Trending

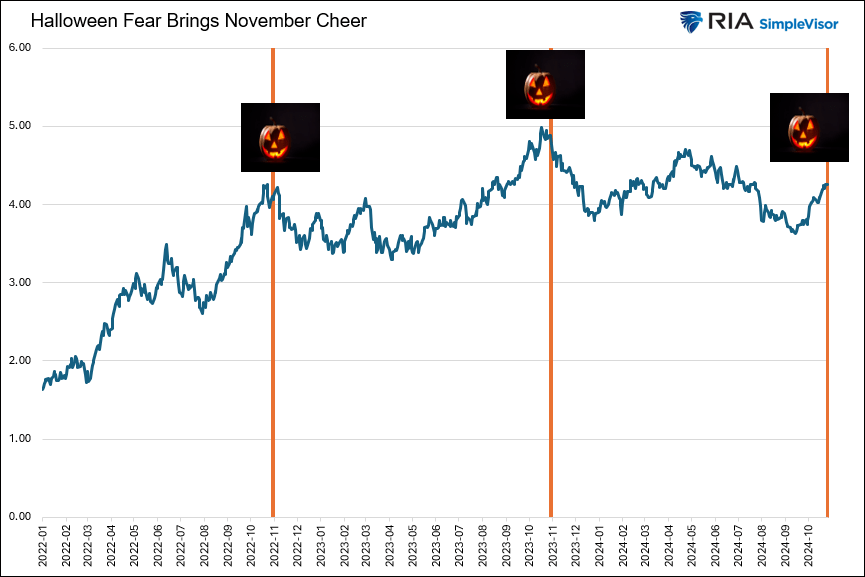

The last two Halloweens capped off a few frightful months for bondholders. However, as we share below, 10-year bond yields reversed course on Halloween in 2022 and 2023. Will 2024’s harrowing October for bondholders end with Halloween’s ghosts and goblins? Accordingly, will November be better for bonds as it has been for the last two years?

Despite the eerie correlation highlighted below, Halloween is insignificant to the bond market. However, what does matter is a slew of negative narratives about bond market fundamentals that cause fear in some bond investors. Additionally, famed investors Paul Tudor Jones and Stanley Druckenmill boost the fear as they publically “talk their books.” To help you navigate this tricky market, we add context around the recent bond bearish arguments to better appreciate what is happening with bond yields.

To wit:

The economy is about $8 trillion, or 33%, larger than it was on the eve of the Pandemic. Therefore, it’s not surprising the amount of debt has grown commensurate with that amount.

Following Japan’s path seems awfully bullish strictly from a bond holder’s perspective.

What To Watch

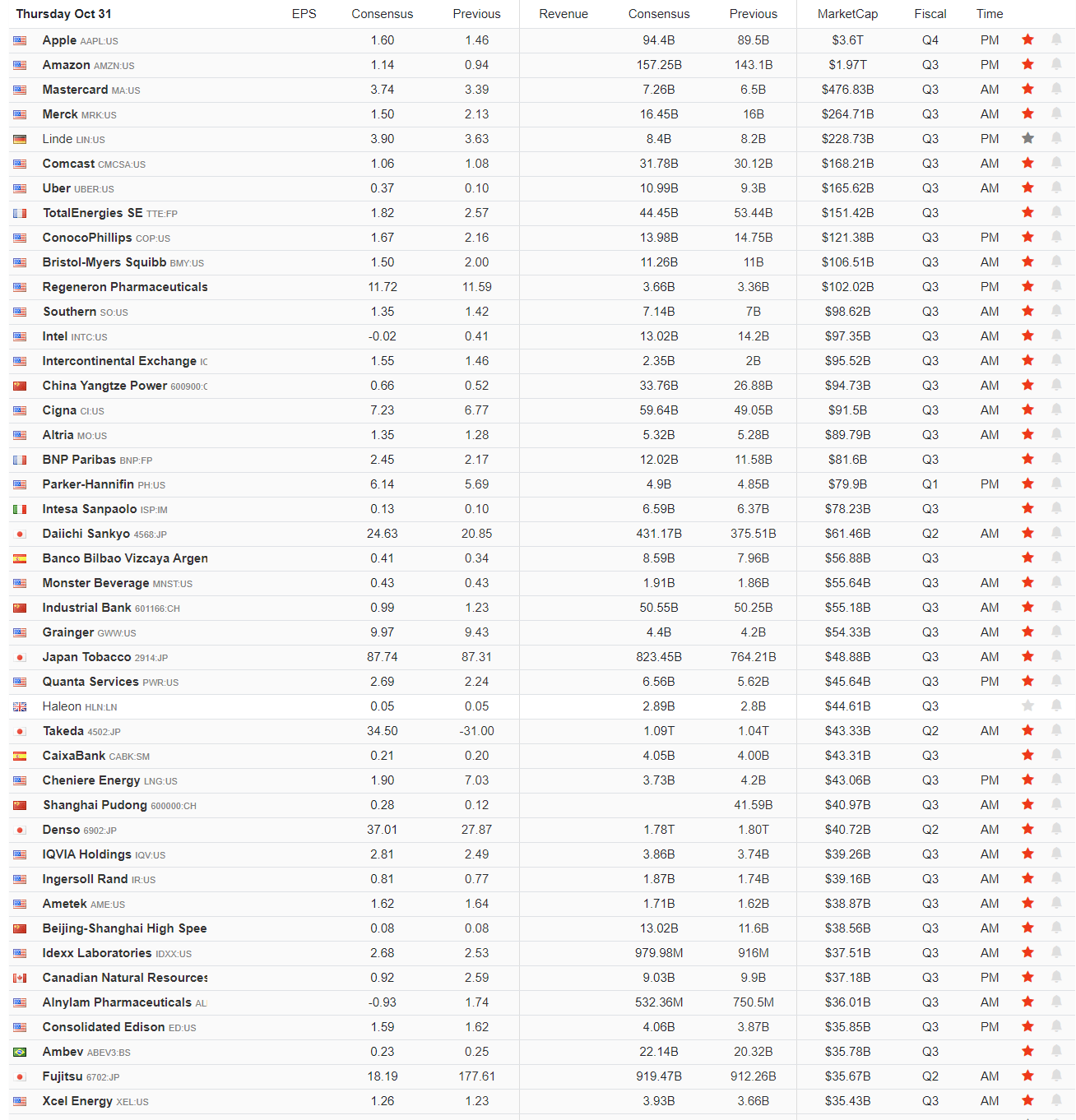

Earnings

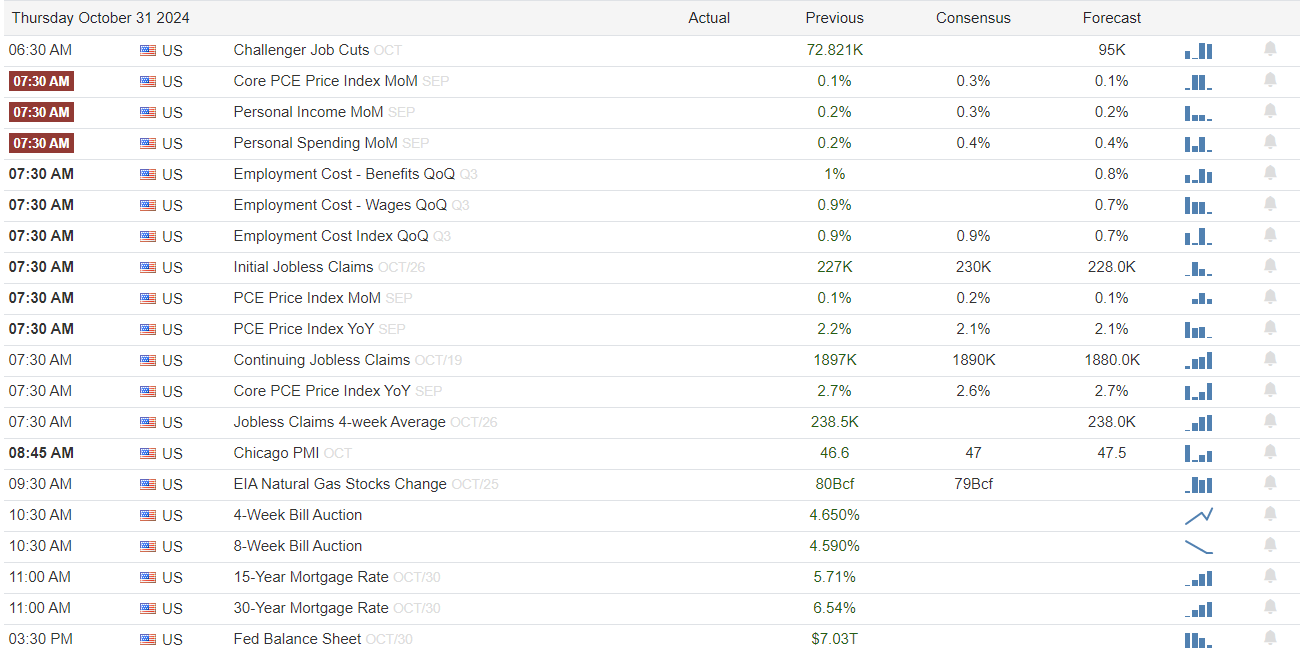

Economy

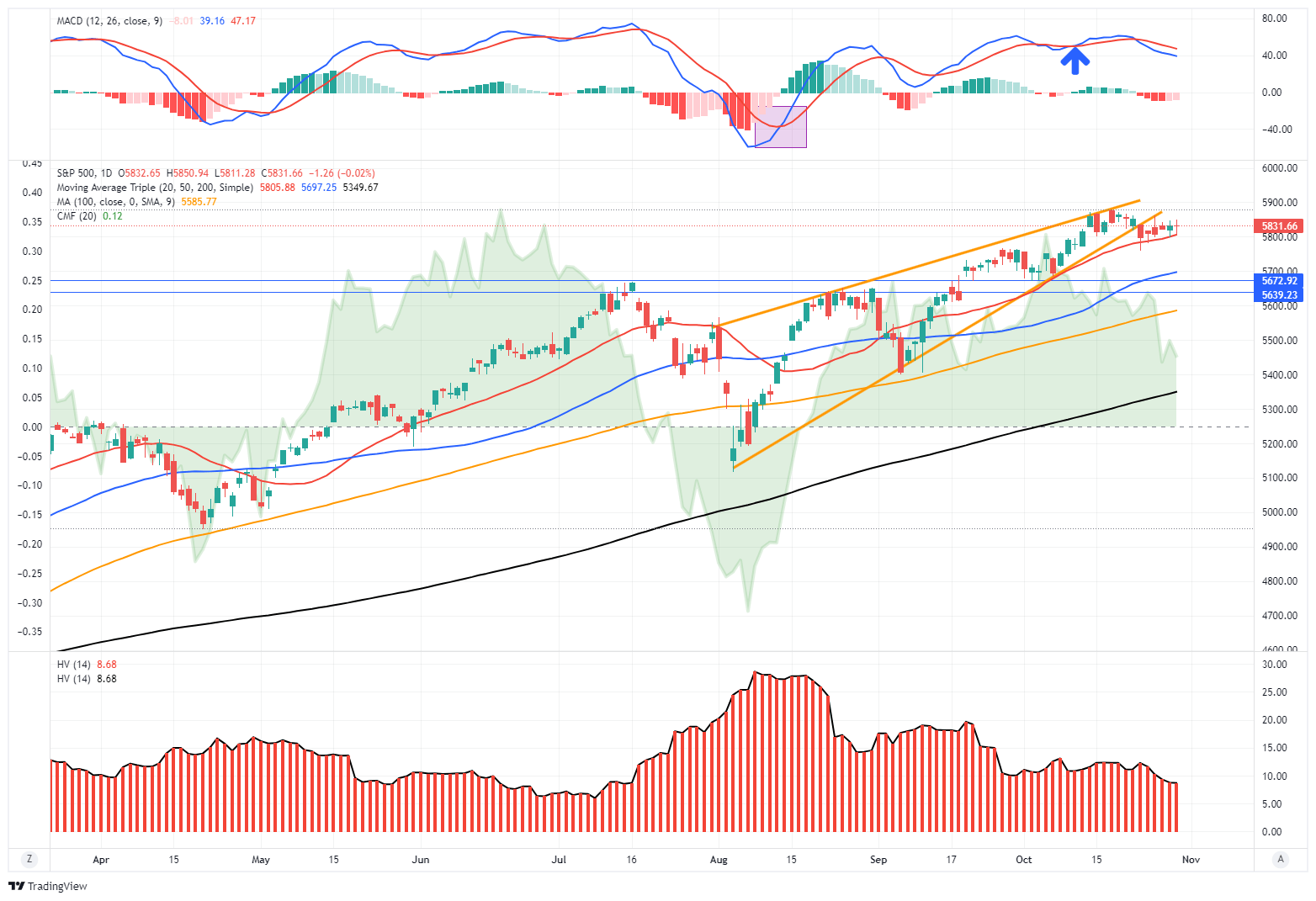

Market Trading Update

As noted yesterday, the market remains “stuck in neutral” over the last two weeks ahead of several key events. Tomorrow is “employment day,” when we will see the October numbers. A strong employment report could worry markets about reduced rate cuts from the Federal Reserve. On Tuesday is the election, with no small risk of a potential contested outcome. Then, on Wednesday is the Federal Reserve FOMC meeting, where we will get the latest update from the Fed on its rate cut decision and outlook. With the potential market volatility those events could unleash on the markets, it is quite surprising to see recent market action remain so calm.

The 20-DMA remains key support, with buyers repeatedly stepping in at that level. On the other hand, the upside remains contained to the underside of the broken rising trend line from the October lows. Notably, the previous “buy signal” has reversed to a “sell signal,” which currently limits the bulls. However, money flows are declining, which suggests that buying power is waning. With historical volatility at decently low levels, such sets the stage for a potential bearish reversal if something “unexpected” occurs.

We remain underweight equities and overweight cash in the near term with our core Treasury bond holdings intact to hedge against a sharp increase in volatility. That positioning is unlikely to change much over the next two months, and we are willing to sacrifice some performance in exchange for control over risk.

While we have discussed these simplistic rules over the last several weeks, we continue to reiterate the need to rebalance risk if you have an allocation to equities.

- Tighten up stop-loss levels to current support levels for each position.

- Hedge portfolios against significant market declines.

- Take profits in positions that have been big winners

- Sell laggards and losers

- Raise cash and rebalance portfolios to target weightings.

Keep moves small for now. As the markets confirm their next direction, we can continue adjusting accordingly.

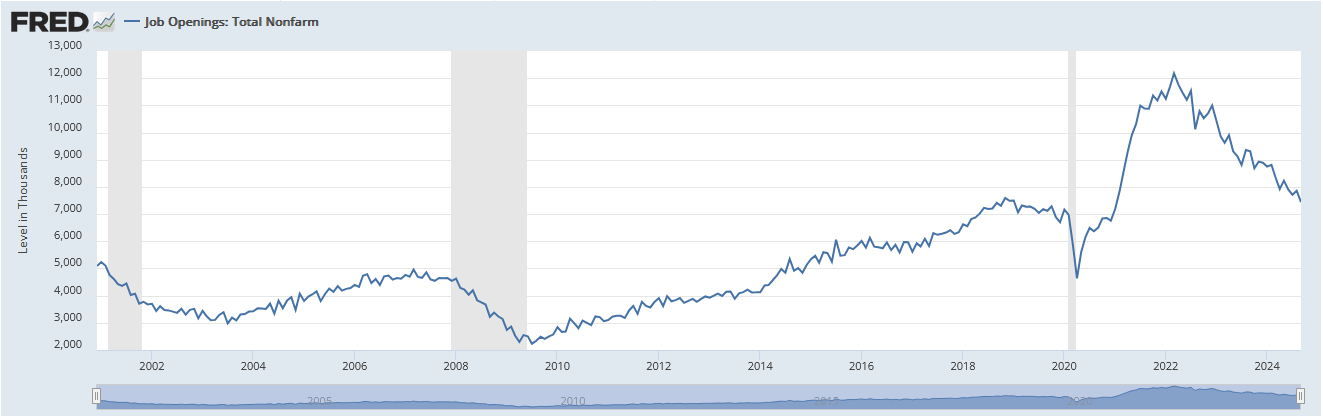

JOLTS and ADP

With the Fed seemingly more focused on the labor markets than inflation, the JOLTs and ADP reports help add context to whatever we will learn about the labor market from the BLS employment report on Friday. As shown below, the number of job openings in the JOLTs report fell sharply by 418k. Moreover, there were 165k layoffs and another 107k quits, more than offsetting the 123k hires. The data, which is delayed a month, contradicts last month’s solid BLS employment report.

While JOLTs portrayed weakness in the labor market, ADP was stronger than expected. ADP reports the workforce added 233k jobs last month, more than double expectations and 90k more than last month’s figure. We caution with JOLTs and ADP that seasonal factors can significantly affect labor market data this time of year and won’t be fully sorted out for at least a few months. Furthermore, the hurricanes also played a role that is hard to estimate. The current consensus estimate for Friday’s BLS report is 180k new jobs, with the unemployment rate increasing from 4.1% to 4.2%

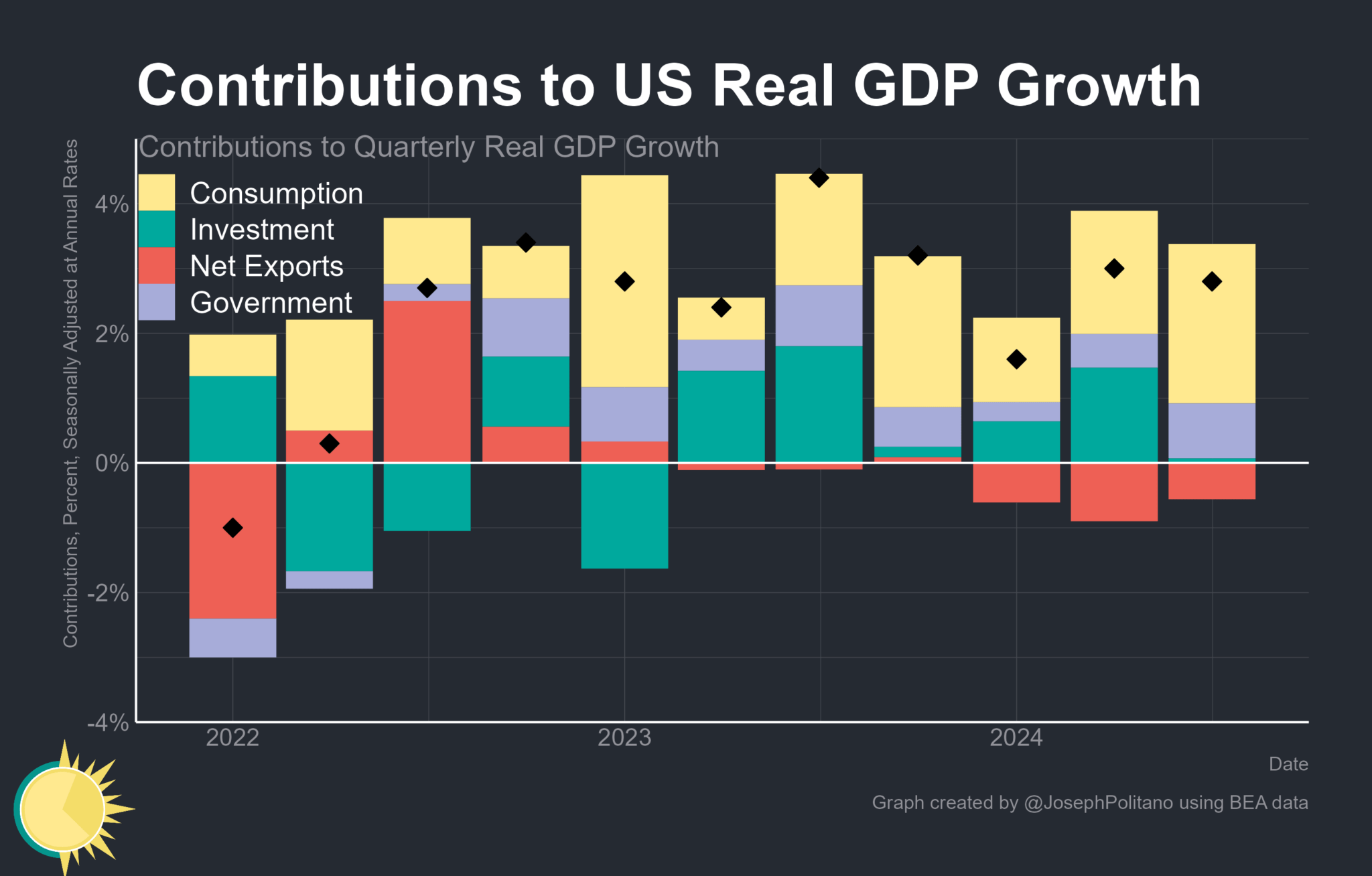

GDP Remains Robust

Third quarter GDP was a mixed bag of information. GDP fell 0.2%, slightly short of estimates at 2.8%. However, the PCE prices deflator was well below the consensus estimates at 1.5%. Wall Street economists thought it would come in around 2.5%. Therefore, GDP was 1% lower than estimated due solely to overforecasting inflation. The counter to the lower prices was higher than expected consumer spending. Consumer spending grew by 3.7%, above estimates of 3.0%. Generally, the data points to a strong consumer and a continued decline in inflation.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”