Trending

Written by: Vipul Jain and Roman Kouzmenko | MSCI

- The short interest factor's return spiked during the mid-March sell-off in global equities, similar to what happened during the 2008 global financial crisis.

- During the recent sell-off, we observed a reduction in aggregate shorts, suggesting that the outperformance might have been driven by the unwinding of short positions, particularly among the most heavily shorted stocks.

- The strongest performance of the short interest factor occurred in countries that enacted short interest bans, suggesting that these bans may have driven the unwinding of existing short positions.

Historically, heavily shorted stocks have underperformed the market as a whole. The short interest factor — a proxy for a strategy that invested in the most highly shorted stocks — spiked during the peak of the March sell-off. The factor also outperformed during the peak of the 2008 global financial crisis (GFC).

Given these facts, we address the following questions:

- What was the relationship between the short interest factor and large market drawdowns?

- Were there significant changes in short-selling activity during the COVID-19 crisis?

- Did short-selling bans influence short interest factor performance?

What Was the Relationship Between the Short Interest Factor and Large Market Drawdowns?

When investors think stocks are overvalued, some may seek to short them — typically, by borrowing stocks. But when markets are not conducive to short selling, such as during large drawdowns, investors may choose to return these borrowed stocks by covering or unwinding their short positions. To do so, they may buy the stocks they had previously shorted. The combination of already high valuations (usually reflecting above-market returns) and newly increased demand for these stocks, usually means that these stocks outperform the market.

The short interest factor’s return represents the performance differential between stocks having high and low short interest exposure, after accounting for market, industry, country and other style factor influences. In other words, when short sellers have sought to cover their positions, the short interest factor has tended to outperform the market, which is what happened in mid-March.

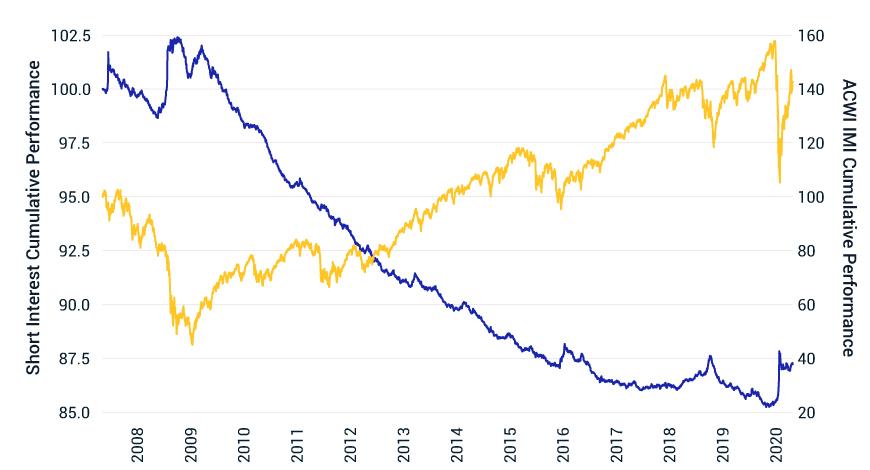

To evaluate the extent of the factor’s recent outperformance, we examined daily short interest factor returns in the MSCI ACWI Investable Market Index (IMI) universe from January 2007 through May 2020. The exhibit below shows that the factor significantly outperformed when global markets, represented by the MSCI ACWI IMI, experienced big drawdowns, such as during the COVID-19 crisis and the GFC.

Short Interest Spiked When Markets Plunged

The short interest factor’s return is computed by running a multivariate cross-sectional regression of the excess returns of the stocks against their exposures consisting of the market, the style, country, industry and currency factors. Performance is computed in the MSCI ACWI IMI universe. Cumulative performance is geometric compounded performance of daily returns.

Were There Significant Changes in Short-Selling Activity During the COVID-19 Crisis?

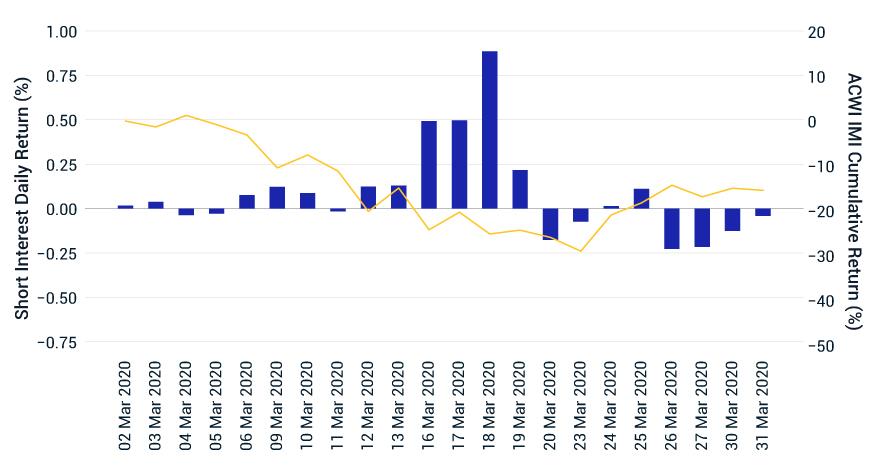

Looking deeper, the next exhibit shows that the factor experienced most of its recent outperformance between March 12 and 19, when global markets experienced significant volatility.

Short Interest Factor Outperformance Occurred in Mid-March

The short interest factor’s return is computed by running a multivariate cross-sectional regression of the excess returns of the stocks against their exposures consisting of the market, the styles, the countries, the industries and the currency factors. Performance is computed in MSCI ACWI Investable Markets Index (IMI) universe.

We also analyzed average short interest levels, normalized by shares outstanding, over all securities in the top decile of the most heavily shorted stocks. As the exhibit below shows, average shares shorted divided by shares outstanding decreased around the period when the short interest factor had the highest returns. This suggests that the outperformance might have been driven, in part, by the unwinding of short positions, particularly among the most heavily shorted stocks.

Most Heavily Shorted Stocks Saw a Reduction in Short Interest During Mid-March

Most-shorted securities are the securities in decile 10 by shares shorted divided by shares outstanding. Average is the simple cross-sectional mean of shares shorted divided by shares outstanding. Deciles are constructed by sorting universe into increasing order of shares shorted by shares outstanding and then dividing it into 10 sub-universes. Each sub-universe has an equal number of stocks and decile 10 is the sub-universe with the greatest exposure to shares shorted by shared outstanding.

Did Short-selling Bans Influence Short Interest Factor Performance?

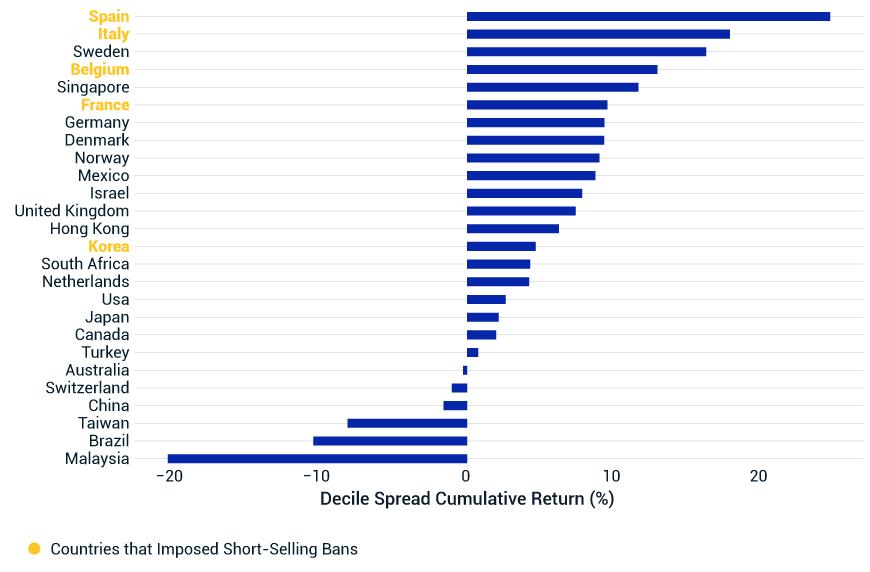

Next, we analyzed the performance of the short interest factor based on a simple decile analysis in a subset of countries in the MSCI ACWI Investable Markets Index (IMI) universe. The exhibit below shows that four of the top six countries with the largest decile spread return were countries where a ban on short selling was enacted during the recent crisis period. For example, in Italy and Spain, a ban was imposed on March 13, in South Korea on March 16 and in France and Belgium on March 17. This evidence suggests that — in addition to preventing further shorting — the short-selling bans may have also driven unwinding of existing short positions.

Short Interest Factor Outperformance in Countries with and Without Short-selling Bans

Decile spread is the spread of returns between the most-shorted and least-shorted decile. The deciles are constructed by sorting the MSCI ACWI IMI universe based on shares shorted divided by shares outstanding. The decile spread total return is the cumulative return of decile spread between March 11 and March 19.

The extremely volatile period used in this analysis had large negative-return days but also occasional large positive-return ones. It is possible that the performance of the short interest factor was driven, in part, by portfolio deleveraging, a liquidity crunch or short squeezes. We also find evidence that bans on short selling may have contributed to the performance differentiation between heavily shorted and moderately shorted stocks during this period.

1 During the GFC, the short interest factor had positive spikes between Sept. 2 and 18, 2008, when global markets experienced a drawdown of about 12%. During the nadir of the COVID-19 market reaction, the factor experienced positive spikes between March 12 and 19, when global markets dropped about 14%.

2 We picked indexes with at least 35 stocks to ensure a coverage of at least four stocks in each decile.

Related: The Major Stock Index Does Not Reflect the Economy… or Even the Stock Market