Trending

During the last week of December, I polled my X followers for their outlook on the markets and the economy for 2024. The results were quite interesting, but before we look forward, we must look back at 2023 for context.

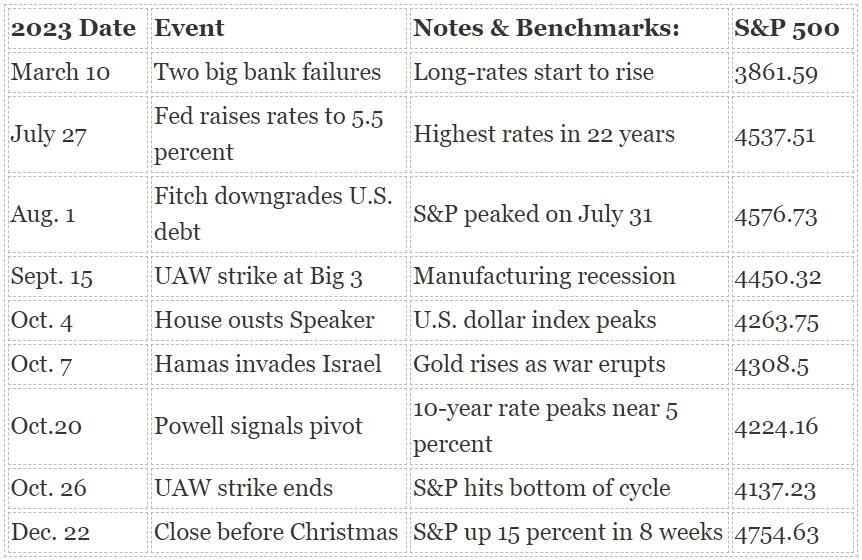

Last year was not what the majority of mainstream economists and analysts predicted. Going into last year, expectations for a recession and negative market returns were high. The table below shows some important events and market reactions during the previous year. Each one of those events was expected to disrupt the market.

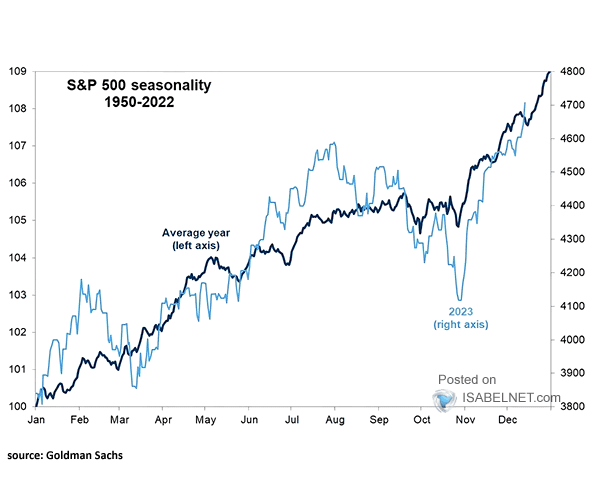

Yet, despite higher Fed funds rates, rising interest rates, bank failures, and fiscal concerns, the market closely followed the seasonal pattern of a pre-election year.

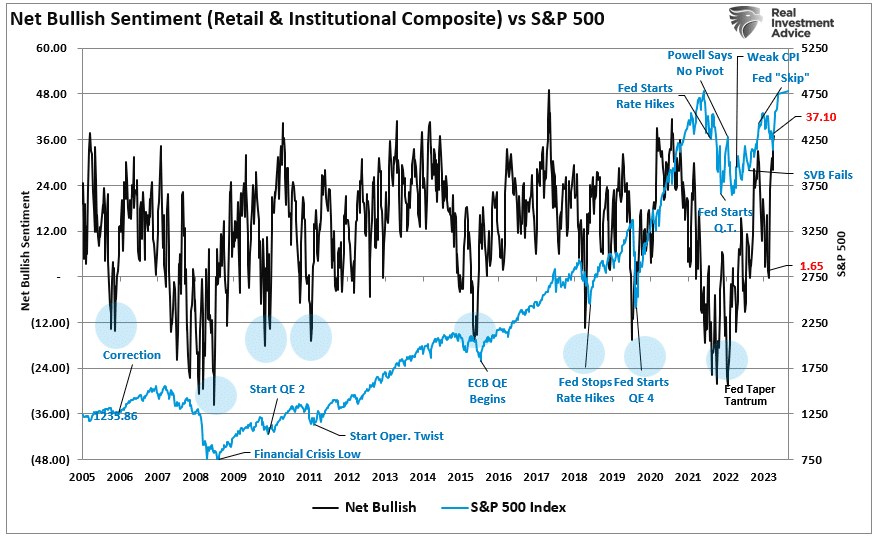

The correction during the summer certainly had the bears coming out of hibernation, but the bulls were entirely in charge by year-end. The chart is the combined net bullish sentiment index (professional and retail) compared to the S&P 500 index.

So, with the understanding that 2023 defied all previous expectations, what do investors enter 2024 think regarding the market and the economy?

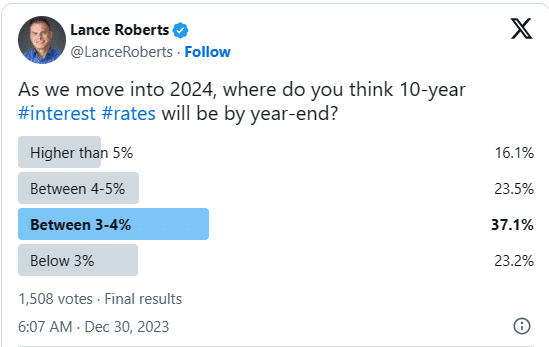

The 2024 Twitter Poll Outlook

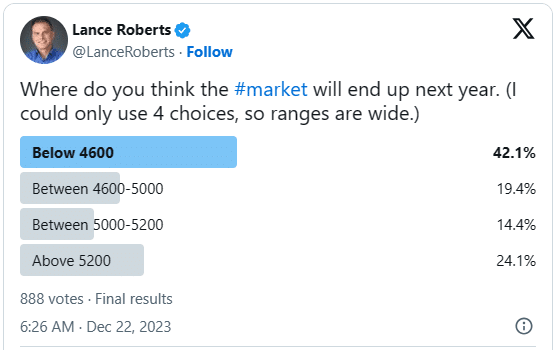

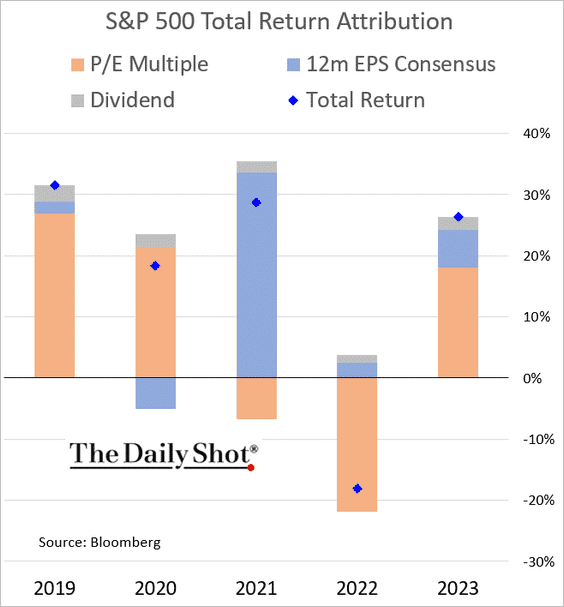

With the S&P 500 ending the year 24% higher than where it started, 42% believe 2024 will end lower than the year’s close of 4769. However, if we split the 4600-5000 band, roughly 50% think the year will be lower. Interestingly, 24% expect returns above the 2024 market consensus of 5200.

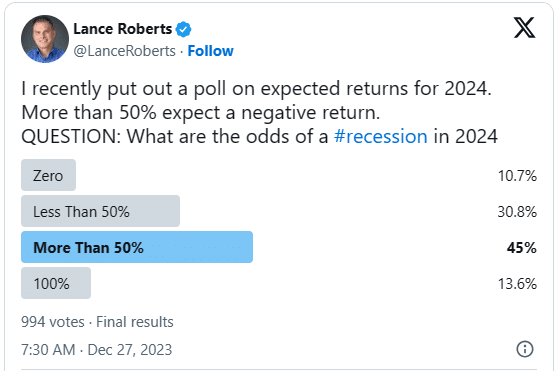

Of course, for the market to generate those returns, the economy must avoid a recession. When asked that question, 45% of those polled believe there is more than a 50% chance of a recession, with 13.6% at a 100% conviction.

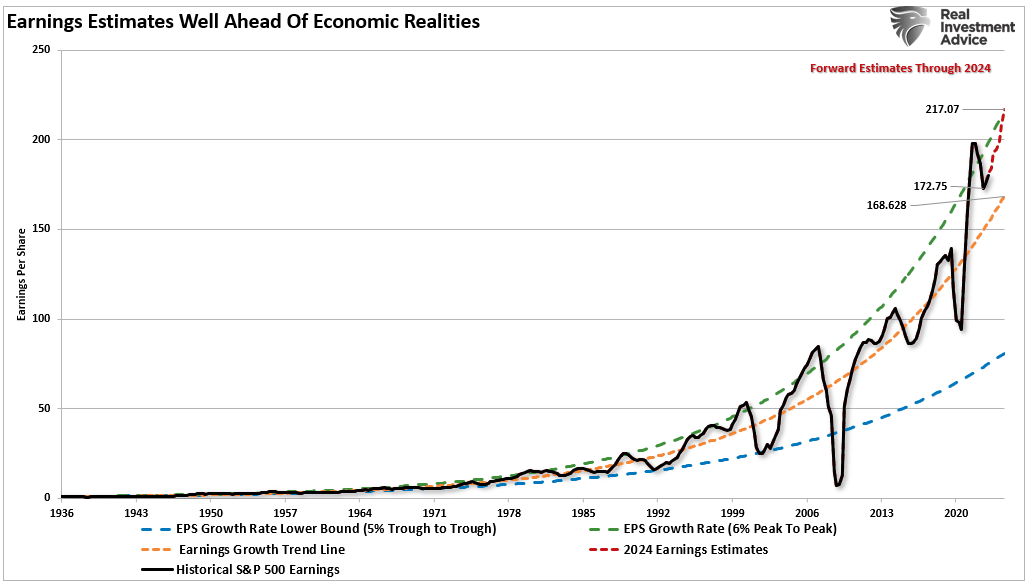

Here is the problem with that view. In an economic downturn, the market must reprice earnings for slower economic growth. Therefore, given that 2023 was a year driven by multiple expansions, there is significant room for a repricing of earnings if a recession develops.

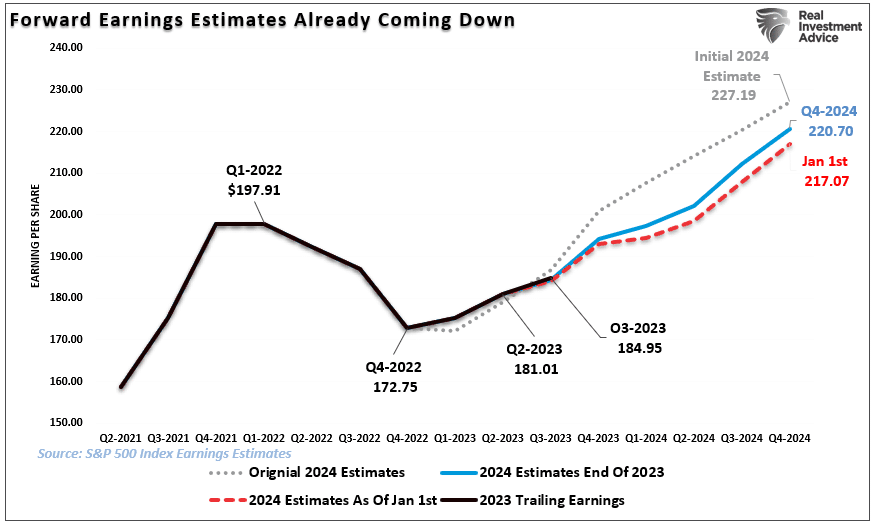

Given that recent economic data has slowed, the more optimistic view of the market will become more challenging as forward earnings estimates continue to decline.

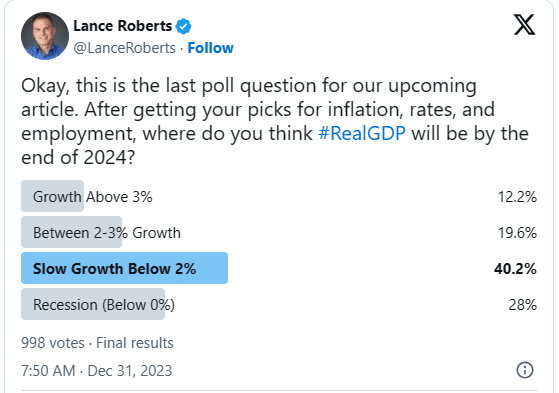

Following that poll question of recession expectations, I asked about real GDP growth (inflation-adjusted). 40.2% of those polled expect the economy to avoid a recession but exhibit growth below 2%. Only 28% expect a recession.

Again, given that earnings are derived from economic activity, the problem of current growth estimates will be more challenging to obtain. Such is mainly the case given that earnings growth estimates for 2024 are highly elevated relative to historical norms.

With valuations on the rise, as earnings fail to keep pace with price increases, the risk of a repricing event increases if earnings fail to meet current expectations. What could keep earnings under pressure? Such would be a slower economy impacted by higher inflation, unemployment, and interest rates.

Higher Rates, Unemployment and Inflation

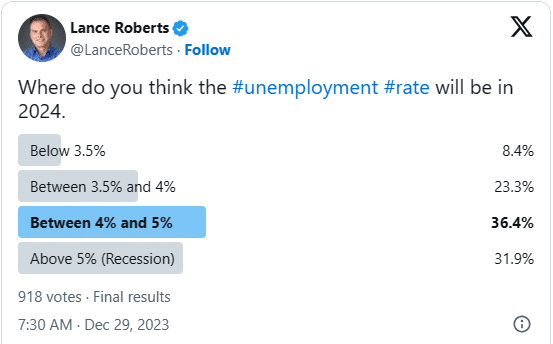

The 2024 poll became more interesting when explicitly asked about the underlying factors of the economy. For example, more than 68% of those polled believed the unemployment rate would rise above 4% this year.

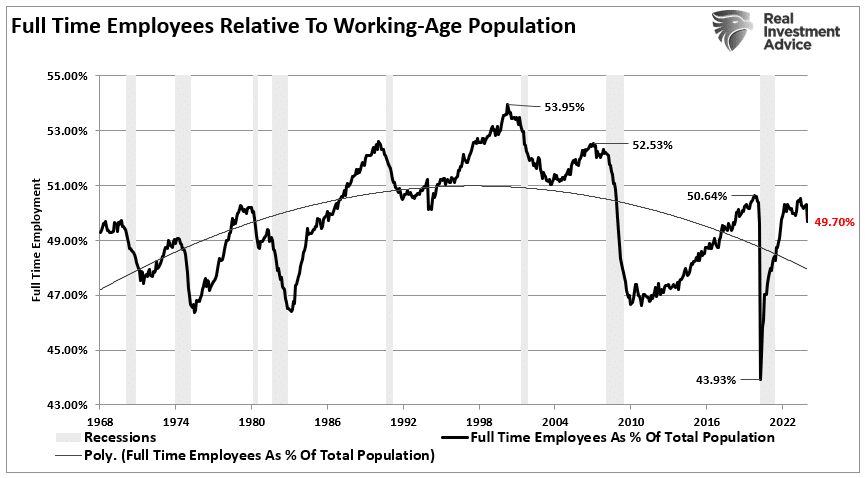

Given last Friday’s BLS employment report’s sharp drop in full-time employment, there is certainly some evidence to suggest economic deterioration is in process. (We will discuss this in further detail on Friday.)

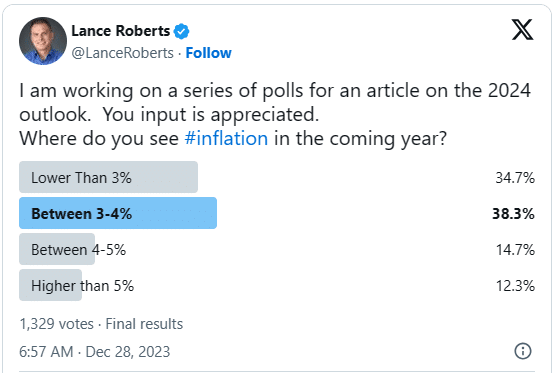

However, if employment is expected to fall, then higher rates of inflation are much less probable. Such is because of the supply/demand relationship that drives employment over time. Therefore, the 65% of respondents who believe inflation will be higher than 3% over the next year will likely be disappointed.

Another dichotomy in the survey was interest rates. Most respondents also think interest rates will be higher over the next year.

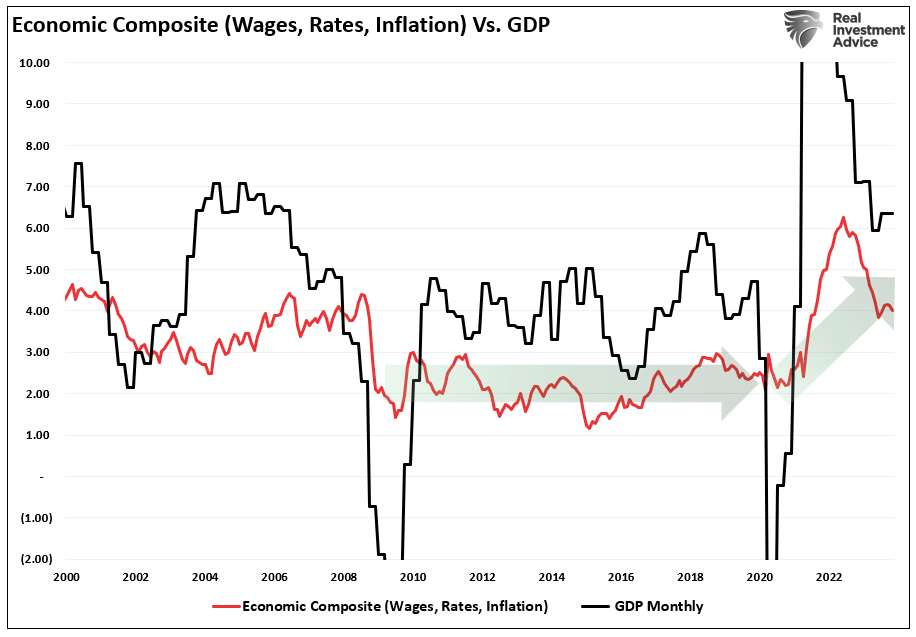

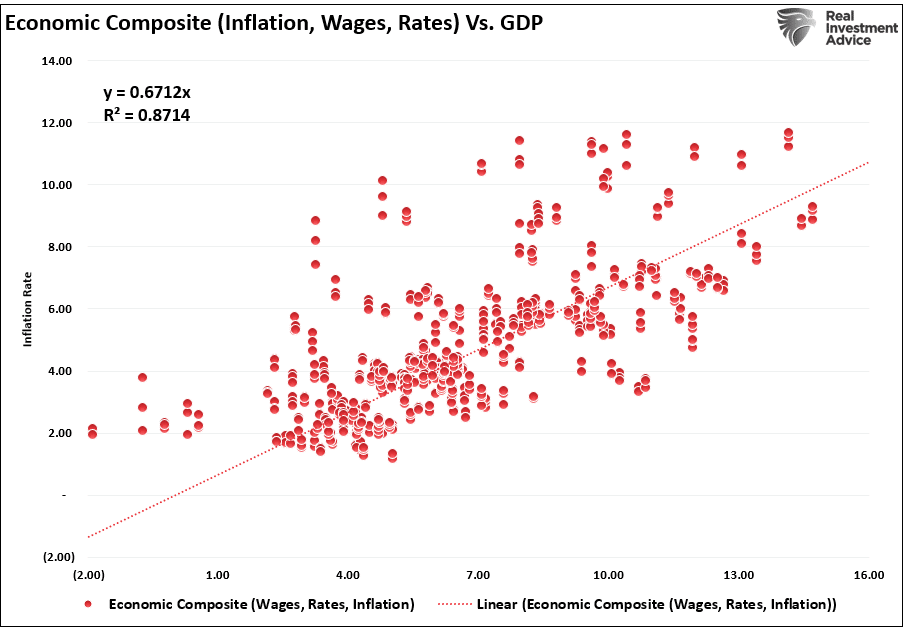

The issue is the high correlation between inflation, interest rates, wages, and economic growth. Such was a point discussed previously.

“Falling inflation, interest rates, and higher wages support the economy. The composite index of wages, inflation, and interest rates remains well elevated above the post-Financial Crisis trend. While it is reversing, which corresponds with weaker economic growth rates, it is not near levels suggestive of an economic recession.”

While it is not near recessionary levels yet, the data trend is slowing. As noted, with an 87% correlation to economic growth, the slower pace will eventually manifest in lower interest rates and inflation.

Conclusion

Given that these polls were taken over a week, the participants in the survey were not the same. Such accounts for the diversity of responses in the poll.

While you should not make any assumptions from these polls, the responses were interesting. Overall, most participants are more bearish on the markets and economy for the coming year. This was the case last year, and the markets defied those expectations. However, a critical takeaway is that the economy can not be weaker AND have higher inflation and interest rates. If employment is slowing, as it looks like, the real risk is slower economic growth, lower rates, and further disinflation.

If such is the case, the current earnings growth expectations this year remain elevated even though they have already been revised lower. Such potentially creates the potential for investor disappointment and a repricing of markets to correspond with reduced valuation assumptions.

While we have no idea how 2024 will eventually turn out, the risk is that the markets may defy more bearish expectations again, hoping the Federal Reserve will offset any risk with accommodative actions.

Or maybe this is the year the “Bears” get it right.

The best we can do is pay attention to the changes in the data, manage risk, and be willing to change our views as needed.