Trending

Heading into last Friday’s BLS employment report, the Fed Funds futures market put equal odds of the Fed cutting by 25 bps or 50 bps. Most economists thought the employment report would answer the question of whether they will cut by 25 bps or 50 bps at the September 18th FOMC meeting.

The BLS employment report was weak but not awful. As a result, as shown below, the market remains in limbo. Accordingly, this Wednesday’s CPI report may persuade the market toward 50 bps or 25 bps.

Per the BLS report, payrolls increased by 142k, below expectations of 165k. However, the prior two months were revised lower by 86k. The unemployment rate fell to 4.2% from 4.3% as expected. Important to the Fed, hourly earnings rose by 0.4%, a tenth more than expectations. However, the prior month was revised downward by 0.3% to -0.1%. The latest BLS and ADP data, taken in stride with the monthly and outsized annual -880k revisions a few weeks ago, clearly shows the labor market is weakening. But is it weakening enough for the Fed to justify cutting rates by 50 bps?

What To Watch

Earnings

Economy

- No notable economic releases today.

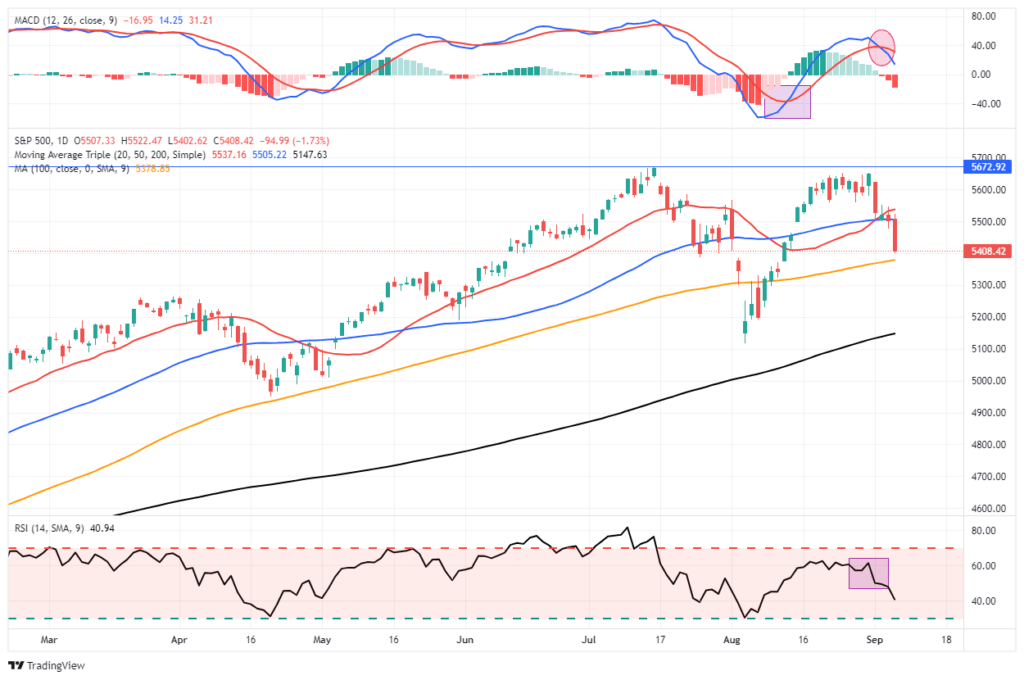

Market Trading Update

“This past week, the market struggled to make gains, and as shown, its momentum has slowed. While such does not mean a significant correction is imminent, it does suggest that the upside is likely limited. Investors should expect a continued consolidation or pullback to previous support levels. Notably, a negative divergence is developing between momentum, strength indications, and market performance. We last mentioned such a negative divergence was in late July before the August correction.”

This past week, slowing economic data and a weak payroll report weighed on market sentiment, pushing the market below initial support levels at the 20—and 50-DMA. That suggests that the current correction process that began in early August is continuing ahead of the upcoming November election.

As discussed this past Tuesday in “Risks Facing Bullish Investors,” an essential “buyer” for the market is fading with the corporate buyback window closing. Such increases the risk of a pickup in volatility over the next two months, which coincides with a potentially contentious election that will likely keep major investors sidelined.

In the short term, the weekly technical gauge shows the recent correction resolved much of the previous overbought conditions. That sets the market up for a reflexive rally early next week.

We suggest using any rally that fails to regain the 50-DMA to reduce risks, rebalance portfolios, and raise cash levels. While the potential downside is not significant, the goal is not to sacrifice a substantial amount of recent gains or put yourself in a position of being forced to sell for any reason.

Remain cautious for now. Following the election, we will likely have significantly more clarity about where the market is heading next.

The Week Ahead

With employment data behind us, we turn to inflation to help us assess whether the Fed will cut by 25 bps or 50 bps. This week’s data features CPI on Wednesday, PPI on Thursday, and Import/Export prices and University of Michigan inflation expectations on Friday. The current market expectation for CPI is an increase of 0.2%. The graph below shows that monthly inflation rates have been slightly higher than in the three years before the pandemic. However, the average change over the last six months aligns more with pre-pandemic levels.

Also on the calendar are the 10- and 30-year UST auctions. With bonds trading much better over the last few months, demand should be decent; thus, volatility related to the auctions will likely be less than we have witnessed over the past few years.

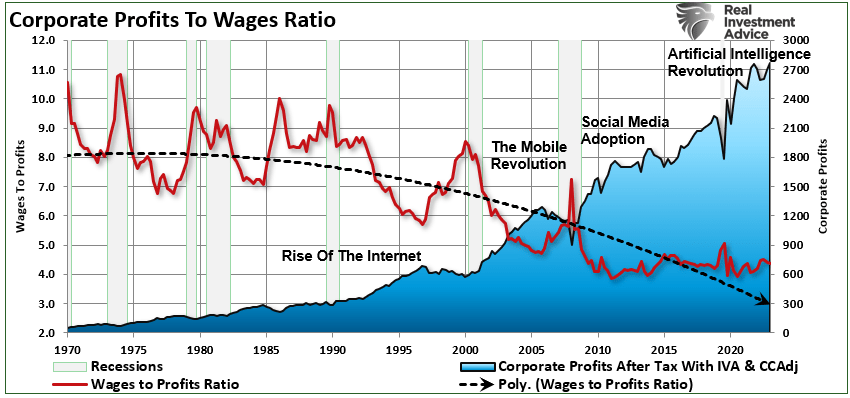

Technological Advances Make Things Better – Or Does It?

While technological advances seem to produce an enormous benefit, a dark side gets hidden from public discourse.

One primary concern is job displacement. Automation and artificial intelligence, while improving efficiency, often replace jobs traditionally performed by humans. This displacement mainly affects low-skilled workers in industries like manufacturing and retail, leading to unemployment and underemployment. As machines take over routine tasks, the workforce faces the challenge of reskilling to meet the demands of a more technologically advanced economy. That transition period can lead to economic slowdowns and increased inequality, as not all workers have the means or opportunity to adapt quickly.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”