Trending

Might another market liquidity event be on the horizon? While there is generally good liquidity in the financial system, there are some nascent signs that problems could arise. A liquidity shortfall can have meaningful market impacts since asset prices rely heavily on liquidity. Liquidity problems lasting more than a few days typically require the Fed to inject liquidity into the financial system to stabilize it. Investors and traders, aware of the liquidity situation, are often rewarded handsomely for frontrunning the inevitable Fed response. Therefore, let’s review the current liquidity status in the financial system and harken back to 2019 to appreciate the potential timing for a liquidity shortage and, equally importantly, consider how the Fed may react to such a problem.

Clear Signs Of Liquidity Problems

Imagine a friend asking for a favor. His rent is due today, but he isn’t paid until tomorrow. To bridge his 24-hour liquidity gap, he asks for a loan. He offers to give you the keys to his new Mercedes in exchange for $5,000. He promises to pay you back in full, including interest, tomorrow. Moreover, if he doesn’t pay, the car is yours.

Not only can you be a good friend, but if he fails to pay you back, you will have a new Mercedes worth a lot more than $5,000. The proposal is as close to a risk-free, win-win proposition as possible.

The tell-tale sign of a liquidity problem in the banking system occurs when a profitable, risk-free lending situation, like our neighbor’s proposition, arises and no lenders are willing or able to advance money or are only willing to do so at an exorbitant price.

The most recent liquidity event occurred in 2019. As a result, the Fed came to the market’s rescue by restarting QE, advancing funds through its repo program, and lowering the Fed Funds rates. Stock investors frontrunning the Fed were able to take advantage of a 15% S&P 500 surge in just four months.

The 2019 Repo Market Liquidity Crunch

In September 2019, the $4 trillion overnight repo market froze. Overnight repos are one-day loans collateralized with U.S. Treasury and Mortgage-Backed Securities. Like our example, ample collateral exists to prevent any loss if the borrower defaults. Accordingly, overnight repos should trade better than Fed Funds, which have no collateral backing.

Equally important, many leveraged portfolios holding stocks, bonds, and other assets depend on overnight repo for funding. If money can’t be borrowed, leveraged asset holders must sell assets.

The graph below from the Fed shows that overnight repo rates traded 25 basis points higher than the norm on September 16th and then surged on the 17th. Borrowers had to pay 3.00-3.50% more than was typical for a fully collateralized overnight loan.

The combination of quarterly corporate tax payments, Treasury auction settlements, and the Fed’s ongoing QT activities drained excess liquidity from the banking system. Significant liquidity demands may move the overnight markets by a few basis points, but this instance was a different animal.

The Fed provided immediate liquidity via an overnight repo operation. The emergency operation was soon extended through the second quarter of 2020. As shown below in red, the amount borrowed from the Fed via this facility was about two times the peak borrowed during the financial crisis.

To further bolster liquidity, the Fed announced $60 billion per month in Treasury Bill purchases (QE) and reduced the Fed Funds rate twice by the end of the year.

There is a limited amount of liquidity in the system. In 2019, QT, tax payments, and heavy Treasury issuance drained liquidity. Accordingly, investors with leveraged portfolios dependent on overnight repo had to pay dearly to borrow. Some likely sold assets to reduce their funding needs. The Fed came quickly to the rescue to prevent a liquidity-driven market meltdown.

Sources Of Liquidity

Beginning in 2019, to address the liquidity shortfall and then to counter the pandemic for the next three years, the Fed flooded the banking system with reserves, allowing the banks to create ample liquidity for the markets. The Fed’s balance sheet peaked at nearly $10 trillion in May 2022. Since then, excess liquidity has slowly been leaving the banking system. Let’s look at three predominant sources of liquidity to help ascertain when or if the financial system might be near another liquidity deficit. For those looking at frontrunning Fed liquidity operations, these liquidity sources are vital to follow.

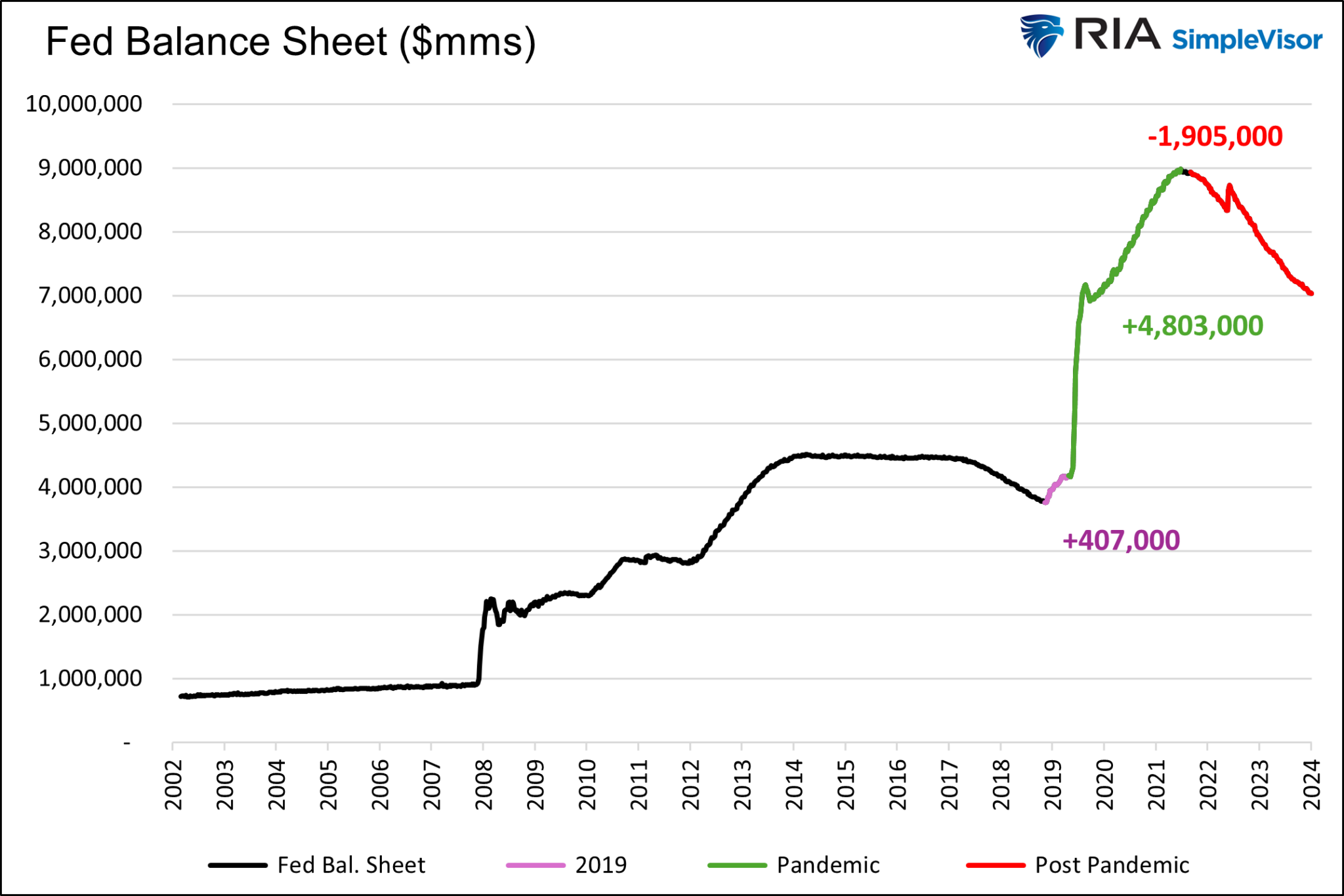

Fed Balance Sheet

The Fed uses its balance sheet to add or remove liquidity from the markets and banking system through Treasury and MBS purchases and sales. QE, in which the Fed buys bonds from the largest banks, removes assets from banks’ balance sheets and replaces them with banking reserves. The reserves are the basis on which banks make loans, i.e., provide liquidity.

Conversely, the Fed removes liquidity with its balance sheet via QT. This occurs when they sell their bonds back to the market or let them mature. In either instance, the banks add bonds to their balance sheets requiring reserves. QT removes reserves available to make loans; thus, liquidity declines.

As we discussed earlier, the Fed’s repo program, residing on its balance sheet, is also used to add liquidity. Conversely, the Fed has a reverse repurchase program (RRP), which we describe further in this article, that reduces liquidity.

The following graph shows the Fed’s balance sheet increased by $407 billion in 2019 to meet the market’s liquidity shortfall and another $4.8 trillion during the pandemic to flood the banking system with liquidity. The graph also shows a decline of $1.905 trillion over the last two years due to QT and declining RRP balances. Since the Fed started addressing the market’s liquidity shortfall in 2019, its balance sheet has grown by $3.3 trillion.

Overnight Reverse Repurchase Agreements

The massive addition of liquidity by the Fed during the pandemic was more than the system needed. The Fed wanted to provide the markets with excessive liquidity to ensure they didn’t crash due to the potential economic hardships and anomalies caused by the pandemic.

The drawback was that the excess liquidity would force Fed Funds and money market rates well below zero percent. The Fed removed liquidity via its overnight reverse repurchase program (RRP) to avoid negative interest rates. Essentially, the Fed would borrow money (liquidity) from the banks backed by Treasury collateral. Simply put, the Fed added and withdrew funds daily to balance liquidity.

As shown below, RRP removed about $2.5 trillion of excess liquidity from the market at its peak usage. Today, the program sits below $200 billion. RRP is a good barometer of excess liquidity. The declining trend represents liquidity, leaving the Fed’s balance sheet and fortifying the market. However, the dwindling excess liquidity means that the remaining pool of potential market liquidity is limited.

The Treasury Department And TGA

When the Treasury Department issues debt, it removes liquidity from the banking system. Like any other borrower from a bank, Treasury debt requires reserves. When banks use reserves to hold Treasury debt, they have fewer reserves for other forms of bank lending. Not all Treasury debt ends up on bank balance sheets, but even if a citizen or private institution buys the Treasury debt, the cash to pay for it comes from a money market account. Ergo, higher Treasury debt balances require more system-wide liquidity.

Currently, there is approximately $27.6 trillion in federal debt oustanding. That figure is about $10 trillion more than at the start of 2020.

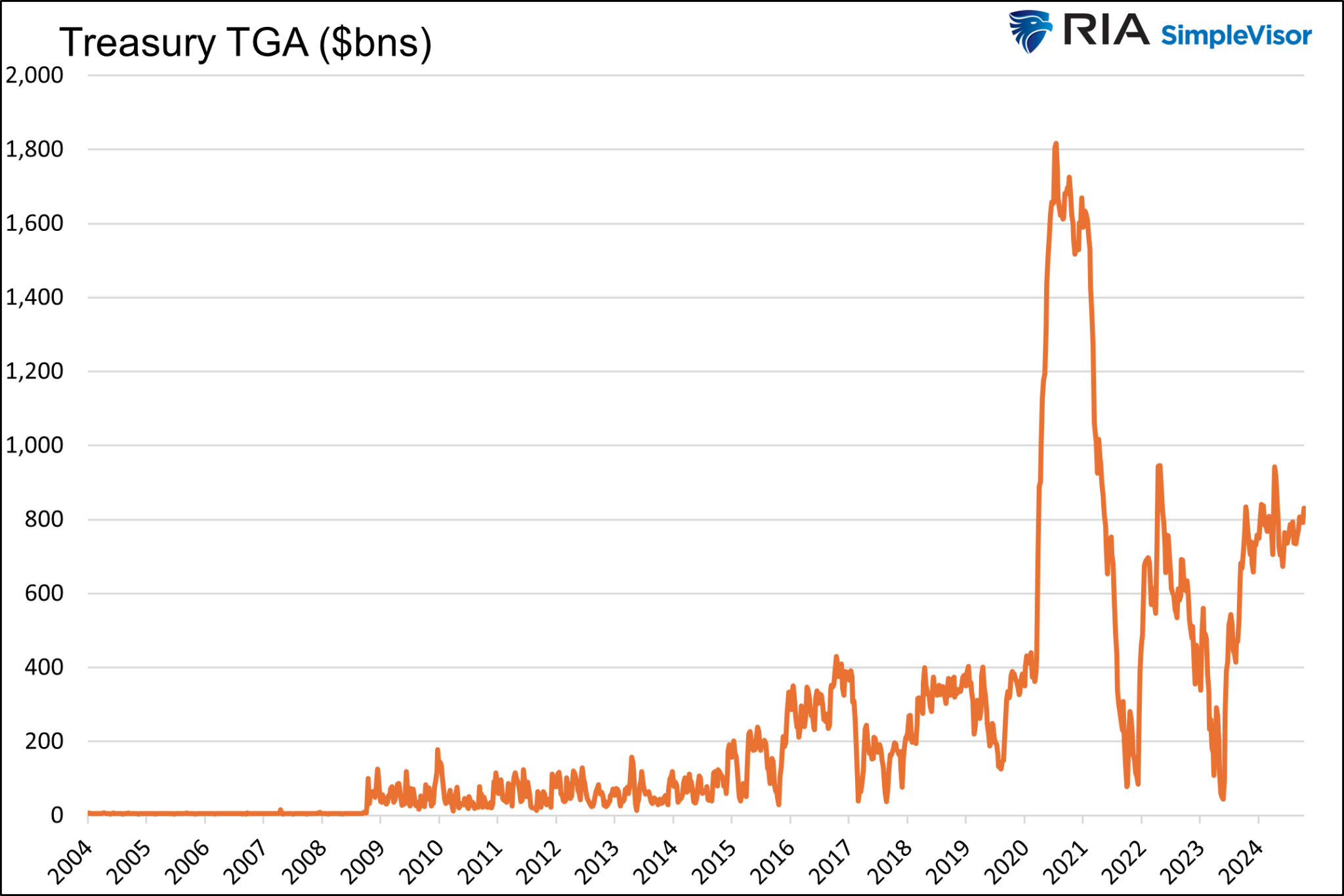

Further complicating the analysis of the Treasury’s role is its Treasury’s General Account (TGA) held at the Fed. This is essentially the Treasury’s checking account. When the account increases, the Treasury is removing liquidity from markets. Conversely, a declining TGA balance represents the addition of liquidity.

As shown below, the TGA account is well above pre-pandemic levels. Spending down the account is a potential source of liquidity for the market.

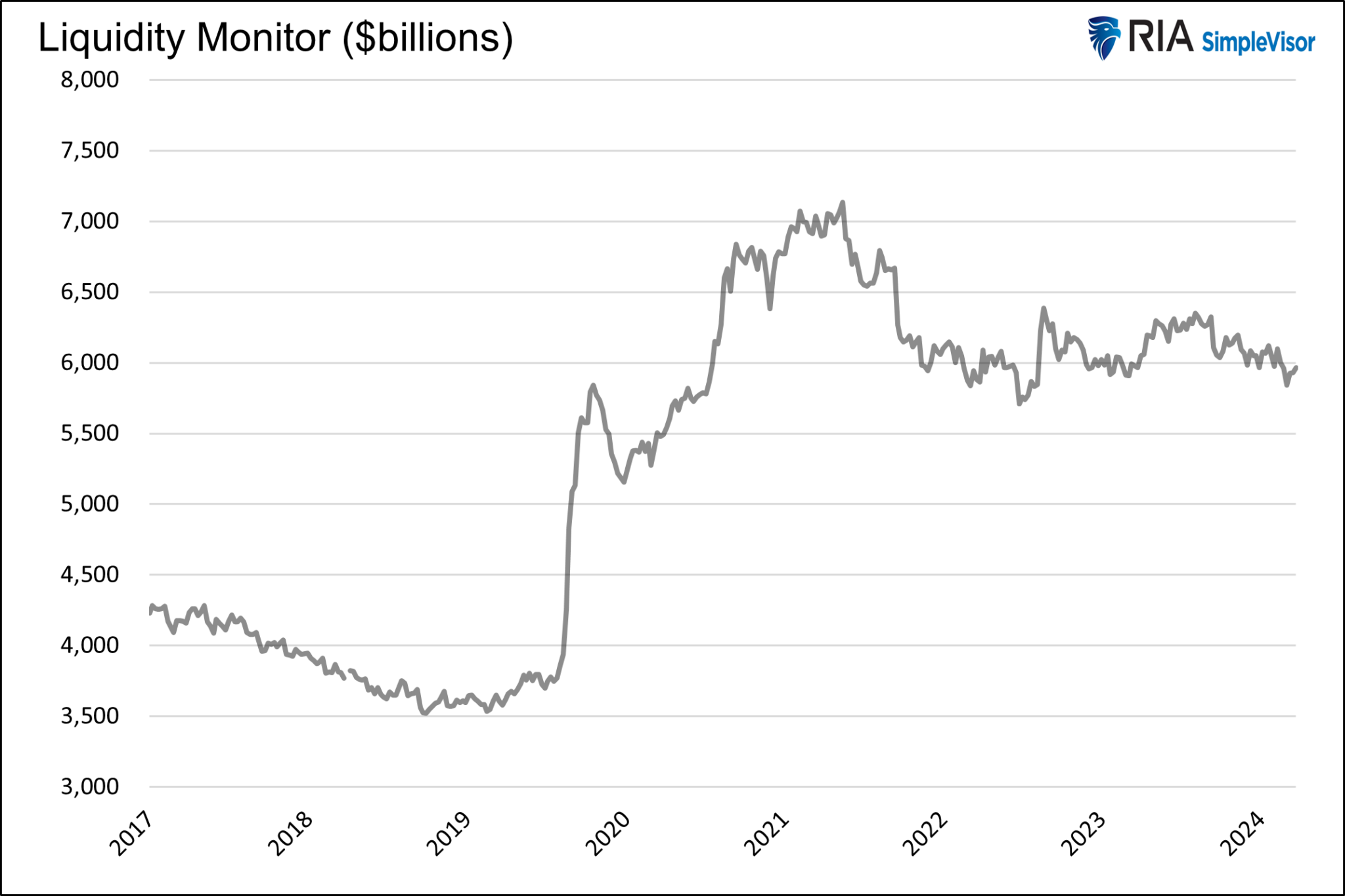

Net Liquidity Monitor

We can use the Fed and Treasury sources of liquidity to calculate a liquidity proxy, as shown below. It’s most important to focus on its trend and not as much on the absolute dollar amount.

We shy away from focusing on the actual number because there is more to liquidity than the three inputs we employ. Furthermore, it doesn’t tell us how much liquidity the market requires or how those needs may change. We know that the size of the asset markets has grown appreciably since 2019; therefore, today’s liquidity needs are significantly greater than five years ago.

Our proxy measure has been relatively stable for the last two years, unlike the steadily declining trend leading to the 2019 problems.

Two Liquidity Clues

The liquidity proxy we share above is not overly concerning. However, we are watching a few other liquidity monitors that are more concerning. For instance, the Fed’s RRP balance is below $200 billion. Its decline, which has offset the liquidity-draining QT operations, has resulted in a stable liquidity proxy. However, there isn’t much gas in that engine.

Also of concern is the recent jump in repo rates, as shown below. While the occurrence was only at the most recent quarter-end, when liquidity is often compromised, the leap in the collateralized SOFR rate was far and away the largest since COVID.

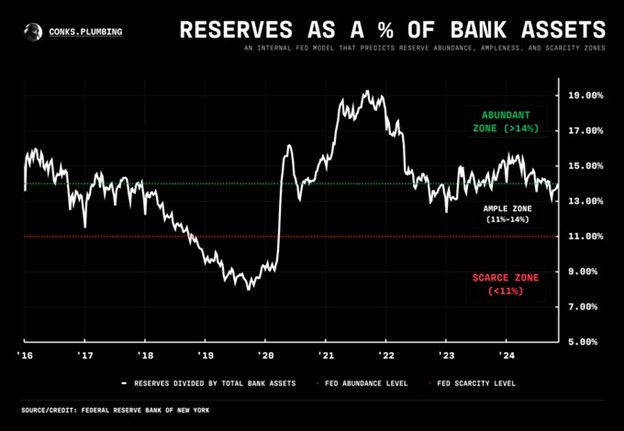

While RRP and the recent spike in overnight borrowing costs are alarming, the graphs below show that bank reserves are ample.

The first graph below shows that banks’ reserves are declining slightly but well within the range of the last few years. A sharper or extended decline, like 2018-2019, would be more concerning. Similarly, the second graph shows reserves as a percentage of banks’ assets.

Summary

There is no imminent concern about a liquidity problem, albeit a few indicators tell us to pay attention. Liquidity problems arise quickly. With the excess liquidity in the RRP program dwindling, our liquidity radars must attune.

Liquidity problems will likely first appear via spiking overnight borrowing rates. If it persists, asset market prices will feel the effect. However, the Fed is very attuned to liquidity conditions and the markets. Accordingly, they will likely supply liquidity when needed and arrest any market disruption quickly.

While a liquidity shortage is alarming, it is at that time we should think about the benefit of the emergency liquidity on asset prices that the Fed is likely to flood the markets with. Frontrunning Fed liquidity operations are not for the faint of heart but can be very rewarding if timed correctly.