Trending

Should the forgotten sectors of the S&P 500 be ignored, or does opportunity knock?

Is it a stock market, or a market of stocks? So goes the old Wall Street expression. In our sound-bite lives, even an observant investor could be excused for not realizing how uneven the returns have been among the 11 sectors of the S&P 500.

That, in turn, impacts everything. After all, so much investor money, including tons of retirement funds and 401(k) assets are loaded up on exposure to S&P 500 Index funds. For many, it is the closest thing we have to a “one-decision” investment these days.

That’s the phrase used in the past to describe investor attitudes. They felt that all they had to do was buy, and there would never be a need to make a sell decision. After all, they were “long-term investors.” And stocks only go up, according to Dave Portnoy and those guys trying to get you to buy their “can’t-miss” stock.

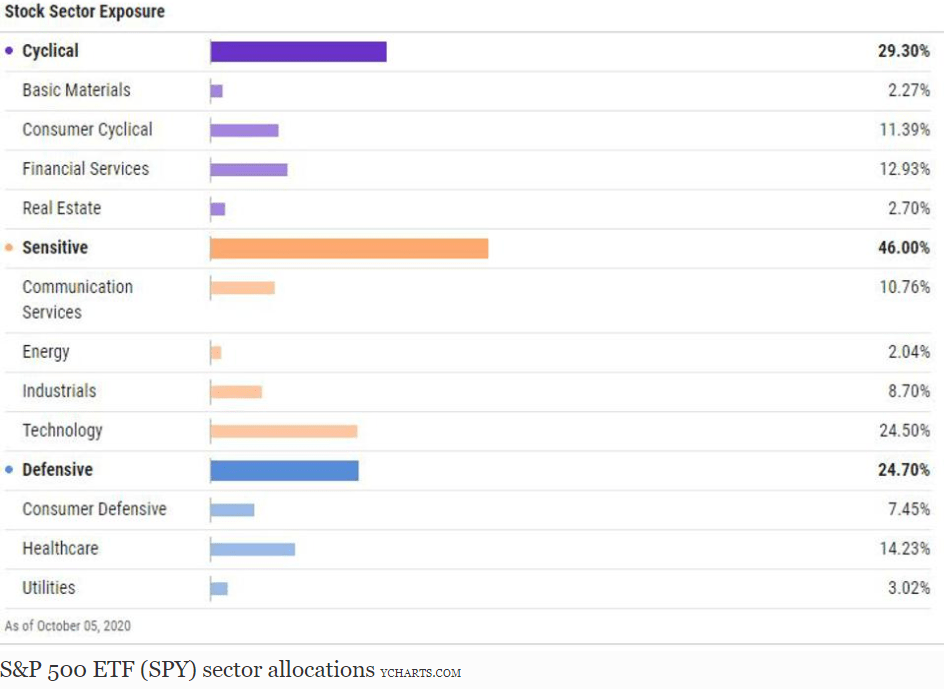

When we look at the S&P 500 today, we find that while there are 11 economic sectors, only some of them matter. Why do I say that? Because collectively, these 4 sectors make up just about 10% of the S&P 500.

That’s right. 90% of the index is comprised of tech and 6 others. So, if you have $1,000 in an S&P 500 index fund, a mere $100 of it is split across the following:

Basic Materials, Real Estate, Energy NRG -0.2%, Utilities

What you do about this depends on what your investment mission is. It also has a lot to do with your outlook for the economy.

I don’t mean next quarter or even next year per se. But if past is prologue, the 4 little sectors will make up some ground on the bigger sectors over time. Energy was one of the larger sectors about 10 years ago, and look at it now. And, as we see tech stocks (currently around 1/4 of the entire S&P 500 Index) dominating like they did during the D0t-Com Bubble 20 years ago, you do get a sense that something has to give.

So What’s The Value in a Sector?

As for what that might be, it is like asking someone if they like a stock. That “value” is in the eye of the beholder. Any security or sector has upside potential at any point in time. The question is how much risk accompanies that upside potential.

Scanning the S&P Sectors

There are many fundamental, quantitative and technical indicators out there. But since we are limited for space, I will present one that I have devoted significant time to. The concept, as I have written in the column in the past, is to evaluate a stock or ETF based on its dividend history.

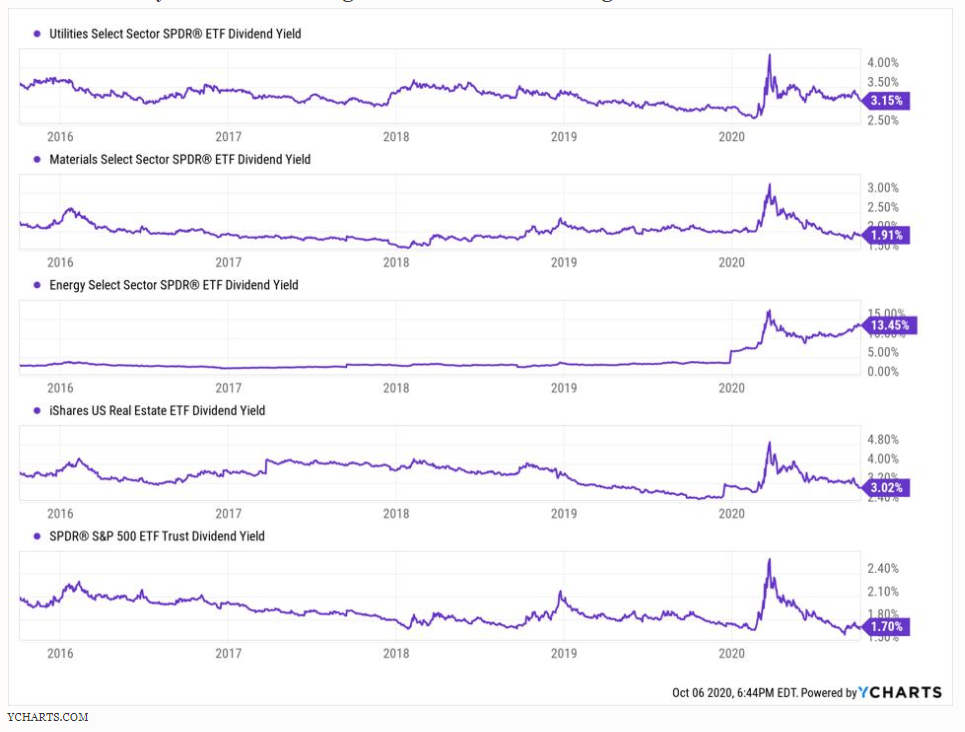

Below is a very simplified version of what I call YARP (Yield at a Reasonable Price). All we are scanning for here is a situation in which one of these underprivileged sectors of the S&P 500 has a dividend yield toward the high end of its historical range.

I went back to the start of 2016. Here’s what I see. Except for the Energy sector, the current dividend yield is closer to its recent low than its recent high. In addition, the S&P 500 (last on the chart), is yielding less than it has at nearly any point during this period.

Where’s the value?

Translation: on the basis of this quick version of a more complex indicator (YARP), nothing appears to be historically “cheap.” In fact, they all look downright expensive. That’s no surprise with a market near all-time highs, though I guess I would have expected to see these smaller sectors closer to their “median” yields.

This is a snapshot in time, and it only looks at one time period. In other words, this says more about the intermediate-to-long-term than what may be attractive in the coming weeks to months. At some point the bull market rally from March will flame out. However, that doesn’t mean it has to be any time soon.

The elephant in the room

Finally, let’s address the elephant in the room: Energy sector. They used to refer to this as “black gold” (including if you were a fan of the old Beverly Hillbillies TV show!). Right now, it’s just a messy sector trying to figure out its future. The sustainability movement, weak demand during the pandemic, and other factors leave us wondering if and when the Energy sector will ever be the same.

Still, that dividend yield is as high as it has been in a very long time. On a “trailing 12 months basis,” the dividend yield of Energy sector of the S&P 500 is over 13%.

There is only one problem. It may not be a believable number. Those companies may not be able to maintain their dividends.

So, the bottom line on Energy is that…there may not be a bottom line for Energy for a while.

This analysis, including the S&P 500 in total, seems to scream “overvalued” at us. Overvalued can stay that way for longer than most of us think. And it appears that there are no great saviors for value-oriented investors coming from the smaller sectors of the market. This should only strengthen your conviction to look at the market with a prudent, yet skeptical eye as we search for that elusive commodity, investment value.

Click here for more on this subject