Trending

Expense ratios can be confusing. What are they? What do they reveal about a fund? Why should you, as an investor, care about any of this?

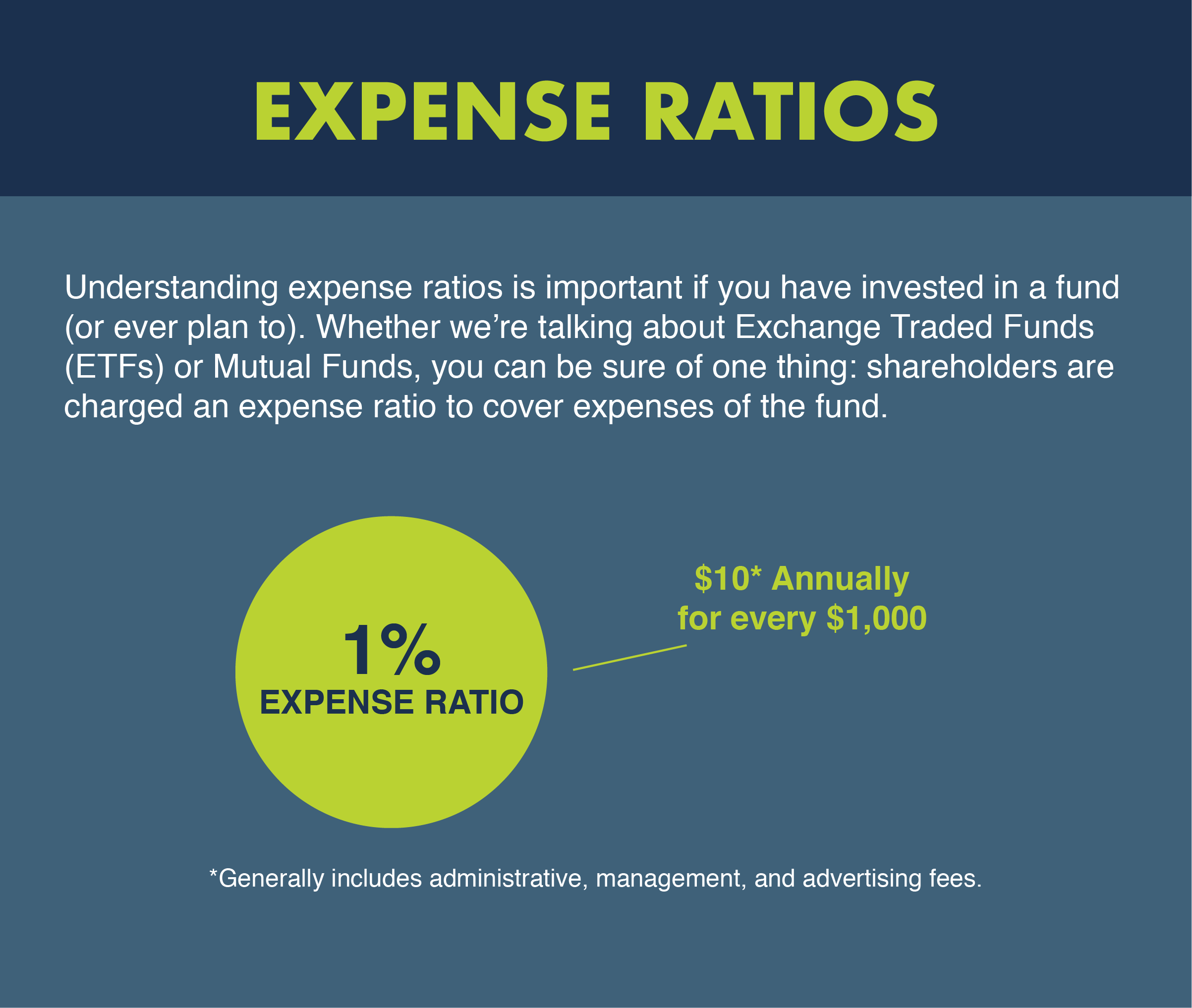

Understanding expense ratios is important if you have invested in a fund (or ever plan to). Whether we’re talking about Exchange Traded Funds (ETFs) or Mutual Funds, you can be sure of one thing: shareholders are charged an expense ratio to cover expenses of the fund.

This charge is not explicitly paid by you, the shareholder, to the fund. Instead, the expense ratio is taken directly from the value of the fund; this reduction in value is reflected in the fund’s daily Net Asset Value (NAV) or, simply put, the fund’s market value per share. Shareholders “pay” the expense ratio indirectly through the value of their investment – as the fund’s returns to shareholders are reduced by operating costs, the value of a shareholder’s investment decreases as well.

The expense ratio is usually expressed as a percent. For example, if the total cost for running a fund is $10 and the fund has total assets under management of $1,000, the expense ratio is 1%. The expenses included in the expense ratio charge vary depending on the fund in question, but generally include administrative, management, and advertising (12b-1*) fees.

One way you can think about the expense ratio (sometimes called the Management Expense Ratio) is as a measure of efficiency. The lower an expense ratio is, the more efficient fund management is with their resources (and your money).

Armed with this knowledge, you may be tempted to pick a fund to invest in because it has the lowest expense ratio you’ve seen and call it a day. However, there are other factors to consider than just the expense.

Here are some things to keep in mind as you apply your expense ratio knowledge to investing:

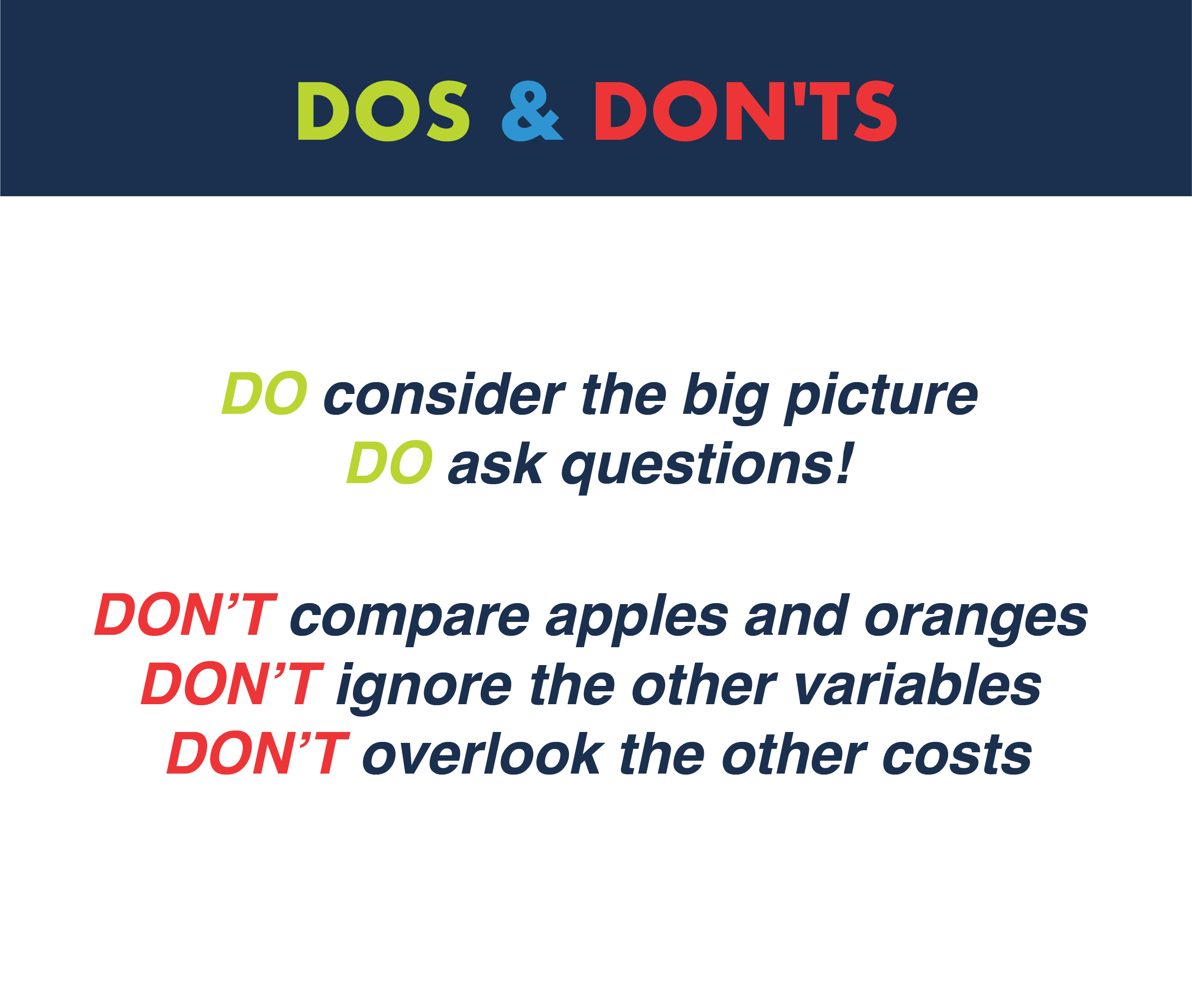

Don’t compare apples and oranges

Just because two things can be compared doesn’t mean the comparison is necessarily valuable. While it’s tempting to compare the expense ratios of two funds, isolated from other factors, to make a quick investment decision – ultimately, it’s not necessarily helpful. This is because funds that appear similar may have different weightings to underlying securities and/or can own different kinds of investments. Because of these underlying cost differences, expense ratio comparisons should be just one factor to consider when evaluating funds that exhibit similar characteristics.

Don’t ignore the other variables

Actively managed mutual funds, for example, tend to have higher expense ratios than ETF’s because they have to pay people to manage the process of selecting securities to buy and sell. Other variables, such as the fund’s classification, investment category, investment strategy, size, and management decisions all impact the expense ratio. This means these fund characteristics impact you, the shareholder, as well.

Don’t overlook the other costs

The expense ratio does not include every fund cost nor any of the costs associated with hiring a wealth manager. The expense ratio is the cost of owning the fund. As such, any brokerage costs, sales loads, transaction fees, advisory fees and any other charges passed on to investors aren’t reflected in the expense ratio.

Do consider the big picture

The expense ratio of a fund is one of many factors that need to be considered before making an investment decision. Rather than getting bogged down in the particulars of a fund, ask your financial advisor how the fund in question aligns with your long-term goals and if the costs are warranted based on the fund’s investment strategy. More importantly, always ask if there are any other funds that have a similar strategy that are cheaper and if they were considered as well before making a recommendation. Not all advisors are required to operate as fiduciaries and therefore do not have to be acting in your best interest.

Do ask questions!

As an investor, you should never feel shy about asking your financial advisor for clarification on something you’re having trouble understanding or for an explanation on any recommendation they are making to buy or sell an investment. At Monument, we encourage our clients to take an active role in understanding how their finances work; after all, wealth management should always be a human conversation, not a numbers game.

This first appeared on Monument Wealth Mangement.

Related: How Can a Plan Balance When Gravity Can’t Be Ignored?

*The SEC adopted rule 12b-1 in October of 1980 under the Investment Company Act of 1940, making it legal for funds to pay for marketing and distribution expenses directly from the assets of the fund. The SEC does not limit the amount of 12b-1 fees a fund can charge, but FINRA rules prohibit 12b-1 fees from being higher than 1% of an investors’ assets in the fund per year (.75% distribution fee cap, .25% shareholder service fee cap).