Trending

Written by: Gershon M. Distenfeld, CFA and Scott DiMaggio, CFA

Today’s market environment taps into bond investors’ primal fears. Extremely low yields make it tough to find sufficient income and potential return. Economic growth is rebounding from its 2020 collapse, but the world’s grip on recovery is uncertain. Massive fiscal stimulus could resurrect inflation, a long-dormant risk that investors are rusty at addressing. And rebounding growth has fueled rising yields—ironically, contributing to, rather than alleviating, yield-starved investors’ anxieties.

Inflation and Rising Rates: Scanning the Horizon

We agree that the global economy is on the cusp of a new, more inflationary regime. Initial signs may appear as base effects and higher commodity prices push headline inflation in advanced economies temporarily higher. But we don’t expect significant and sustained inflation anytime soon.

We also don’t think interest rates will rise dramatically. It’s likely that global economic growth will accelerate in the second half of the year. But even if inflation begins to materialize, policymakers aren’t inclined to let rates rise too far, too fast, which could endanger a fragile recovery. They’re especially likely to step in if rising yields threaten to knock risk assets off course.

The result? Yields in most markets will probably stay low through 2021. Even in the US, which is likely to grow faster than other developed economies, the 10-year Treasury yield is likely to end 2021 around 1.75%—higher than today, but still lower than pre-pandemic levels.

Don’t Put Your Portfolio on Autopilot

Still, with massive stimulus funds sloshing around the global economy, it’s prudent to be prepared—and that means staying active.

It can be tempting to opt for a passive approach in fixed income. Passive strategies let investors sit back and enjoy the ride. But the ride may be more dangerous than many realize. In fact, pressing the autopilot button today could make you overly vulnerable to rising interest-rate and inflation risks. It also exposes you to volatility in risk assets as uncertainty persists around the path of recovery.

In contrast, active managers can control multiple levers and dials to navigate current and changing market winds. Below are three adjustments we think investors should consider today.

1. Dial down duration—but not too much.

When facing a rising-rate environment, investors who can’t stomach too much risk should limit—but not eliminate—duration, or sensitivity to interest-rate changes.

Shortening duration can help mitigate volatility and losses as interest rates rise. Moderately trimming duration can also be an effective hedge against inflation risk.

But don’t shift to cash or drastically shorten your duration exposure, for two reasons. First, this strategy could soon have you lagging both income-generating bonds and inflation. Second, the government bonds that provide duration serve as an offset to credit- and equity-related losses—even when bond yields are low or negative.

In other words, if risk assets are the locomotive that generates high returns, duration is the track that keeps the train in line. Take away the track and you risk derailing your portfolio. (And don’t try to time increases in yield, either. Even the most seasoned bond managers can’t do that.)

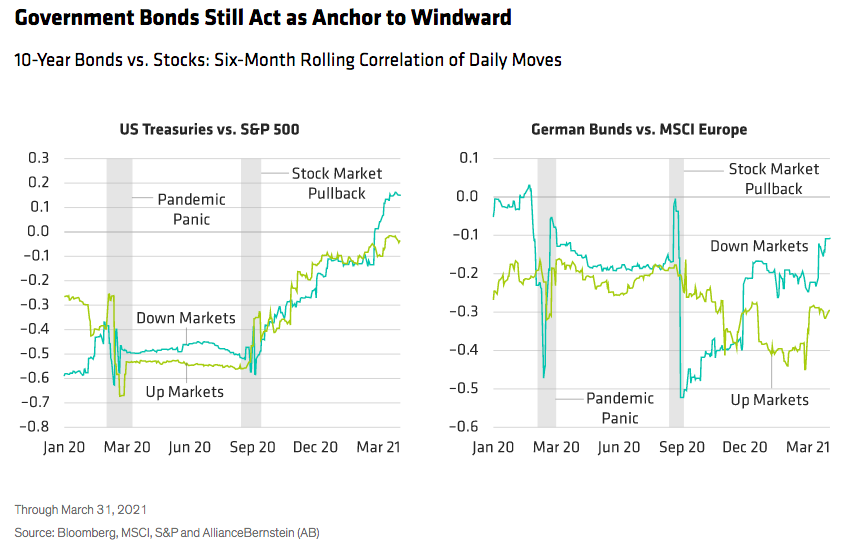

Last year’s coronavirus sell-off provides important insights into the role of government bonds in an allocation. In fact, government bonds were one of the few true offsets to equity-market volatility when stocks crashed in February–March 2020 and again during the pullback in September.

On days when US stocks fell in 2020, the correlation between US Treasuries and the S&P 500 (Display, below left) remained below –0.4. And in Europe, yields on 10-year German Bunds were well into negative territory when stock markets fell in March and September. But correlations between Bunds and the MSCI Europe Index (Display, below right) became even more negative during those sell-offs, falling to around –0.5. In other words, government bonds became more defensive when defensiveness was needed most.

Correlations can be unstable. Over the last three decades, the inverse correlation between stocks and bonds has broken down several times. Most recently, in early March, rising US Treasury yields (and falling bond prices) prompted weakness in equities, resulting in a very low positive correlation between the markets. Historically, though, these episodes have been brief, and the correlation has always returned to negative territory.

Correlations can be unstable. Over the last three decades, the inverse correlation between stocks and bonds has broken down several times. Most recently, in early March, rising US Treasury yields (and falling bond prices) prompted weakness in equities, resulting in a very low positive correlation between the markets. Historically, though, these episodes have been brief, and the correlation has always returned to negative territory.

In the near term, we expect occasional blips of the correlation between Treasuries and stocks into low positive territory, thanks to supportive central banks and a periodic repricing of bond yields as the economy recovers. But over the longer term—and particularly during risk-off events—we believe negative correlations will prevail and government bonds should provide an essential anchor to windward.

2. Balance opposing risks.

While duration provides a buffer against credit-related losses, a healthy allocation to diverse sources of credit allows investors to participate on the upside when risk assets rally. That’s precisely why most investors need to hold both return-seeking assets and risk-mitigating assets.

In fact, among the most effective active strategies are those that combine government bonds and other interest-rate-sensitive assets with growth-oriented credit assets in a single, dynamically managed strategy.

This approach can help managers get a handle on the interaction between interest-rate and credit risks and make better decisions about which way to lean at a given moment. The ability to rebalance negatively correlated assets helps generate income and potential return while limiting the scope of drawdowns.

3. Lean into credit.

At this stage of the recovery, we think investors should consider tilting this balance toward credit. Risk assets such as high-yield corporates tend to outperform in a rising-rate environment, especially when inflation expectations are rising. That’s because such conditions typically go hand in hand with solid economic growth that’s supportive of credit. If that sounds familiar, it’s because that’s our environment today.

Investors with serious concerns about rising inflation might consider explicit inflation-protection strategies. But investors aren’t limited to inflation-linked bonds in developing an all-weather portfolio.

With attractive relative yields and low correlations to government bonds, many credit sectors play a defensive role in inflationary and rising-rate environments. The key is to diversify. Look for compelling risk/reward profiles across sectors and regions with varying inflation and interest-rate regimes. And be selective. Fundamentals matter.

In a world with over US$17 trillion of negative-yielding debt, pockets of the global corporate credit market stand out as a sizeable group of assets offering attractive levels of yield. Fundamentals are broadly supportive, companies have taken advantage of low rates to strengthen their liquidity buffers, and supply and demand conditions are very favorable.

Financials should benefit from an economic recovery and rising rates. As interest rates rise, so do bank margins, improving banks’ credit profiles. In Europe, for example, yields on subordinated Additional Tier 1 bonds of European banks exceed those of other European and US high-yield issuers, while their balance sheets have been bolstered by improving capital and liquidity ratios.

For a healthy yield pickup over investment-grade corporate bonds, fixed-income investors can tap US securitized assets, whose underlying cash flows come from different sources than corporate credit. In particular, we believe credit risk–transfer (CRT) securities—residential mortgage-backed bonds issued by US government-sponsored enterprises—are especially attractive. CRTs enjoy strong fundamentals, thanks to resilient demand in the US housing market. Thanks to their floating rates, CRTs offer protection against rising rates and a solid defense against inflation.

We also expect emerging-market debt to be buoyed by the weaker US dollar, continued fiscal stimulus, attractive valuations and strong investor demand for income in a low-yield environment.

What do these diverse sectors have in common? They should all benefit if vaccine rollouts continue, economies reopen and growth rebounds, prompting a tightening of credit spreads.

Rising Rates Benefit Investors in the Long Run

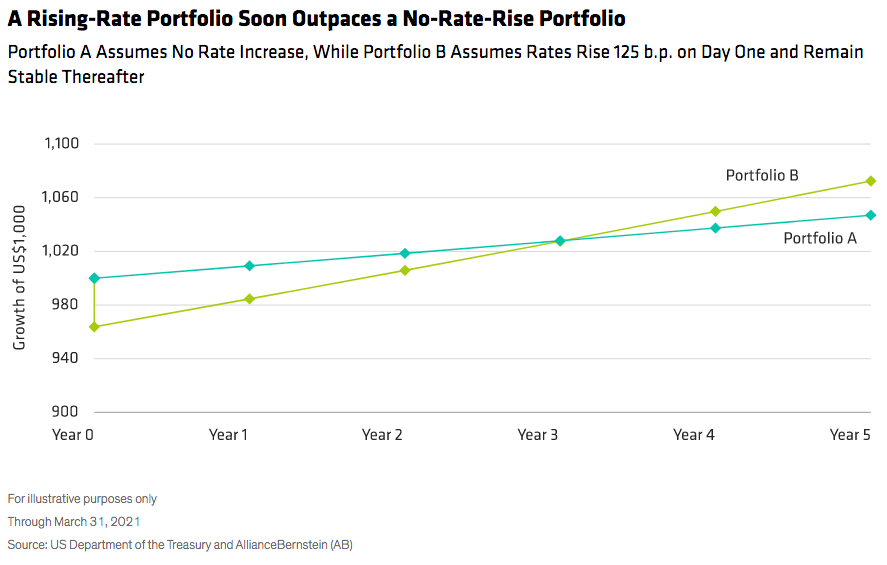

We know that rising bond yields can be painful in the short term as prices fall. But in the long run, rising rates are good for bond investors. Here’s why: the income bonds generate in the form of coupon payments gets reinvested at new and higher rates.

Let’s walk through an example to show what the actual impact of rising rates might be on a bond portfolio. We’ve modeled a simple portfolio of Treasury bonds and “shocked” it by assuming a sudden 125-basis-point rise in rates. What would its immediate performance look like? And then, how would the following years unfold (Display)?

At first, the portfolio sees an initial price loss—an undeniably painful experience. Even so, the portfolio still generates income, and investors who stay the course can reinvest that income at a higher yield. This helps to make up for the price loss and eventually offsets it altogether; in less than two years, our portfolio is back in the black. And in year three, the portfolio has not only caught up to where it would have been had rates never risen, but thereafter it’s worth more and is growing faster. At that point, you’re better off.

Here’s our rule of thumb: as long as the duration of your portfolio is shorter than the investment horizon, rising rates will benefit you—no matter how large the rate increase.

In fact, with the right strategies in place, rising rates can help keep your entire asset allocation aloft.

Related: Four Things Investors Should Know About US Inflation in 2021