Trending

One of the major benefits of the intense interest and investment which has gone into creating Robo-Advice models is that institutions are investing a heck of a lot into researching why and how customers are buying financial products.For years the financial services industry has worked with theories such as “insurance is sold, it is not bought”, or “investment products are too complex for consumers to research for themselves” and certainly for an extended period of time these beliefs were largely true. The “supply” side of the industry (product manufacturers as well as distribution) enjoyed the benefits of information asymmetry.

Put simply: We had more, or better, information than the customers did, and were in the position of greatest power or influence.

Well, hasn’t THAT changed! Raw information and research is abundantly available to any consumer with internet access and a smartphone, and that happens to be just about every person whom advisers might want as future clients. What a lot of the market research by institutions looking to deal directly with those consumers is revealing is the extent to which consumers are embracing and actively using their access to this information. Financial products are nowhere near as baffling and confusing to many consumers as we like to believe. They are figuring stuff out for themselves when it comes to deciding on product solutions.

Financial products are nowhere near as baffling and confusing to many consumers as we like to believe. They are figuring stuff out for themselves when it comes to deciding on product solutions.As with most things in life this is either a threat or an opportunity for an advice business, and the choice of those two really is totally ours.

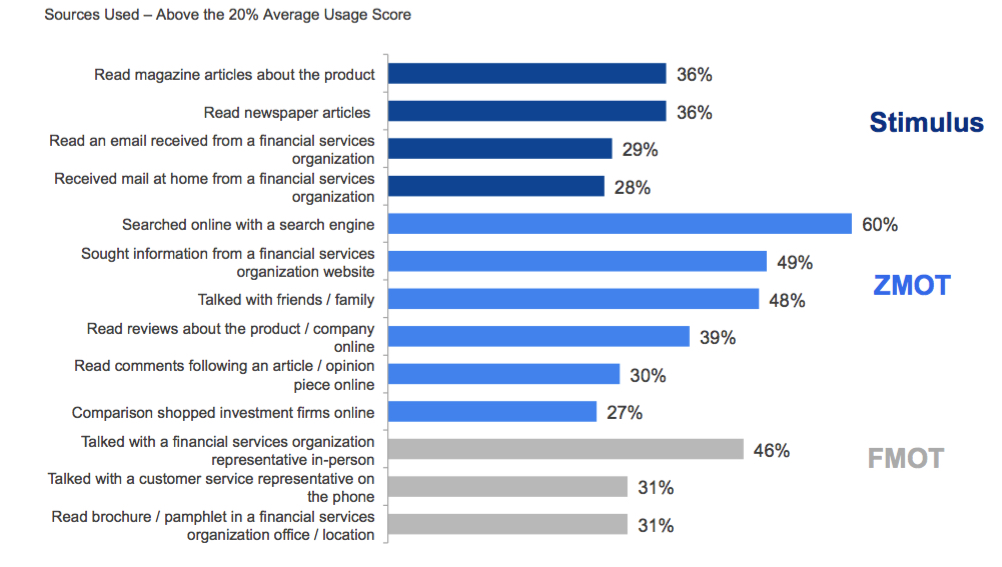

If on the one hand an advice business builds its value proposition or market positioning around the information asymmetry position (“you need us because we have the research/information/smarts…”), then this shift is definitely a threat. In fact it is more than a threat….you have accepted your own demise. This value proposition for an advice business will ultimately result in commercial suicide. You are competing with Google and every other search engine. You will lose that war.On the other hand, we can look at this shift and realise that there is in fact an opportunity to highlight our expertise and position as coaches, or mentors, or counsellors to these consumers. The consumers research may well be triggered by a particular need or transaction at a moment in time (as they see it), and if we are providing useful information which they are using as part of that research then we are definitely still in business. Being a source of trusted and useful information helps with advisers positioning as “guides on the great journey to financial freedom”, and will open up opportunities for us to work with potential clients I believe.What the market research is revealing (and which is particularly useful for advisers) is that there are broadly three phases to the “do it yourself” approach that consumers are using; The first phase of “researching & reading” is a prime opportunity for us to become a trusted information source. Advisers can provide information as well as any other entity, and ensure that it is in with an excellent chance of being found with SEO.The second phase where consumers are essentially “refining” their initial views from the research is also a prime opportunity for advisers. The networking and spheres of influence we create in the real world (not the online world) which essentially are maintained due to our ability to be trusted, respected and deliver value is the opportunity space for us to be able to educate and demonstrate how transactions work with advice. They are not mutually exclusive, are they? So when the consumers turn to friends and family or peers to help refine their choices, that is where great advisers have a great opportunity.The third aspect to the consumers Do-It-Yourself-Decision seems to be me to be primarily about “validating”. Consumers are seeking confirmation that the research and refining stages have resulted in a product solution which is not only likely to be effective, but is also likely to represent good value. “Want good value? Then get some good advice with that product…”Perhaps I am being unduly optimistic as I think about it, however the evolving patterns of consumer’s purchasing process suggest to me that there is opportunity for advisers to position as a far more valuable resource than being mere product delivery mechanisms. Finding and delivering product is something we can do (and do well), and it is often a necessary part of putting effective advice strategies in place. Advisers should not be shying away from that aspect. However, it is not the aspect which presents real value to the consumer.For advisers who figure out how their ideal clients are researching, refining and validating financial decisions, there is opportunity. There is opportunity to be part of the assessment and education phases, and establish higher value in the consumers mind than the product element itself can. There is opportunity to sell the value of advice.Isn’t that what we wanted? The opportunity to showcase the value that advisers can bring to the clients lives?

The first phase of “researching & reading” is a prime opportunity for us to become a trusted information source. Advisers can provide information as well as any other entity, and ensure that it is in with an excellent chance of being found with SEO.The second phase where consumers are essentially “refining” their initial views from the research is also a prime opportunity for advisers. The networking and spheres of influence we create in the real world (not the online world) which essentially are maintained due to our ability to be trusted, respected and deliver value is the opportunity space for us to be able to educate and demonstrate how transactions work with advice. They are not mutually exclusive, are they? So when the consumers turn to friends and family or peers to help refine their choices, that is where great advisers have a great opportunity.The third aspect to the consumers Do-It-Yourself-Decision seems to be me to be primarily about “validating”. Consumers are seeking confirmation that the research and refining stages have resulted in a product solution which is not only likely to be effective, but is also likely to represent good value. “Want good value? Then get some good advice with that product…”Perhaps I am being unduly optimistic as I think about it, however the evolving patterns of consumer’s purchasing process suggest to me that there is opportunity for advisers to position as a far more valuable resource than being mere product delivery mechanisms. Finding and delivering product is something we can do (and do well), and it is often a necessary part of putting effective advice strategies in place. Advisers should not be shying away from that aspect. However, it is not the aspect which presents real value to the consumer.For advisers who figure out how their ideal clients are researching, refining and validating financial decisions, there is opportunity. There is opportunity to be part of the assessment and education phases, and establish higher value in the consumers mind than the product element itself can. There is opportunity to sell the value of advice.Isn’t that what we wanted? The opportunity to showcase the value that advisers can bring to the clients lives?