Trending

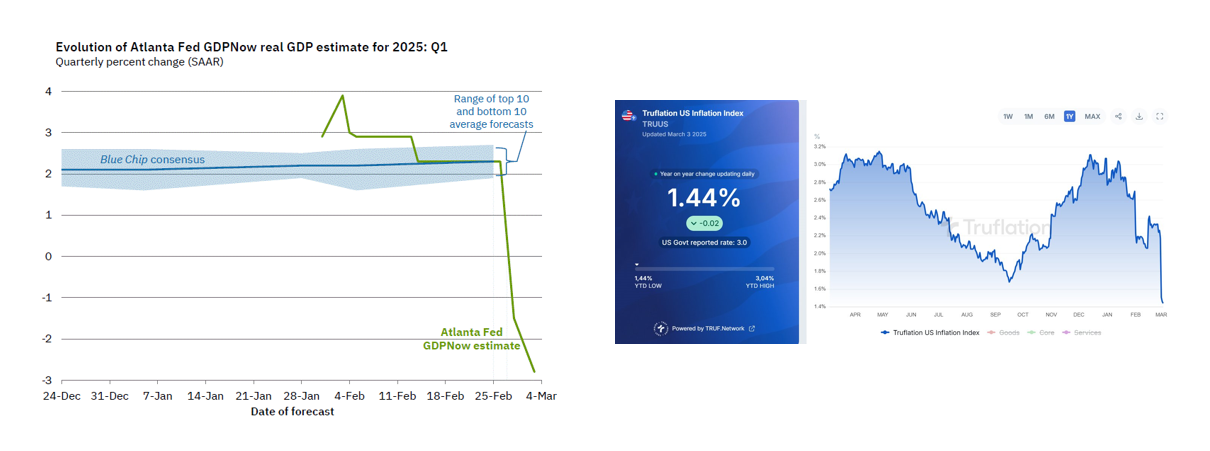

What a difference a month makes. In mid to late January, the bond vigilantes were shorting bonds while warning that bond yields would increase due to a robust economy, large federal deficits, and higher inflation. The ten-year US Treasury note yield peaked at 4.89% on January 13. Since then, it has fallen .72% to 4.17%. Recently, the downdraft in yields has picked up speed. Such is unsurprising given how quickly estimates for the most significant driver of yields, economic activity, and inflation have plummeted. As we wrote on January 8th in Why Are Bond Yields Rising?:

Interest rates, representing the cost of money, strongly impact economic activity and inflation in a highly leveraged economy like ours. Thus, economic growth, inflation, and Treasury bond yields are highly correlated.

In mid-January, the bond vigilantes’ saber-rattling pushed yields almost 1% above their fair value, as we share in the article. Since then, the term premium has significantly fallen. Two estimates of inflation and GDP are shown below to explain why this is occurring. The Atlanta Fed GDPNow estimates first quarter growth of -2.8%. That is almost a 5% decline from its estimate a week ago. The Truflation prices estimate, which has a good track record of leading CPI by 45 days, has fallen from nearly 3% in January to 1.44% today. Weakening economic activity, lower inflation forecasts, optimism over deficit cuts, and an evaporating bond term premium result in lower yields. While bonds are overbought short-term, there is much more price upside if the GDP and CPI estimates are prophetic. Moreover, bond vigilantes still have a lot of short bets to cover, potentially adding fuel to the fire.

What To Watch

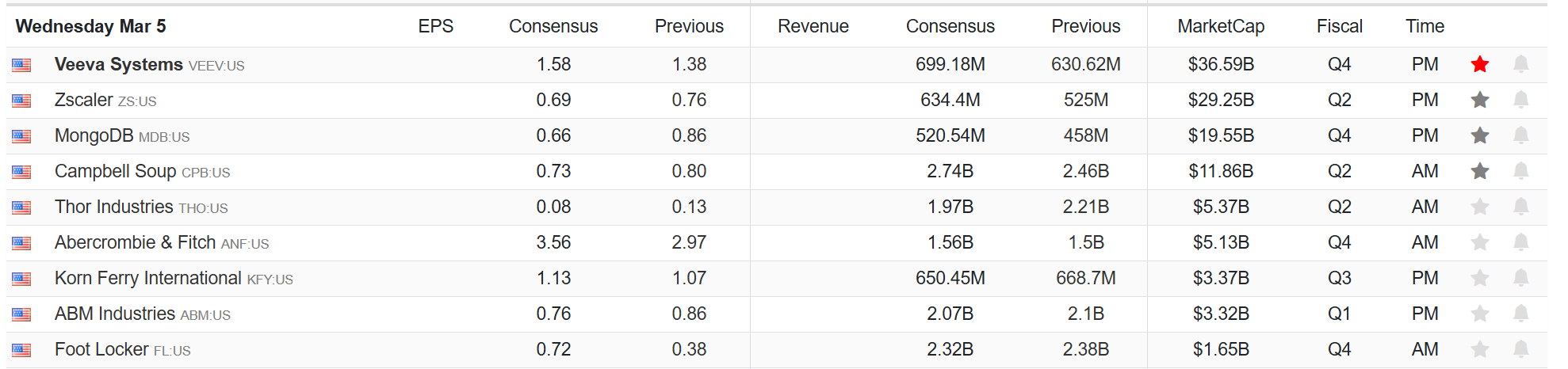

Earnings

Economy

Market Trading Update

In yesterday’s note, we discussed the stagnation of market breadth as the market continues its current corrective phase. The sell-off has been focused primarily on technology and discretionary as of late, but yesterday, we saw it spread into the rest of the market, and profit-taking hit some of the recent winners. The driver behind the sell-off has been the resurgence of tariffs and a slate of weaker-than-expected economic data. Such is not unexpected, as we have discussed it since the beginning of the year.

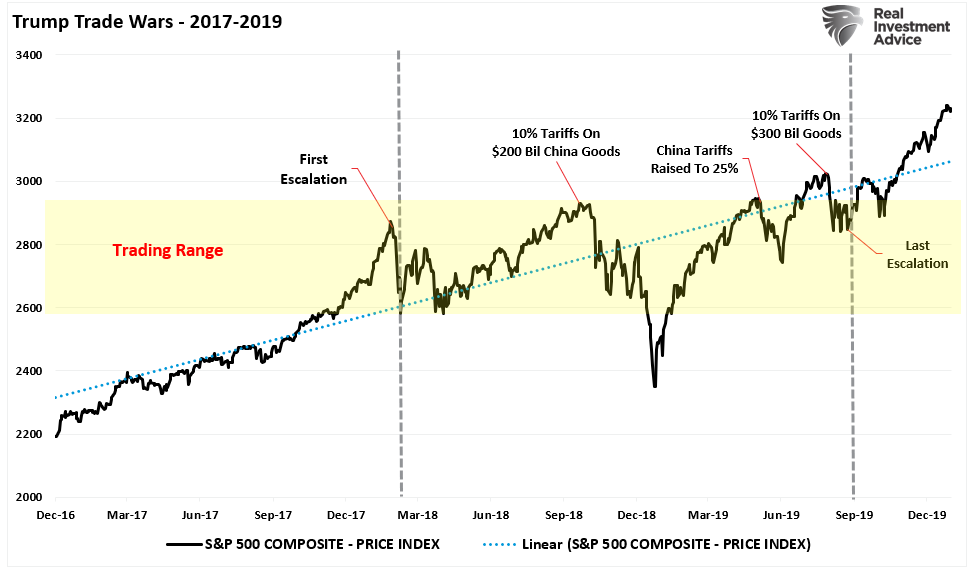

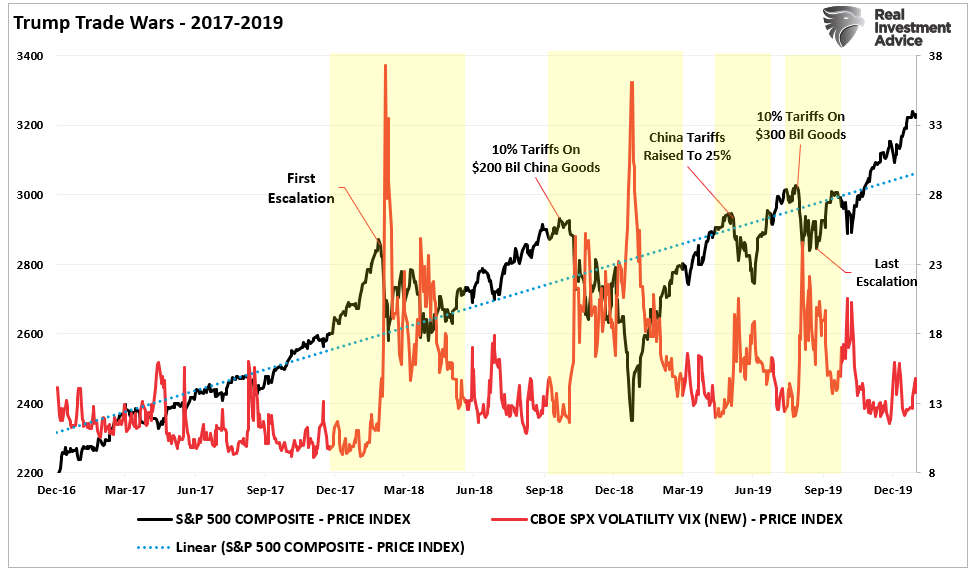

However, what is happening in the markets is very similar to what we saw during President Trump’s first term when he initiated a trade war with China. To draw some conclusions, let’s review the market’s reaction to tariffs.

Many headlines suggest that Trump’s tariffs will cause the next major market crash. Maybe that is the case. There is always a possibility of “something breaking.” However, looking at Trump’s first term in office shows how the markets reacted as the China “trade war” developed. Following the passage of the “Tax Cuts and Jobs Act,” the market surged to all-time highs. Valuations were elevated, and the Fed was beginning a rate-hiking campaign. At the same time, Trump launched the first escalation of the trade war with China. Over the next 18 months, the market traded in a vast trading range but remained in a steady, higher linear growth trend.

As noted in “Curb Your Enthusiasm,” this year may be very similar to what we saw during the first trade war with bouts of volatility. As shown, as different facets of the trade war developed, the impact of tariffs caused short-term volatility spikes as investors digested the actions and their potential ramifications on the market. However, those spikes in volatility were short-lived as the impact of tariffs was quickly absorbed.

Despite the barrage of negative headlines, concerns about inflationary impacts, and economic outcomes, the market ultimately weathered the trade war. As is often the case with more dire predictions, the worse potential outcomes failed to appear. There is no denying that the “trade war” did induce a significant amount of volatility, which made it difficult for investors to “stay the course.” However, in hindsight, we can now see that those spikes in volatility provided repeated buying opportunities for investors to pick up stocks at lower prices.

Will this time be the same? Maybe.

However, with the market profoundly oversold and sentiment extremely bearish, I would more likely be a buyer here rather than a seller. But, even with that said, rallies are likely to be punctuated with more declines as volatility remains a close companion for the rest of this year.

Trade accordingly.

Fed Rate Cuts Back On The Radar

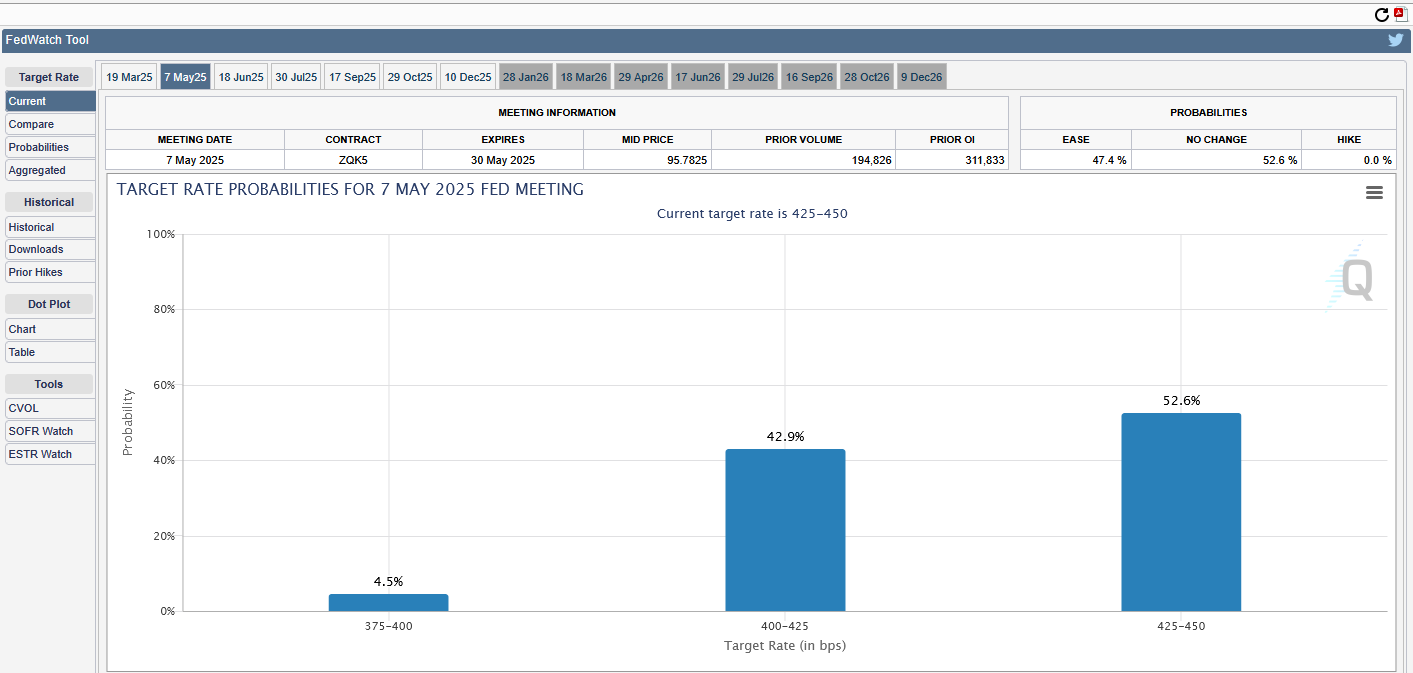

About two weeks ago, Wall Street believed the Fed would not cut rates this year. Sentiment is changing quickly, which aligns with the data we shared in the opening. As we share below, the Fed Funds futures market is now pricing in a 50/50 shot of a rate cut at the May 7th meeting. While slim, it does price a 10% chance they will cut as early as March 19th. Year-end projections are now between .75% and 1% of rate cuts.

While the equity markets are volatile and forecasts for growth and prices are declining, the Fed will want hard evidence that prices are definitively heading lower and/or the unemployment rate is starting to jump. Barring liquidity problems in the capital markets, we think the Fed will want at least a few months of weak data before reacting. A May cut may be a stretch, but we have certainly seen stranger things.

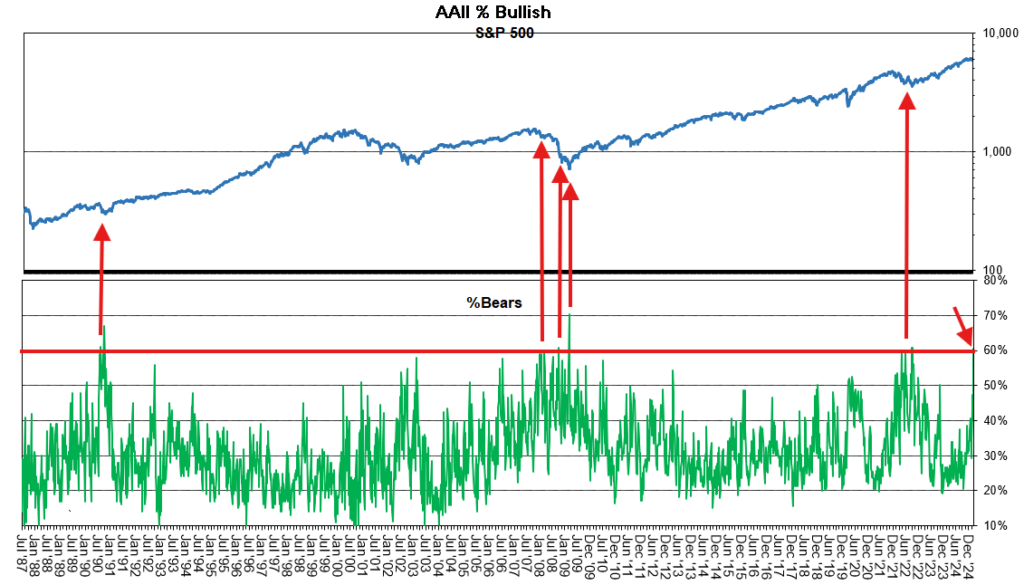

Bearish Sentiment Surges As If The Market Just Crashed

Investors’ bearish sentiment has surged to levels that generally align with previous market corrections and crashes. While concerns about the recent market correction have risen, and bearish headlines are rampant, investor sentiment has become so bearish that it’s bullish.

While that may be hard to fathom, negative sentiment occurs near market lows from a contrarian investing view. S&P’s Sam Stovall once said, “When everyone is bullish, who is left to buy?” The opposite is also true.

One of the hardest things to do is go “against” the prevailing bias regarding investing. As Howard Marks once stated:

“Resisting – and thereby achieving success as a contrarian – isn’t easy. Things combine to make it difficult; including natural herd tendencies and the pain imposed by being out of step, particularly when momentum invariably makes pro-cyclical actions look correct for a while.

Given the uncertain nature of the future, and thus the difficulty of being confident your position is the right one – especially as price moves against you – it’s challenging to be a lonely contrarian.”

\Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Related: Surging Bearish Sentiment: A Warning Sign or Overreaction?