Trending

The Powell inspired, coinciding (have your pick) S&P 500 stop run is almost history now, with the futures trading over 3,880 again as we speak. No surprise here, but since the long-term Treasuries plunge went on largely unabated, that‘s concerning.Even if not now as in right away, TLT and TLH have to power to trouble the stock bulls seriously.

And the financials benefiting from the greater spread, won‘t save the day, as the key chart to watch now is technology and also healthcare. Healthcare especially because biotech didn‘t get its act together yesterday really, while semiconductors did better. With consumer discretionaries hurt, utilities and consumer staples can‘t be relied on in a rising rates environment, and communications can‘t save the day either. The sectoral outlook remains mixed, even as value continues greatly outperforming growth this month.

The stock bulls simply need tech clearly stabilized and turning here so as to think about new S&P 500 highs again. Long-term Treasuries are starting to hold greater sway over the stock market fate now, too. The dollar‘s woes thus far continue playing out largely in the background.

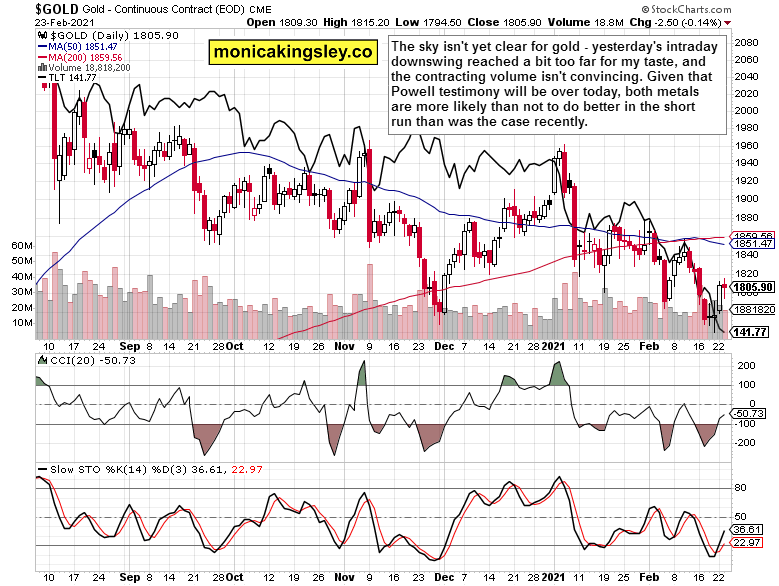

Did gold shake off the TLT shackles? Still early to say, but the clear, directionally opposite move gives the bulls benefit of the doubt thus far. Yesterday‘s gold session didn‘t convince me, so I am not trumpeting the end of yellow metal‘s downside yet. Still, cautious optimism remains – even in the short run, let alone for the medium- to long-term: there, the (bullish) picture is simply clearer.

Let‘s remember my yesterday‘s words about trends and flashes in the pan:

(…) Powell‘s testimony is about to bring volatility, but does it have the power to change underlying trends? Not really – while his latest high profile assessments brought about a downswing, stocks recovered in spite of the GameStop (contagion?) drama too. Should we see a replay of the above, new highs are coming – and they are, in both stocks and precious metals. We‘re in a commodities supercycle on top!

Let‘s get right into the charts (all courtesy of www.stockcharts.com).

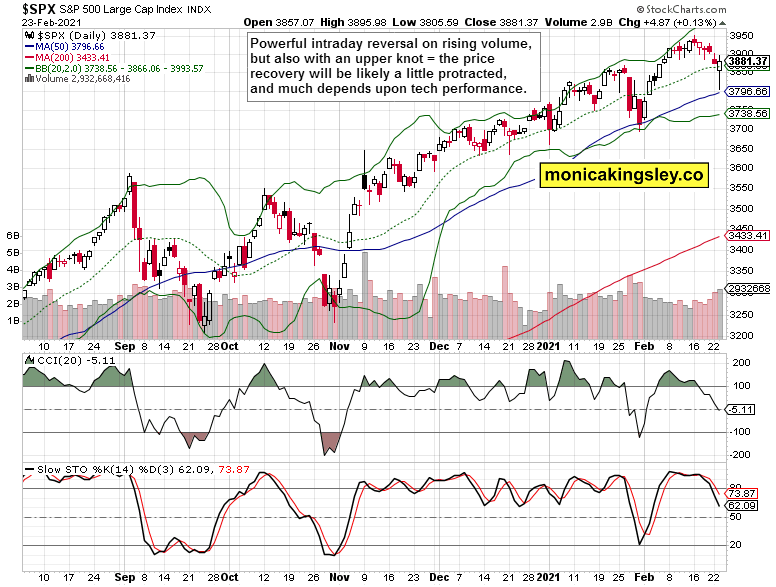

S&P 500 Outlook

Yesterday‘s intraday reversal reached just a little above Monday‘s closing prices, highlighting that more needs to be done for the index to regain upside momentum. The Powell testimony reversal was a good start, and stock bulls need to do more once this event gets in the rear view mirror later today. Given the premarket action reaching 3,890, the case is not lost.

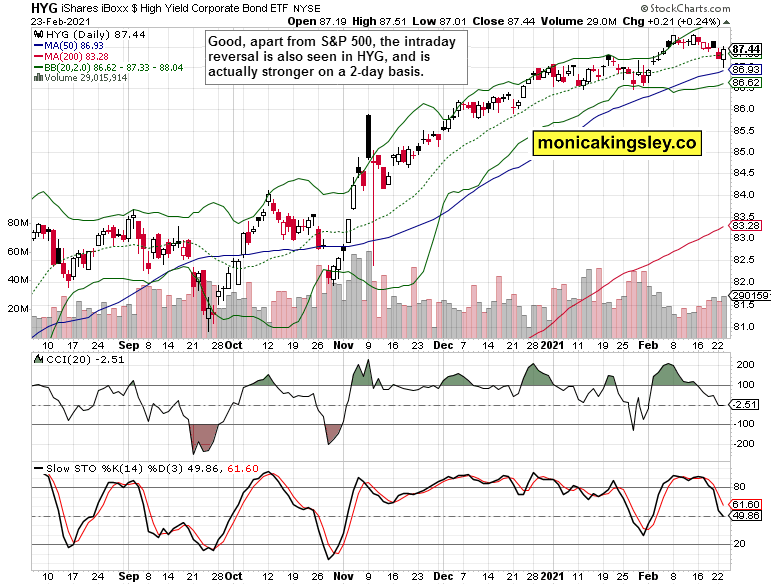

Credit Markets

High yield corporate bonds (HYG ETF) recovered, and crucially did better than stocks. The volume comparison is also a tad more positive. Should this credit market outperformance in the short run hold, then the S&P 500 is more likley to advance than not, too.

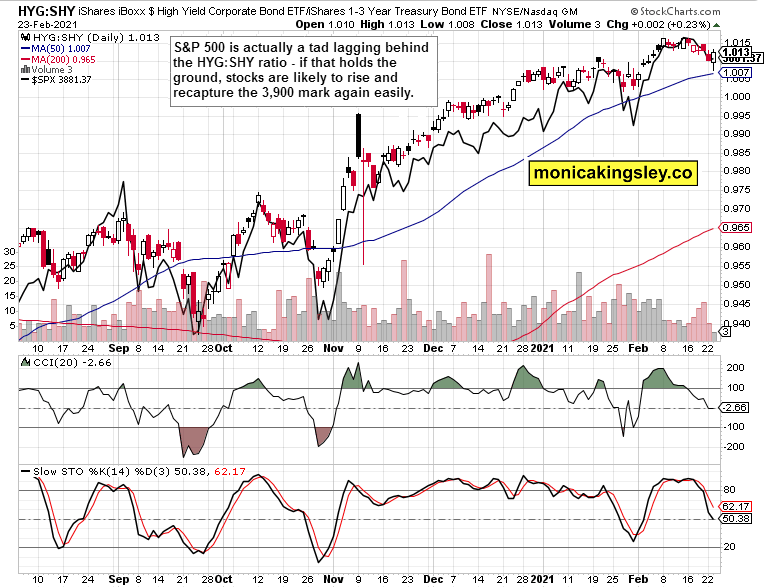

High yield corporate bonds to short-term Treasuries (HYG:SHY) ratio is still behaving reasonably – the overlaid S&P 500 prices (black line) aren‘t accelerating to the downside. The cue to move higher in stocks is apparent.

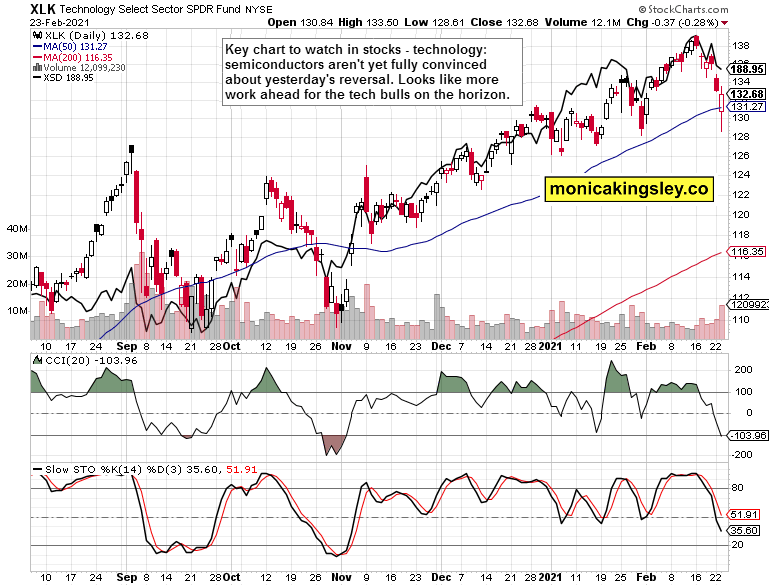

Technology

It‘s the tech (XLK ETF) again – its yesterday‘s reversal is not nearly enough for the S&P 500 to think about taking on new highs. Semiconductors (XSD ETF) subtly outperformed, but they don‘t give outrageously bullish signs either. The tech jury is still out, and this heavyweight sector remains vulnerable, with consequences to the S&P 500 if it doesn‘t keep on the muddle through recovery path at the very least.

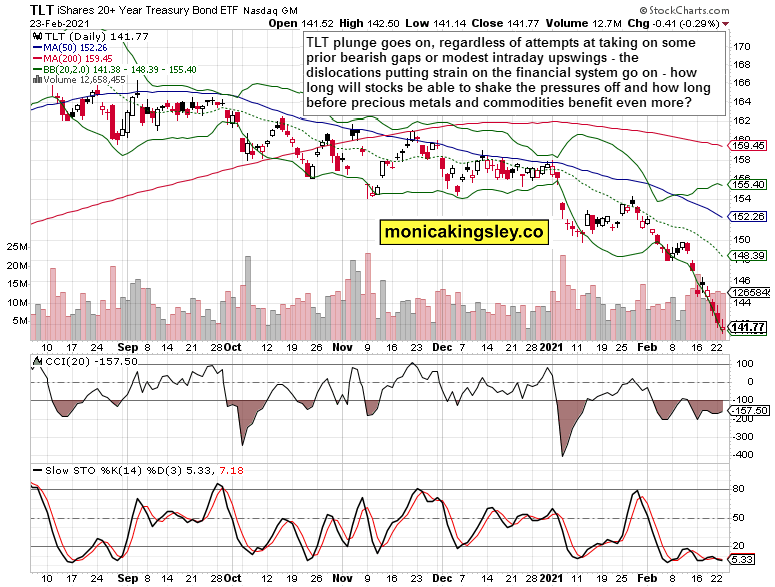

Treasuries and Dollar

No spike in TLT volume shows there isn‘t real willingness to buy the dip the way it were in mid Feb – back then, I could call for a moderation in the decline‘s pace for at least a day, now I can‘t do that. This chart presents the greatest challenge for the markets – going well beyond stocks, precious metals and commodities.

Dollar bulls are predictably on the run. Truly bearish chart targeting much lower lows, in line with the theme I‘ve been banging throughout 2020‘s latter half – the dollar has gotten on the defensive, and would remain there throughout 2021. The technical rebound is over, and not even higher yields can help the greenback much.

Gold, Silver and Platinum

True, gold‘s yesterday‘s candle leaves much to be desired for the bulls, but once again, we‘re seeing a clear refusal to move down even as Treasury yields continue to plunge. It‘s still a valuable first swallow, and more has to follow. Gold isn‘t getting anywhere in today‘s premarket while silver, copper, oil and soybeans are all up mildly. Agrifoods reached a new 2021 high yesterday – commodities clearly like and anticipate the inflationary Fed speak message they get.

One look at the precious metals group – gold the laggard, silver leading, and platinum even more so – check out on the caption when the latter decoupled – 2 weeks before silver did. The anatomy of the unfolding precious metals upleg goes on in this predictable fashion, where platinum has the power to keep running more along the lines of commodities such as copper. That means powerfully.

Yesterday‘s watchout though are the miners, which dragged down both the $HUI:$GOLD and GDX:GLD ratios – not below their lows, but still. A great illustration of the yellow metal‘s woes, and low credibility of its yesterday‘s candle with a sizable lower knot.

Summary

Stock bulls are far out of the woods yet, and technology stabilization must kick in first. Little proof thus far it‘s there, and I view the rising rates as starting to bite the stock market too.

Gold and silver also got under the Powell pressure yesterday, and haven‘t escaped the confines of Treasury yields pressure thus far. The markets are clearly wary of the testimony‘s part II still.

Thank you for having read today‘s free analysis, which is available in full here at my homesite. There, you can subscribe to the free Monica‘s Insider Club, which features real-time trade calls and intraday updates for both Stock Trading Signals and Gold Trading Signals.

Related: It‘s Only Tech That‘s Sold: Not S&P 500, Gold Or Silver

The views and opinions expressed in this article are those of the contributor, and do not represent the views of IRIS Media Works and Advisorpedia. Readers should not consider statements made by the contributor as formal recommendations and should consult their financial advisor before making any investment decisions. To read our full disclosure, please click here.