Trending

Written by: Thomas Van Spankeren, CFA, CFP® | RISE Investments

It’s tax season, and many of us are looking for ways to reduce our tax burden for the upcoming year. Whether you are looking to reduce capital gains tax, maximize deductions or increase your retirement savings, here are three proven tax strategies to maximize your tax savings in 2025.

1. Tax-Loss Harvesting: An Effective Strategy to Offset Capital Gains Taxes

Tax-loss harvesting is a strategy that involves selling securities at a loss and reinvesting the proceeds into a similar investment, thus keeping you invested in the market. The loss realized on a tax-loss harvest trade serves to offset capital gains realized in other areas of your portfolio. Furthermore, if the portfolio has a net realized loss for the year, up to $3,000 of the net loss can be applied to reduce the investor’s taxable ordinary income. Investors can also carry forward any remaining net realized losses above the $3,000 to offset realized capital gains in future years.

While many consider tax-loss harvesting to just be a year-end exercise, investors can benefit from actively tax-loss harvesting throughout the year, especially during times of heightened market volatility.

For instance, the S&P 500 index declined approximately 4% in the first quarter of 2025. An investor who purchased shares of a S&P 500 ETF at the beginning of the year could harvest the losses and purchase a similar (but not virtually identical) strategy, such as the Russell 1000 ETF.

It is important for investors to understand wash sales rules, as an investor will not receive the tax-loss benefit if he or she sells a security at a loss and purchases the same security within 30 calendar days after the sale.

2. Contributing to a Health Savings Account (HSA) or Flexible Spending Account (FSA)

HSAs and FSAs are tax-advantaged accounts that allow individuals to make pre-tax contributions that can be withdrawn on a tax-free basis, so long as the money withdrawn is used for qualified medical expenditures.

While an individual can only contribute to an HSA if he or she is a participant of a High-Deductible Health Plan, individuals can generally contribute to an FSA regardless of their health insurance plan or if they decline employer-sponsored health insurance.

The contribution limits have increased for 2025 meaning that single and family plan participants are able to defer more income into this tax-advantaged vehicle.

Additionally, those that are 55 and older can contribute an additional $1,000 as a catch-up contribution for an HSA.

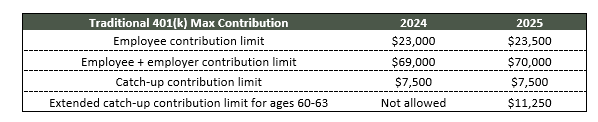

3. Maximize Tax Benefits by Increasing Pre-Tax 401(k) Contributions

A traditional 401(k) plan is a popular retirement savings plan that allows employees to make pre-tax contributions to a retirement program where funds can be invested and grow tax-deferred until withdrawn in retirement. The funds in the 401(k) plan can start being withdrawn at age 59 ½ without penalty. However, both federal and state tax are owed on amounts withdrawn. Once the plan participant reaches age 73 (or 75 if born in 1960 or later), he or she must begin taking required minimum distributions each year.

Increasing the amount contributed to a 401(k) plan results in immediate savings on federal and state taxes. The maximum amount an individual can contribute to a 401(k) plan tends to increase with inflation each year and there are also catch-up provisions for those at or above the age of 50.

Conclusion

Tax strategies are an effective way to generate additional cash flow that can be used for daily expenditures and to boost savings. Tax-loss harvesting, making contributions to an HSA or FSA and maximizing pre-tax contributions to a traditional 401(k) could potentially save you thousands of dollars in taxes each year while also setting you up for greater future success.