Trending

The question asked of us most often recently: “Why are bond yields rising?”

After verbally answering it plenty of times, it’s time to put our answer in writing for everyone to see. The answer will help you understand what is causing bond yields to rise, and more importantly, it will help you better appreciate when the trend may reverse.

Unlike short- and medium-term gyrations in stock prices, which are often due to changes in investor sentiment, the bond market has a much more fundamental grounding. Interest rates, representing the cost of money, strongly impact economic activity and inflation in a highly leveraged economy like ours. Thus, economic growth, inflation, and Treasury bond yields are highly correlated.

That said, bond investor sentiment does impact yields and can be relatively accurately quantified, unlike the stock market. In bond market parlance sentiment is called the “term premium or discount.”

Quantifying the term premium or discount and, equally important, understanding the market narratives responsible for the premium or discount is valuable. With such knowledge, one can assess whether the narratives make sense. Thus, is the premium or discount likely to be sustained? If the narrative(s) are illogical, there could be an opportunity to profit when the premium or discount normalizes.

With that, let’s better appreciate why bond yields are rising.

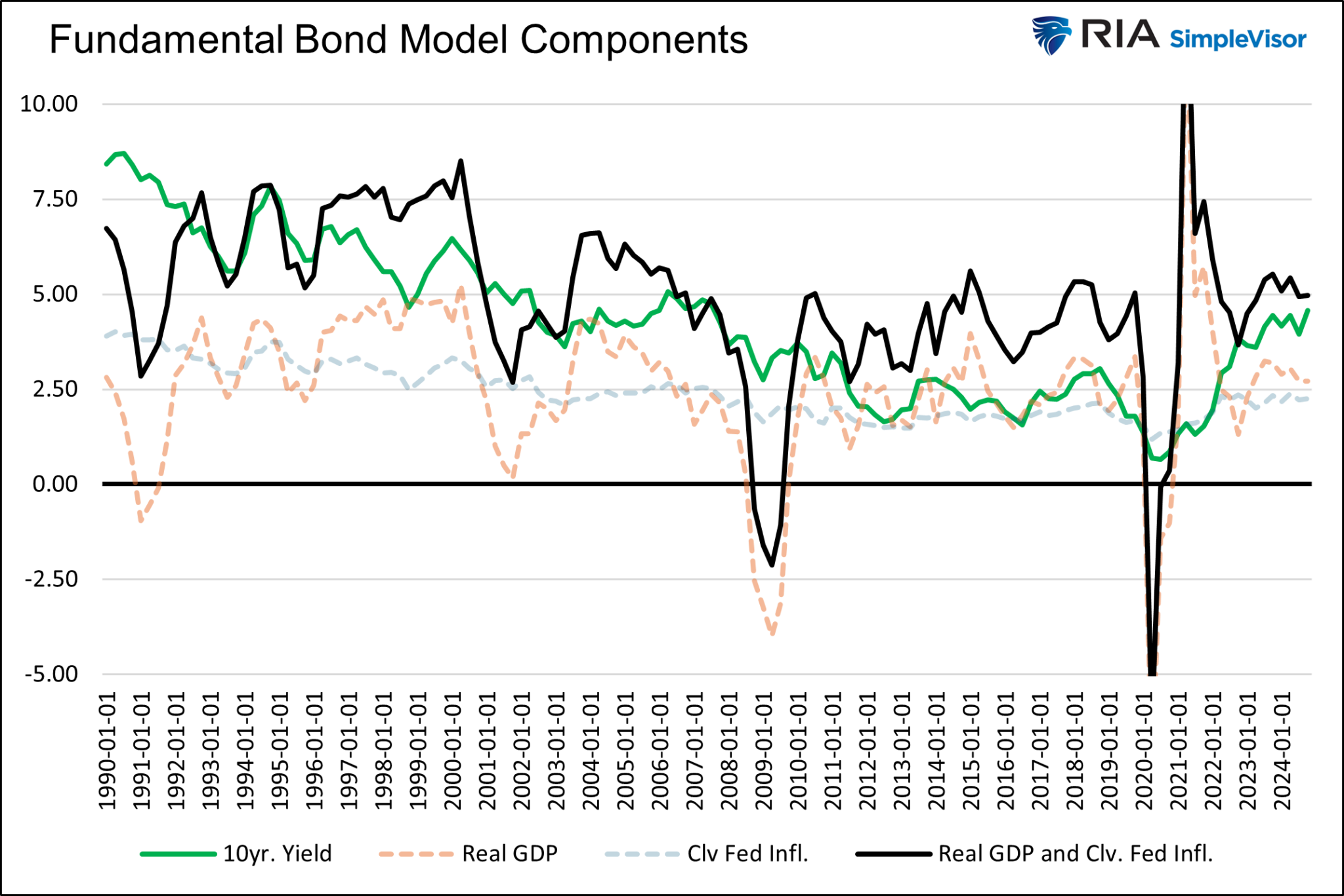

Fundamental Bond Yield Model

We created a relatively simple but highly effective proprietary fundamental yield model based on inflation and economic growth. Our bond yield model only uses two inputs.

- Inflation– The Cleveland Fed Inflation Expectations Model. Their model is unique as it uses actual inflation data and market and survey-based measures of inflation expectations. The combination of actual and expected price changes provides a complete inflation picture.

- Economic activity– Real GDP. Real GDP strips out inflation to estimate economic activity without the impact of price changes.

The graph below charts the two inputs alongside their sum and ten-year UST yields. We use faded coloration of the two inputs to highlight the correlation between the sum of both factors (black) and yields (green).

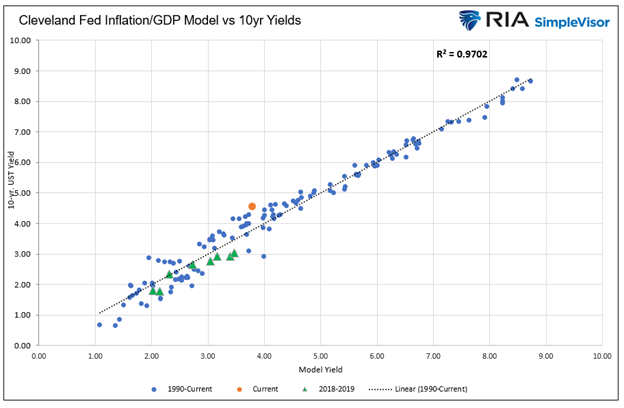

The graph above shows a decent correlation. However, to vastly improve the model, we ran a multiple regression analysis of the two inputs with yields. Doing so created a significant correlation with an r-squared of .9702. As we share in the two graphs below, the correlation is statistically and visually much more potent than that pictured above.

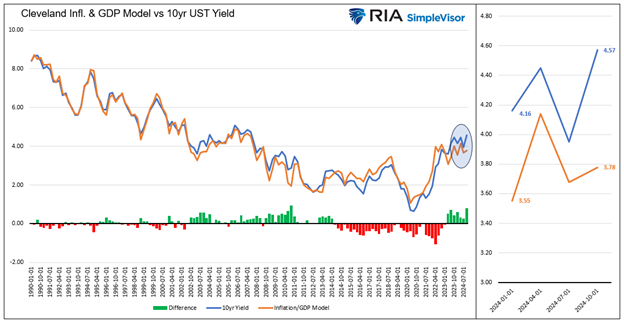

Model Yield Expectations

The line graph comparing the expected model yield to actual yields shows that the model yield is 3.78% versus the actual yield of 4.57%. The difference of .79% is the term premium. The bar chart in the first graph and the orange dot in the scatter plot put historical context to the degree of the premium.

Within the scatter plot we highlight the 2018-19 levels in green to show what will happen to 10-year yields if economic activity and inflation continue to normalize and the term premium goes away. Such should bring 10-year yields into the 2-3% range. If we assume an eight-year duration on ten-year bonds, bond holders should see a price return of 12-20%, plus additional returns from the 4+% annual coupon.

What Is Sentiment Worth?

The New York Fed defines the term premium as follows:

The compensation that investors require for bearing the risk that interest rates may change over the life of the bond.

Simply put, it’s the additional yield that investors require above and beyond those justified by economic activity and inflation. It quantifies bond market sentiment.

We believe there are many reasons for the current premium, but two are probably the most impactful.

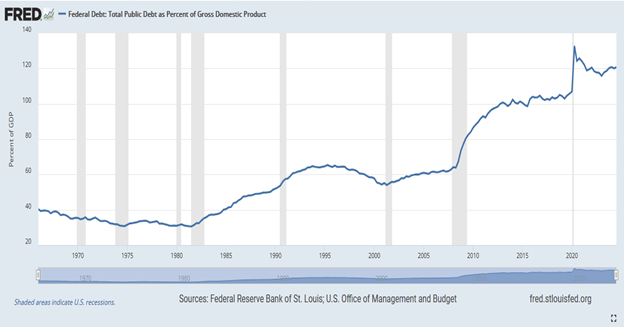

High Deficits

The market is drowning in Treasury debt, say some pundits. We do not necessarily disagree, but the statement needs context. To their point, over the last five years (2020-2024), the federal debt has grown by $12.2 trillion or nearly 9% a year. Despite five more years, the debt grew by $2 trillion less in the ten years prior.

Economists often compare debt to GDP to gain perspective on debt levels. The graph below shows that the federal debt-to-GDP ratio surged in 2020 but has since partially retreated. More importantly, it has remained relatively stable since 2022. While debt has been growing rapidly, economic activity, or the ability to fund it, has grown similarly.

Also important from a bond market perspective is the maturity of the new debt, not just the total amount of debt. The following comes from the New York Post:

Yellen has been moving away from long-term debt to finance the shortfalls to shorter-dated securities, essentially rolling over deficits with more and more Treasury bills instead of the normal way of debt issuance through 10- and 30-year debt. That’s according to an analysis by Robbert van Batenburg of the influential Bear Traps Report, who estimates that around 30% of all debt is the short-term variety — aka 2-year and shorter notes — compared to 15% in 2023.

Treasury Secretary Yellen has favored short-term debt to match strong demand from short-term debt investors. As a result, she is reducing long-term debt issuance as demand for long maturities has been relatively weak. Yellen is trying to match supply and demand to fund in the short and long run at the lowest cost.

The risk to her strategy is that yields could be higher when the short-term debt matures. The potential benefit is that yields fall. Thus, when the short-term debt needs to be rolled over, it gets refinanced at lower rates for longer maturities. Yellen is betting on lower yields in the future.

Regardless of the market opinions of Janet Yellen, she has done a good job managing the supply of long-term debt in the market. Thus, while deficits are higher than average, their impact on longer-term bond yields is much less concerning than some believe.

A change in strategy by the new Treasury Secretary will warrant reconsideration.

More Inflation

The other narrative negatively impacting bond yields is a palpable fear of inflation. We have written plenty on the topic, but it’s worth summarizing two key points.

First, the inflation surge in 2022 and the lasting effect was almost entirely due to broken supply chains and limited goods inventories coupled with strong demand due to massive government stimulus. An increase in demand coupled with a decrease in supply is inflationary. The condition has largely normalized and is highly unlikely to resurface.

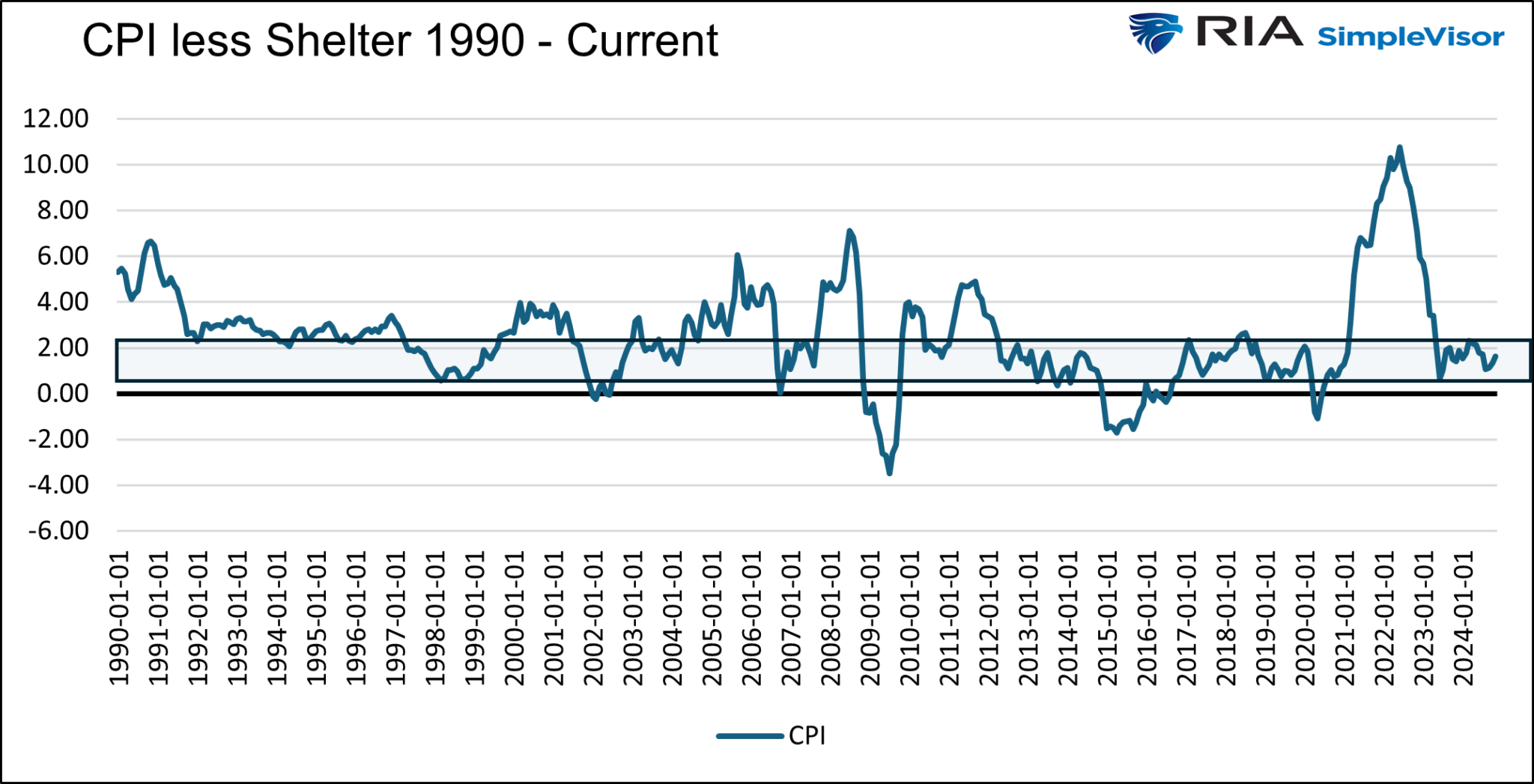

Second, inflation’s recent “stickiness” is primarily due to shelter costs. Within CPI, shelter accounts for over one-third of the index. Unfortunately, CPI shelter prices often significantly lag real-time shelter costs as rents are slow to reset, and housing prices used to impute rent also lag. As we share below, CPI excluding shelter costs is well within the 2018-2019 range. When CPI shelter catches down to near zero actual rental inflation, we suspect CPI will return to the Fed’s 2% target.

There are other narratives regarding inflation, but we find them highly unlikely, barring a sharp increase in economic activity or surge in government spending. If the economy slows, as it is globally, inflation should decline.

Summary

So why are bond yields rising? During the fourth quarter, the ten-year UST yield rose by 62 basis points. 52 basis points were due to the rising term premium, leaving only 10 basis points as the result of economic activity and inflation.

The two culprits behind the jump in the term premium were the fear of deficits and inflation. Even with no change to the fundamental factors, a sizeable return can be had in longer-term bonds if the premium diminishes. Furthermore, those returns could be supercharged if a recession, economic weakness, and/or a return to 2% or less inflation occurs.

Bond investors will most likely be rewarded handsomely when economic fundamentals normalize and the term premium fades. Until then, sentiment, not economic data, is the key factor impacting rates.

Related: Massive Outflows from TLT: What It Means for Investors