Trending

Written by: Meera Pandit and Margaret Byrne

After the worst year for bonds on record, bonds are back, providing opportunities for income and diversification at attractive valuations. However, with a potential recession on the horizon and vulnerabilities in the financial system, investors ought to be selective, gearing towards the highest quality areas of the bond market. Municipal bonds provide a particularly compelling opportunity within the fixed income landscape:

- Quality – Municipal issuers are well-positioned to weather slower growth given the cushion provided by healthy rainy-day funds, unspent federal aid, and conservative management practices over the past decade. While corporate and Treasury debt have increased by 50% and 100%, respectively, growth in municipal debt has been flat. Additionally, municipal default rates of 0.08% are significantly lower than investment grade corporates, with lower default rates across every ratings bucket.

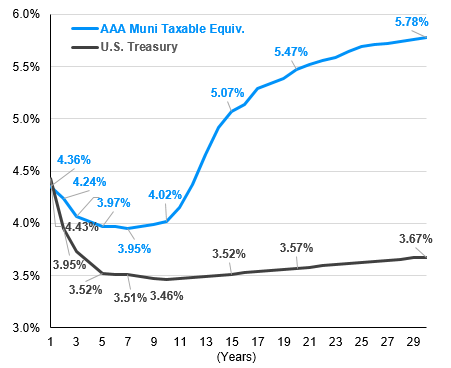

- Income – The Federal Reserve (Fed) has raised rates 475 basis points (bps) over the last year, pulling yields up across the curve. Municipal 10-year rates have risen over 125 bps since 2021, but the taxable-equivalent yield has increased even more, by 228 bps to 4.02%, comparing favorably to U.S. Treasury bonds yielding 3.46%.

- Valuations – Rapidly rising rates and record mutual fund outflows of nearly 152 USD billion in 2022 pressured valuations. Looking ahead, the municipal market should benefit from continued strong retail demand and lighter supply, which year-to-date (YTD) is running 25% lower than last year. If small to intermediate-sized banks are forced to pare back on their holdings of high quality, long duration municipals, this could present opportunities at the long end of the curve.

The best opportunities in the municipal market today are in high quality bonds across most sectors. Unlike Treasuries, the municipal yield curve is steep, offering opportunities to add duration - which we think makes sense now - and earn yield, particularly in the 12 to 18-year part of the curve.

After years of extremely low yields, many portfolios are under-allocated to core fixed income. Municipal bonds offer opportunities to boost those allocations with high quality bonds that provide solid income at reasonable valuations. These benefits are pronounced for taxpayers, who can add a high-quality diversifier to help build income streams that can better protect portfolios in volatile markets.

Muni taxable-equivalent yield curve vs. Treasury yield curve

Source: Bloomberg, TM3, J.P. Morgan Asset Management. Municipal taxable-equivalent yield assumes a top tax rate of 37% plus the 3.8% Medicare tax for a total tax rate of 40.8%. Labels shown represent 1, 2, 5, 7, 10, 15, 20, and 30-year yields. Data are as of March 23, 2023.