Trending

Written By: David Trainer Last week we featured three safe stocks to get you through a bear market . This week we’re going in the opposite direction and picking three stocks that have performed well in 2018 but look overvalued as the market grows more volatile.Advanced Micro Devices (AMD: $20/share), TripAdvisor (TRIP: $62/share), and Advance Auto Parts (AAP: $166/share) are this week’s Danger Zone picks.

Price Increase Leads to Overvaluation

It should come as no surprise that many of the top-performing S&P 500 stocks for 2018 now earn our Unattractive-or-worse rating. Anytime a stock nearly doubles in one year, there’s a good chance it will become overvalued.Figure 1 shows the year to date (YTD) performance and the price to economic book value ( PEBV) for the top three performing stocks in the S&P 500 so far this year. Economic book value represents the zero-growth value of a company’s cash flows, so all three companies have a valuation at least four times higher than their zero-growth value. For comparison, the weighted-average PEBV for the S&P 500 is 2.6.Figure 1: Three Stocks to Sell Before a Bear Market

Image Source: New Constructs, LLCSources: New Constructs, LLC and company filingsIn addition, these three stocks also share a few other traits, including:

Image Source: New Constructs, LLCSources: New Constructs, LLC and company filingsIn addition, these three stocks also share a few other traits, including:Advanced Micro Devices (AMD)

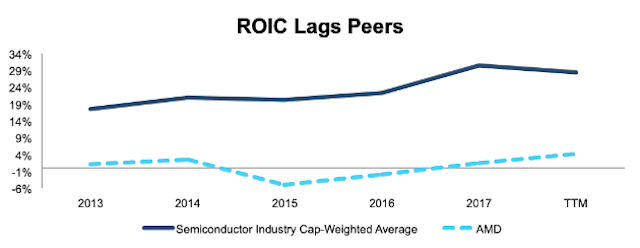

Advanced Micro Devices AMD[NGS] - $19.00 is a global semiconductor company. The company is one of the smaller players in most of its product lines, except for graphics processing units (GPU’s), where it operates in a virtual duopoly with Nvidia NVDA[NGS] - $136.19.AMD drastically outperformed the market this year as it took GPU market share away from NVDA and analysts perceived opportunities for the company to capitalize on struggles at Intel INTC[NGS] - $47.22 . Reported earnings growth also helped drive the stock increase, as GAAP EPS increased 546% TTM to $0.32/share.However, GAAP earnings growth is overstated due to a $19 million one-time gain from tax reform (5% of GAAP net income) and understated earnings in the previous TTM period. Net operating profit after tax ( NOPAT) grew by 36% TTM, still impressive, but not as big an improvement as GAAP EPS.More importantly, even after its fundamental improvement, AMD remains at a significant disadvantage to its peers. Figure 2 shows that AMD’s ROIC remains significantly below the rest of the semiconductor industry.Figure 2: ROIC Since 2013: AMD Vs. Semiconductor Industry

Image Source: New Constructs, LLCSources: New Constructs, LLC and company filingsOn top of its inferior profitability, AMD’s valuation implies an unrealistic level of future profit growth. In order to justify its valuation of ~$17/share, AMD must immediately increase its pre-tax margins from 8% to 30% (in line with industry leaders like INTC) and grow NOPAT by 42% compounded annually for 10 years. See the math behind this dynamic DCF scenario.We believe that level of growth and profitability will be incredibly difficult, especially with the prospect of the crypto-bubble bursting leading to decreased demand for GPU’s. These concerns have already driven AMD down 30% over the past three months, and we think that decline could continue.Even if AMD doubles its pre-tax margins to 15% and grows NOPAT by 33% compounded annually for 10 years, the stock is worth just $10/share today – a 41% downside from the current stock price. See the math behind this dynamic DCF scenario.

Image Source: New Constructs, LLCSources: New Constructs, LLC and company filingsOn top of its inferior profitability, AMD’s valuation implies an unrealistic level of future profit growth. In order to justify its valuation of ~$17/share, AMD must immediately increase its pre-tax margins from 8% to 30% (in line with industry leaders like INTC) and grow NOPAT by 42% compounded annually for 10 years. See the math behind this dynamic DCF scenario.We believe that level of growth and profitability will be incredibly difficult, especially with the prospect of the crypto-bubble bursting leading to decreased demand for GPU’s. These concerns have already driven AMD down 30% over the past three months, and we think that decline could continue.Even if AMD doubles its pre-tax margins to 15% and grows NOPAT by 33% compounded annually for 10 years, the stock is worth just $10/share today – a 41% downside from the current stock price. See the math behind this dynamic DCF scenario.TripAdvisor (TRIP)

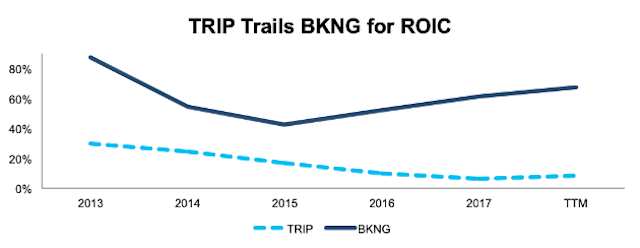

TripAdvisor TRIP[NGS] - $53.92 is an online travel company that features reviews and recommendations for hotels, restaurants, and attractions around the world.TRIP’s presence on this list stands in contrast to Booking Holdings BKNG[NGS] - $1,717.55 , another travel site which we recently featured in our article “ Safe Stocks for a Bear Market”. TRIP and BKNG operate on two sides of the travel industry. TRIP focuses on reviews and recommendations, whereas BKNG handles the actual payment and reservations. The two companies compete for pageviews while at the same time partnering to serve customers, as visitors to TripAdvisor can book tickets for hotels through Booking.TRIP’s 82% YTD gain comes not from any major increase in demand or market share, as revenues are up just 3% TTM. Instead, the company has significantly improved its margins. TRIP’s NOPAT margin is up from 6% in 2017 to 8% TTM.The major driver of this improvement comes from decreased spending on sales and marketing. In Q3 2018, TRIP spent 45% of revenue on sales and marketing compared to 56% in Q3 2017. In addition, TRIP is overstating its profit growth through the use of non-GAAP metrics that exclude real costs such as stock-based compensation. Through the first nine months of 2018, TRIP reports that non-GAAP net income increased 46%, but NOPAT is up just 32% TTM.Even with its profitability improvements, TRIP remains well below BKNG in terms of ROIC, as shown in Figure 3. TRIP bills itself as “the world’s largest travel site based on monthly unique visitors,” but it’s clear that BKNG is better at monetizing its user base.Figure 3: ROIC Since 2013: TRIP Vs. BKNG

Image Source: New Constructs, LLCSources: New Constructs, LLC and company filingsIn order to justify its valuation of ~$51/share, TRIP must immediately improve its pre-tax margins from 11% to 35%, in line with BKNG, and grow NOPAT by 24% compounded annually for 10 years. See the math behind this dynamic DCF scenario.It appears as if the market is valuing TRIP and BKNG based on eyeballs instead of cash flows. We think that in a bear market, cash is going to matter much more.If TRIP only improves margins to 20%, which it achieved in 2015, and grows NOPAT by 20% compounded annually for 10 years, the stock is worth $38/share today – a 25% downside from the current stock price. See the math behind this dynamic DCF scenario.Related: 2019: The Beginning of the End

Image Source: New Constructs, LLCSources: New Constructs, LLC and company filingsIn order to justify its valuation of ~$51/share, TRIP must immediately improve its pre-tax margins from 11% to 35%, in line with BKNG, and grow NOPAT by 24% compounded annually for 10 years. See the math behind this dynamic DCF scenario.It appears as if the market is valuing TRIP and BKNG based on eyeballs instead of cash flows. We think that in a bear market, cash is going to matter much more.If TRIP only improves margins to 20%, which it achieved in 2015, and grows NOPAT by 20% compounded annually for 10 years, the stock is worth $38/share today – a 25% downside from the current stock price. See the math behind this dynamic DCF scenario.Related: 2019: The Beginning of the EndAdvance Auto Parts (AAP)

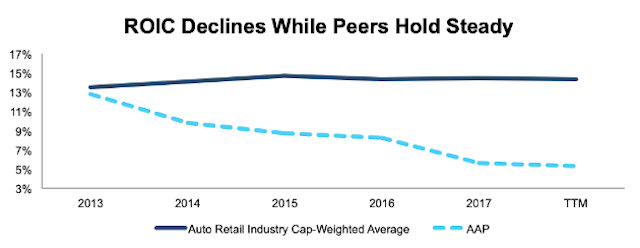

Advance Auto Parts AAP[NYE] - $158.81 operates ~5,200 stores throughout North America selling auto parts and accessories 2018 has been a bounce back year after the stock was one of the S&P 500’s worst performers in 2017, declining 41%.However, AAP’s earnings beats have been driven in large part by accounting head fakes. The company had a one-time $144 million benefit from tax reform, as well as a $45 million TTM gain from changes in LIFO reserves. Combined, these two items accounted for 34% of GAAP net income. Add in the company buying back $126 million (1% of market cap) in shares in the most recent quarter, and AAP manufactured 58% TTM GAAP EPS growth even as NOPAT declined 25%.As Figure 4 shows, this decline is part of a long-term trend. AAP’s ROIC has declined every year since 2011, even as the rest of its industry has maintained a consistent level of profitability.Figure 4: ROIC Since 2013: AAP Vs. Auto & Parts Retail

Image Source: New Constructs, LLCSources: New Constructs, LLC and company filingsThe auto parts industry faces significant competitive pressure in the near future as large brick-and-mortar retailers, along with Amazon AMZN[NGS] - $1,575.39, try to push their way into the market. AAP has already begun cannibalizing its own business by partnering with Walmart WMT[NYE] to stave off the competitive pressure.When competition increases, the least profitable players tend to get squeezed out.Despite its growth in accounting earnings, AAP is significantly less profitable than competitors such as AutoZone AZO[NYE] - $835.63 or O’Reilly ORLY[NGS] - $341.82 .AAP’s high valuation only increases the risk of owning this stock. To justify its current valuation of ~$163/share, the company must increase its pre-tax margins from 7% to 10% (in-line with its 2015 margins) and grow NOPAT by 12% compounded annually for nine years. See the math behind this dynamic DCF scenario.If AAP’s margins pre-tax margins rebound to 9% (the weighted average of the past three years), and the company grows revenue at just 3% compounded annually for the next 10 years (in-line with projected industry growth rates), the stock is worth $114/share today – a 30% downside from the current stock price. See the math behind this dynamic DCF scenario.

Image Source: New Constructs, LLCSources: New Constructs, LLC and company filingsThe auto parts industry faces significant competitive pressure in the near future as large brick-and-mortar retailers, along with Amazon AMZN[NGS] - $1,575.39, try to push their way into the market. AAP has already begun cannibalizing its own business by partnering with Walmart WMT[NYE] to stave off the competitive pressure.When competition increases, the least profitable players tend to get squeezed out.Despite its growth in accounting earnings, AAP is significantly less profitable than competitors such as AutoZone AZO[NYE] - $835.63 or O’Reilly ORLY[NGS] - $341.82 .AAP’s high valuation only increases the risk of owning this stock. To justify its current valuation of ~$163/share, the company must increase its pre-tax margins from 7% to 10% (in-line with its 2015 margins) and grow NOPAT by 12% compounded annually for nine years. See the math behind this dynamic DCF scenario.If AAP’s margins pre-tax margins rebound to 9% (the weighted average of the past three years), and the company grows revenue at just 3% compounded annually for the next 10 years (in-line with projected industry growth rates), the stock is worth $114/share today – a 30% downside from the current stock price. See the math behind this dynamic DCF scenario.