is limited in direct terms, though turmoil in China could rattle sentiment elsewhere.

To sum things up, we share the view that China’s economy is slowing, and that slower growth will likely last as the economy transitions. There are also financial-market risks associated with that slowdown. But in our view, the “cure” to that problem—piling more debt and leverage onto the economy and property sector—would be worse than the ailment.

We think China’s policymakers feel the same way, so we expect targeted, gradual stimulus to manage the slowdown, not a “big bang” stimulus to push growth into a faster trajectory.

Related: Inflation Is Coming Down. Will Treasury Yields Be Next?