Trending

From a macroeconomic perspective, Friday’s bank earnings reports provide two important pieces of information. As we detail below, their profit margins are shrinking, and their economic outlook remains favorable.

JPM, C, and WFC reported paying depositors higher interest rates to retain their accounts. The consequence is a compression of their net interest income (NII), which weighs on the bank’s earnings. JPM, for instance, guided this coming year’s NII lower, blaming “deposit margin compression and lower deposit balances.” In layman’s terms, their current and future profit margins are shrinking. With banks less financially incentivized to lend to consumers and businesses, debt-driven economic growth will be less than it might have been had the banks been able to keep deposit rates lower. The inverted yield curve also pressures the bank’s NII and its earnings.

The second important macroeconomic takeaway is that bank loan loss reserves were mainly left unchanged. For example, JPM released $72 million in reserves, while WFC lowered its credit loss provision. This is an optimistic signal from the banks that they do not expect loan losses to increase in the coming quarters. Ergo, we can infer from the big bank’s earnings reports that they do not see a recession on the horizon.

What To Watch

Earnings

Economy

Market Trading Update

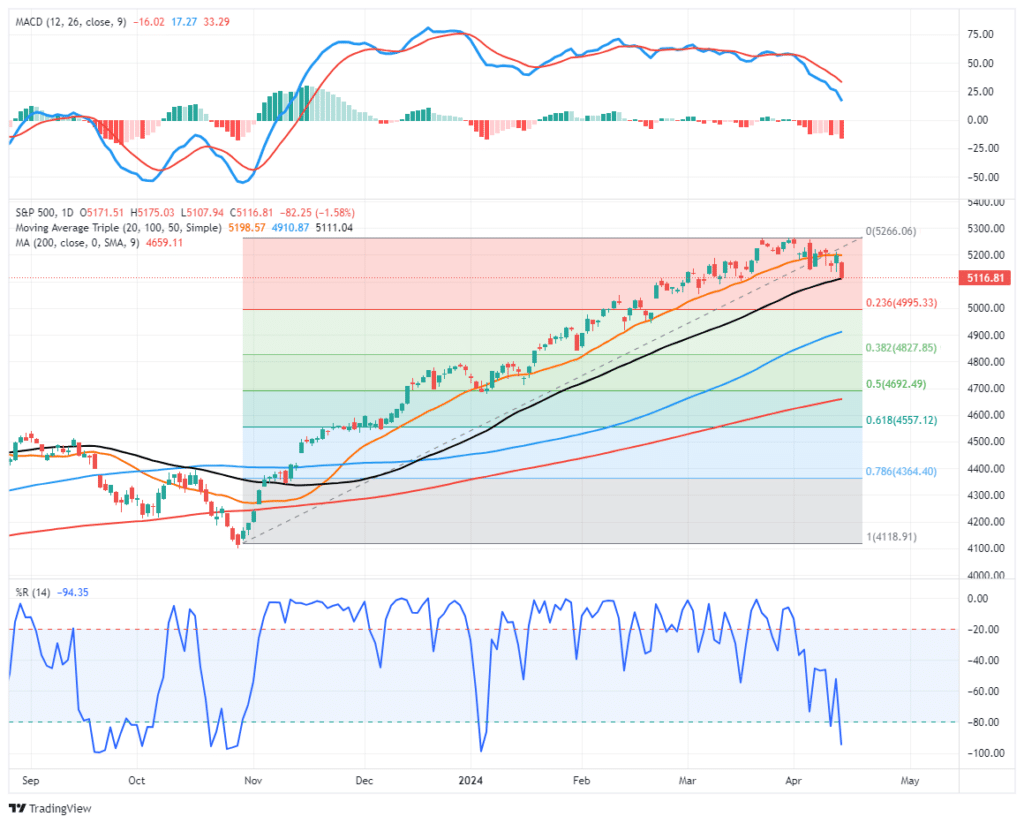

Last week, we discussed the current bullish trend’s ongoing, mind-numbing, narrow channel. We have suggested there was little to worry about until the market violates the 20-DMA. That “crack” to this “unstoppable” bullish rally was confirmed on Friday. As we noted last week:

“However, as we previously noted, just because the market breaks the 20-DMA does not mean we must take immediate action. What we need to see is a confirmation of that break with either a failed retest of previous support or a further decline. If the market is lower on Monday and takes out Thursday’s low, as shown, this would confirm the break of support and suggest lower prices. The 50-DMA will quickly become the next significant support level.”

As shown, the market broke below the previous Thursday’s low on Friday after failing a retest of the previous support at the 20-DMA. This turns the previous 20-DMA into resistance and makes the 50-DMA key support over the next few days. (Note: If the market makes a confirmed break of the 50-DMA, the 100- and 200-DMAs become the next logical targets.)

The market is oversold enough for a bounce early next week that investors should use to make further adjustments to portfolio allocations. Crucially, this signal DOES NOT mean to “sell everything and go to cash.”

The confirmed break of support suggests reviewing portfolio allocations and taking profits in well-performing positions. However, while some stocks have only begun to correct from previously overbought conditions, many have already corrected by 10% or more over the last few weeks. Those companies may see inflows as a rotation trade in the market occurs.

In other words, as is always the case, be careful “throwing the baby out with the bathwater.” Opportunities to acquire better-priced companies always exist, even during a corrective process.

The Week Ahead

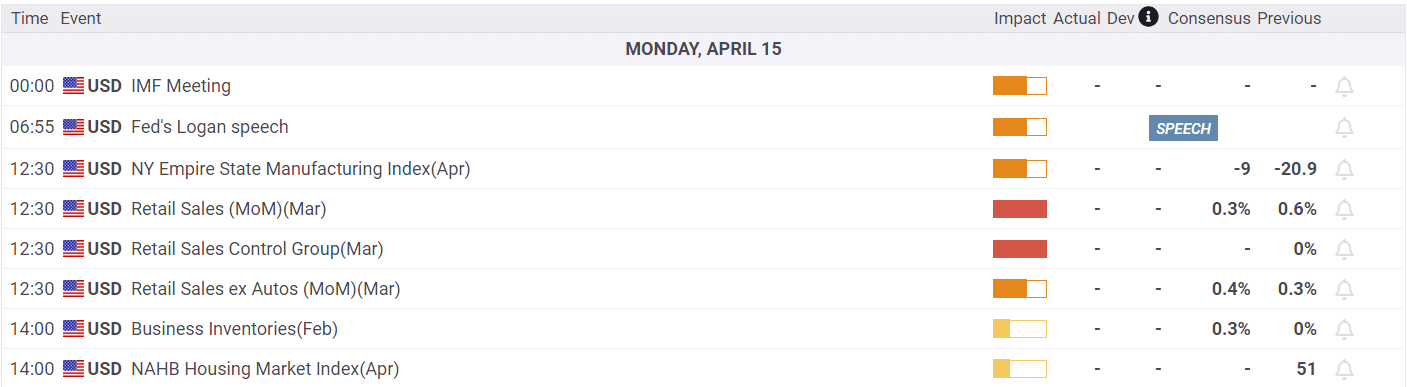

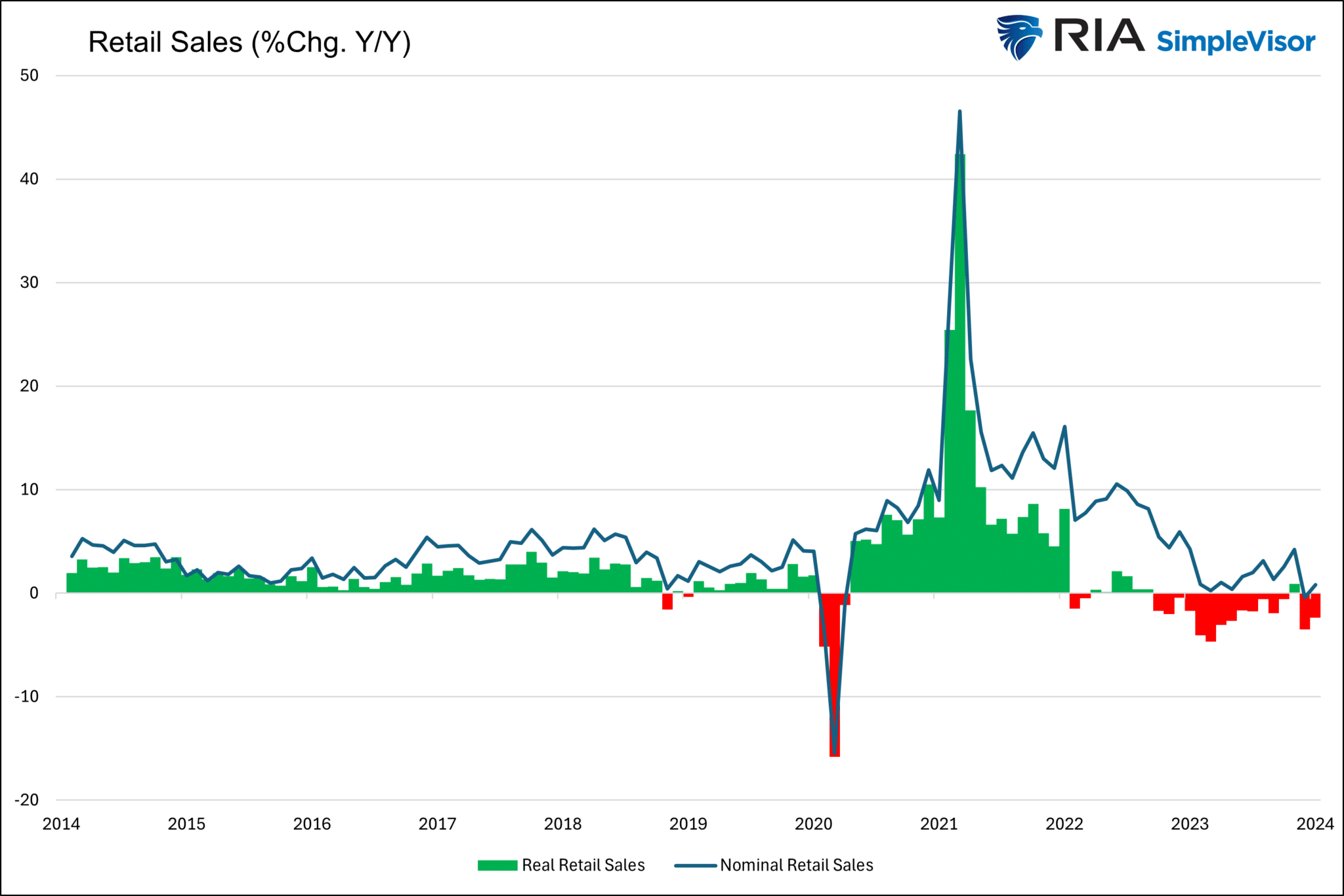

This morning’s retail sales report will help shed light on personal consumption. Since September, retail sales have declined slightly while up slightly on a year-over-year basis, as shown below. The green and red bars show retail sales adjusted for inflation. As shown below, real retail sales have been declining for the better part of the last two years. Given personal consumption accounts for two-thirds of economic activity, the data set is not in sync with robust GDP growth.

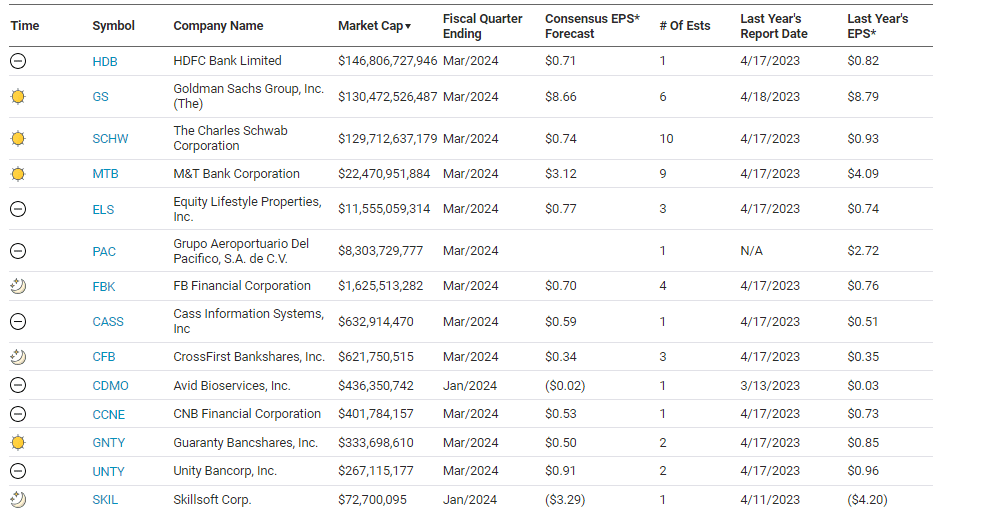

Earnings will take center stage this week. Goldman Sachs, Bank of America, Morgan Stanley, and the regional banks’ earnings reports will further affirm our thoughts in the opening paragraphs. UnitedHealth, J&J, Abbot Labs, NetFlix, and Proctor & Gamble are among the largest non-financial stocks reporting this week.

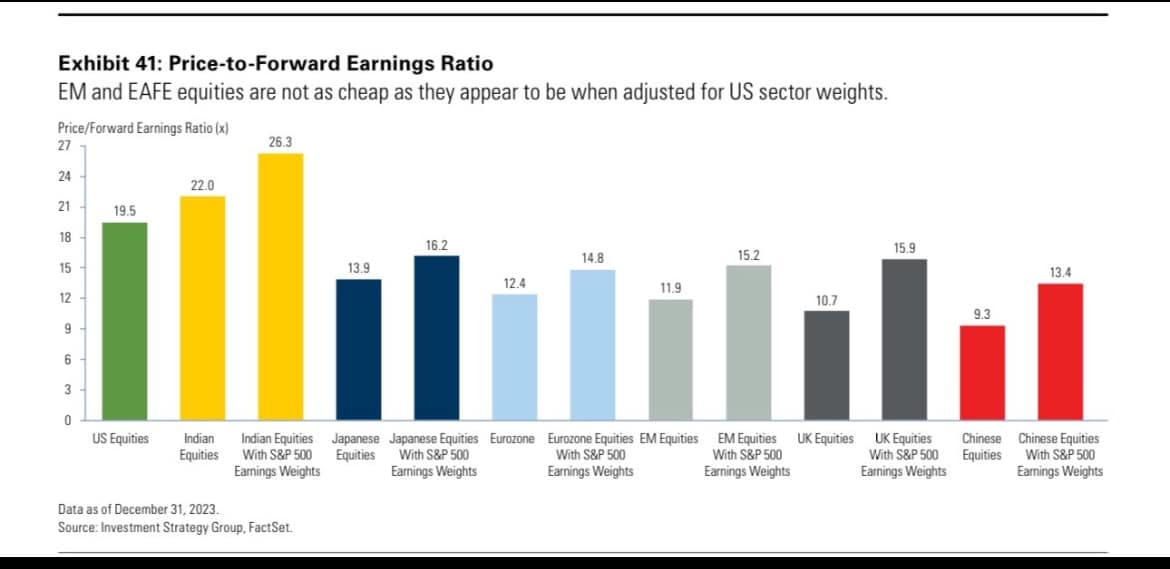

Are Foreign Stocks Really That Cheap Versus American Shares?

Quite often, a financial pundit will argue that foreign stocks offer much more value than U.S. stocks. A cursory glance at valuations would certainly affirm such a view. However, what they often fail to mention is that the sector composition of foreign indexes is different from that of the S&P 500. For instance, the Japanese Nikkei stock index has an approximate 24% weighting to the technology sector, while the S&P 500 has a 30% weighting. Given that valuations are much higher for technology companies in aggregate than other industries, differences in composition, even if minor, can have a big difference.

The graph below from the Investment Strategy Group compares the valuations as they are reported and when adjusted for the S&P 500 weights. Based on the adjusted valuations, the S&P 500 is still richer than the other indexes, but not nearly as much as their unadjusted valuations would lead us to believe.

Tweet of the Day

“Want to have better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”