Trending

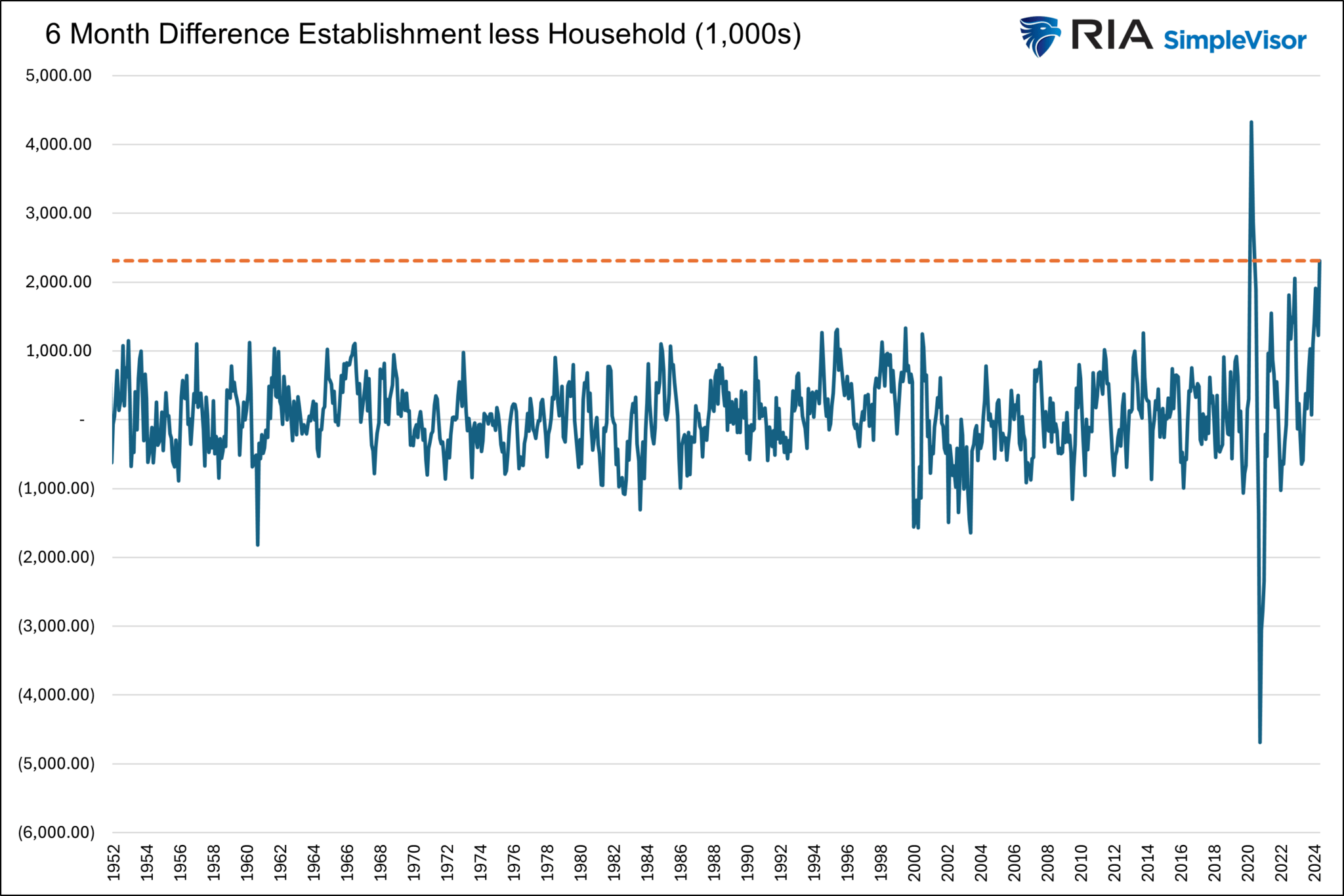

The BLS jobs report showed the economy added 272k jobs, well above expectations of 175k, and the 152k jobs reported by ADP. Also pointing to a strong labor market, average hourly earnings were 0.1% above expectations at +0.4%. While the jobs data seems strong, there is a lot of other data within the report, leading us to question its veracity. For starters, the unemployment rose from 3.9% to 4.0%. While the economy did add jobs per the establishment survey, the unemployment rate calculation uses the household survey. That shows the number of employed people fell by 408k. Further, the participation rate dropped from 62.7% to 62.5%. The graph below shows that over the last six months, the headline-garnering establishment survey has added 2.3 million more jobs than the household survey. Such dwarfs any divergence since the pandemic.

The quality of jobs also has a lot to be desired. The number of full-time jobs fell by 625k while part-time jobs rose by 286k. Such is the biggest drop in full-time employment since last December. Furthermore, the number of people with multiple jobs is now 8.4 million, which is just below a record high. The report also highlights why economic survey results, including Democrats, show dismay at Biden’s economic performance. In just May alone, 414k legal and illegal immigrants gained a job. Meanwhile, 663k native-born Americans lost their jobs. Since the pandemic, native-born workers have lost around 2 million jobs.

The bond market’s initial reaction was very negative due to the strong headline job growth and hourly earnings beat. However, we think that over the next few days, as the market digests the complete set of jobs data, it may feel otherwise. Remember that the coming CPI, FOMC meetings, and Treasury bond auctions also weigh on bonds.

Market Trading Update

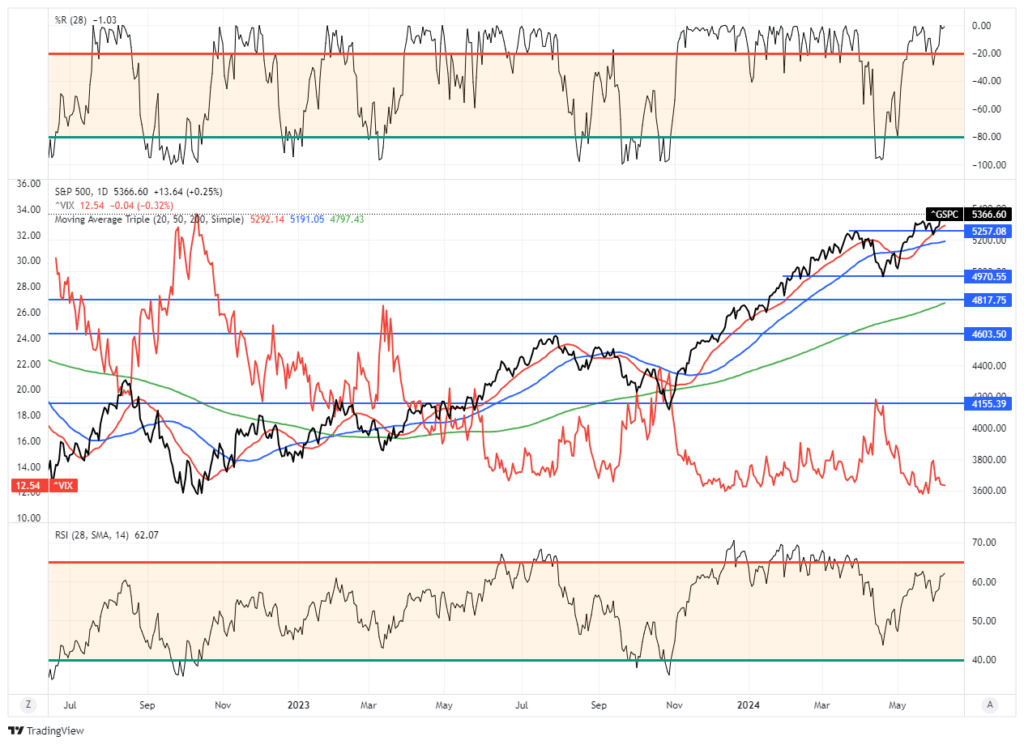

Last week, we noted that the market remains range-bound within the recent consolidation. To wit:

“Crucially, the market has now registered a ‘sell signal,’ which will limit any rallies in the near term. Therefore, investors should continue to use bounces to reduce exposure and rebalance portfolios as needed. The upside to the market is likely constrained to recent highs.“

While the market set marginal new all-time highs this past week, the upside likely remains somewhat limited in the near term, given the more overbought conditions. On Friday, the market flipped back onto a MACD “buy signal,” suggesting that the rally remains firmly intact, with the 20-DMA continuing to act as the primary support. Furthermore, volatility remains very suppressed, suggesting that traders are not worried about a significant decline anytime soon. However, with that said, the FOMC meeting and inflation reports are next week, which will have an outsized impact on the broader market. Therefore, continue to manage risk accordingly.

While the market did sell off early on Friday with the strong headline report, the underlying data strongly suggests that employment is much weaker than headlines suggest. For the Federal Reserve and the upcoming FOMC meeting next week, the 4% unemployment rate will likely keep them focused on the risk to the economy and on track to cut rates this year.

Such should continue to a bid under the market for now.

The Week Ahead

This will be a very busy week with lots of information for investors to digest. Wednesday, in particular, could be volatile, with CPI being released at 8:30 am ET, followed by the FOMC at 2:00 pm ET. The market expects CPI to be 0.3% on a monthly basis. Little is expected of the Fed, although it will be interesting to see if they shift their view on the economy to a slightly weaker outlook based on recent data. Jerome Powell may share his thoughts on Friday’s employment report. Given that the Philadelphia Fed expects a significant downward revision of employment figures, he may offer that the jobs market is not as strong as the headlines portray. We look forward to hearing his thoughts on the recent rate cuts by the ECB and Bank of Canada.

Also, this week, the 10-year UST auction will be held on Tuesday, and the 30-year auction will be held on Thursday. Like CPI, PPI on Thursday is expected to rise +0.3%.

Housing Struggles

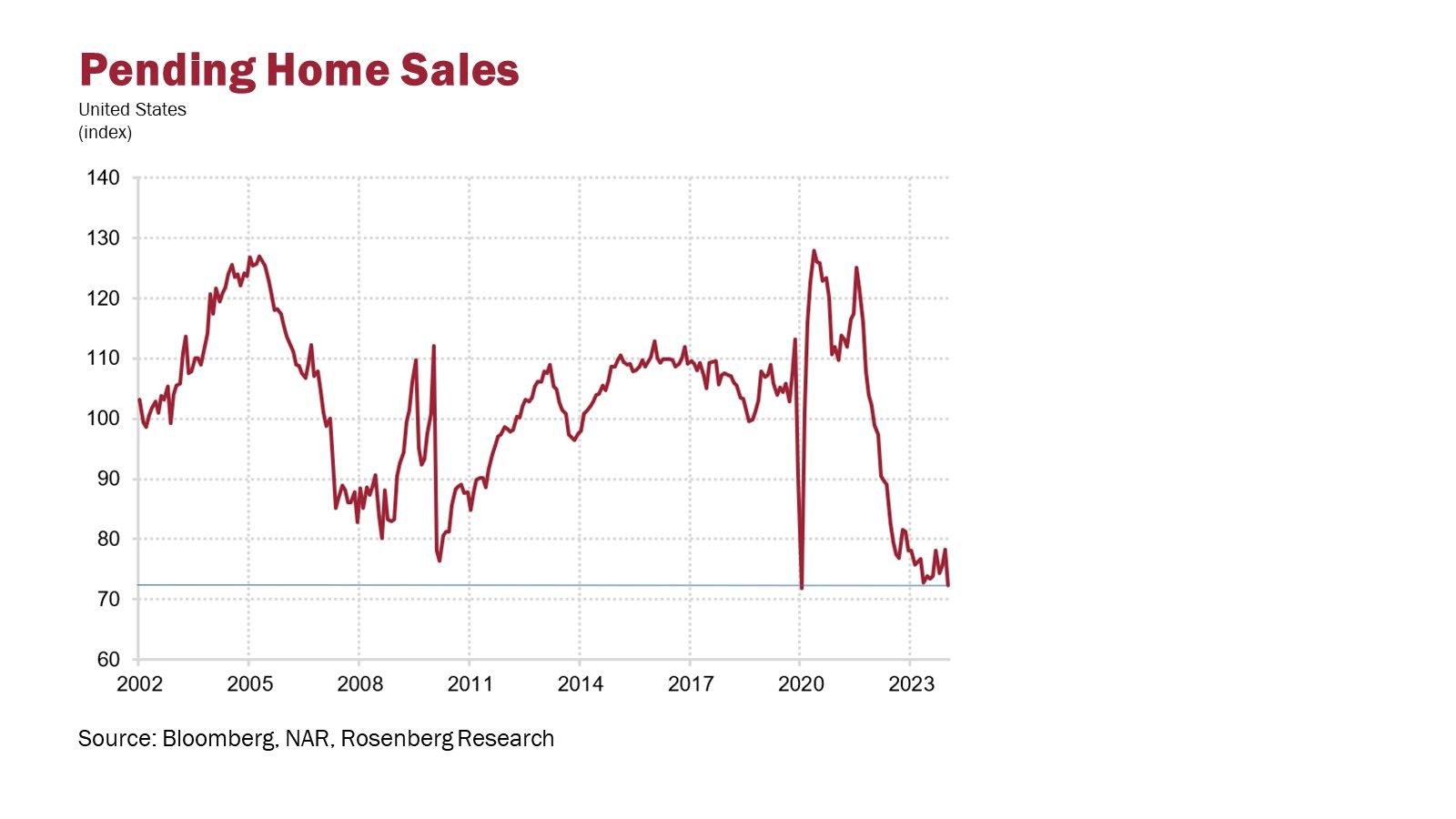

Not surprisingly, with almost two years of mortgage rates north of 7%, the existing home market has been struggling. Buyers are few and far between as high prices and mortgage rates make home-buying difficult. Further, for many homeowners with sub-4 % mortgages, selling a home and buying a new home with much higher mortgage rates is not appealing. Sales for new homes have performed much better than those for existing homes as homebuilders have been offering customers reduced-rate mortgages. The graphs below show us that both the new and existing markets are essentially shut down.

The first graph shows pending home sales. They are homes under contract but have yet to go to settlement. Last month, they declined 7.7% compared to the prior month. Furthermore, they are down 7.4% versus one year ago. Most stunning, the index is at the same level as in April of 2020, when COVID essentially closed the real estate market. Home sales track very closely with pending home sales.

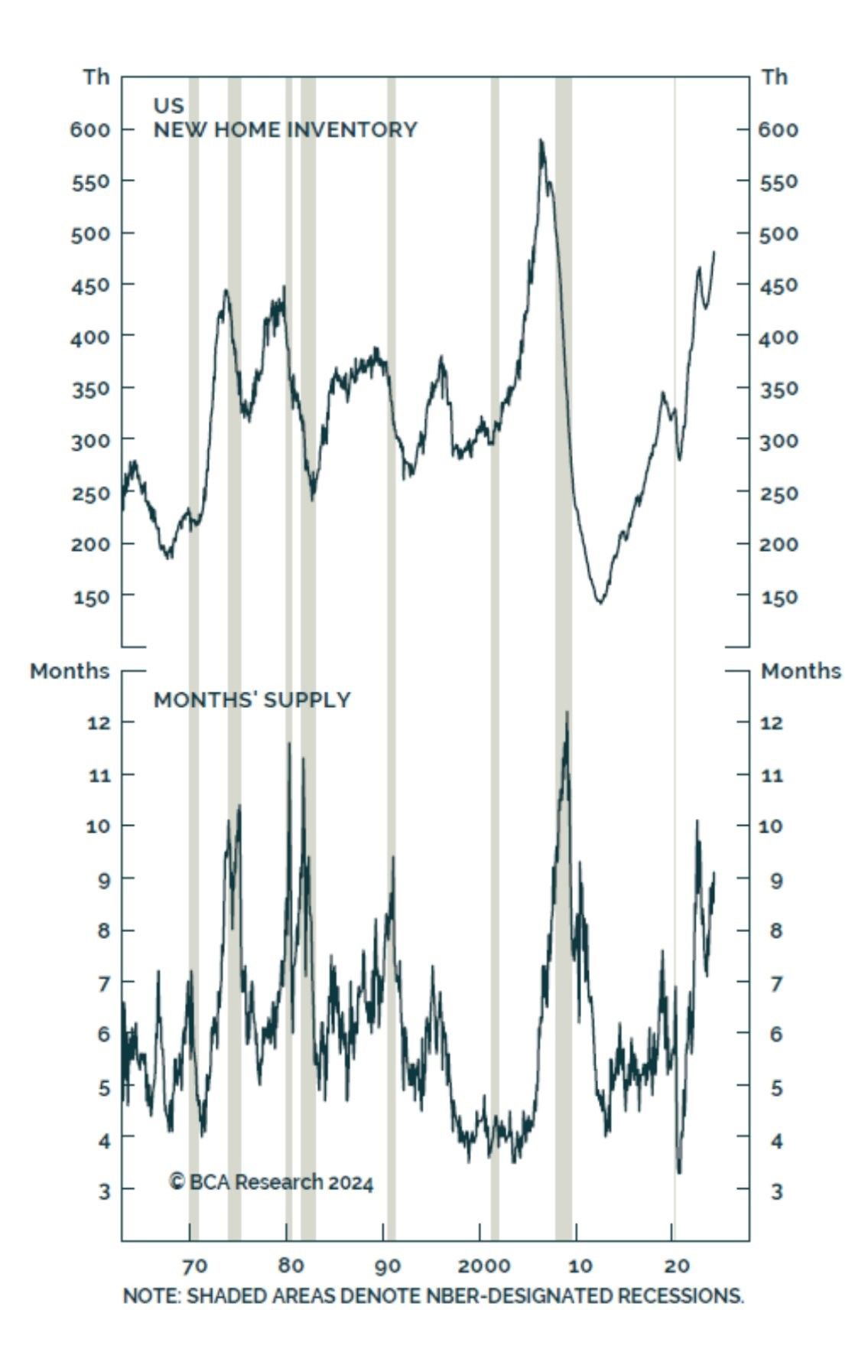

The second graph shows that the supply of new homes is rising and approaching the 2008 highs. The lower graph measures the supply slightly differently.

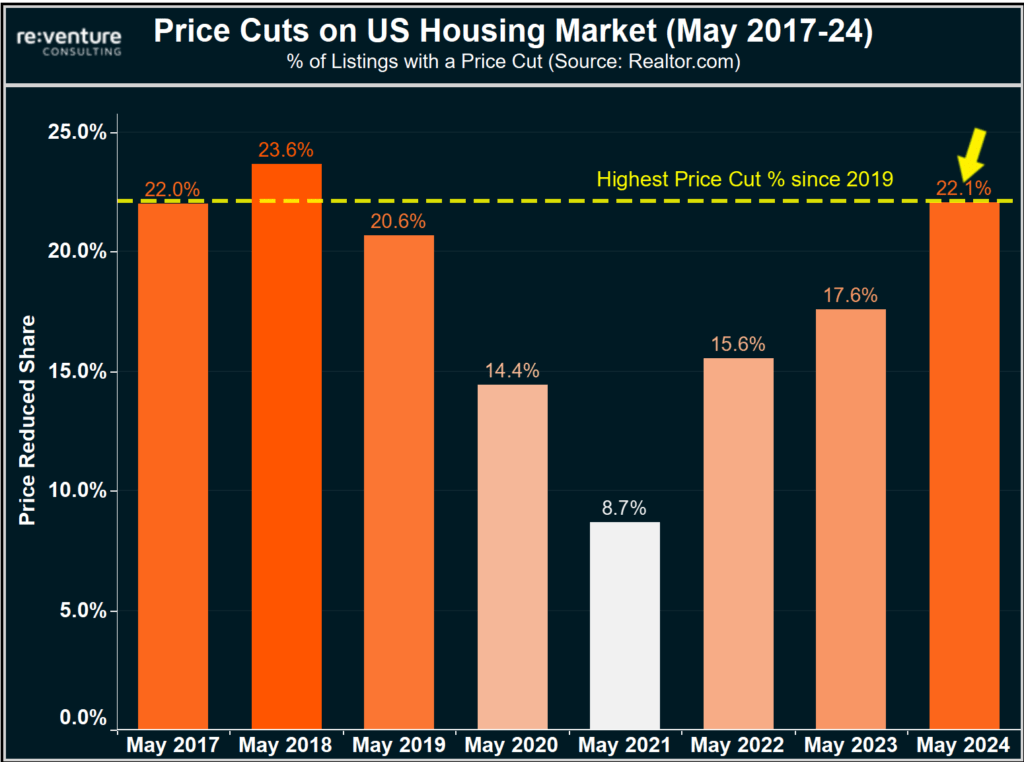

The final graph is important as it shows that the balance between supply and demand for homes may be shifting. Before recently, home prices have remained relatively stable despite high mortgage rates. This is largely a function of the small number of sellers in the market. However, as the third graph shows, price cuts to entice borrowers are becoming more popular. In fact, the percentage of listings with a price cut is back to pre-pandemic levels.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Related: Commodities and the Boom-Bust Cycle