Trending

Here we go again. After plunging to new lows, the calls for the end of the “bond bull” market mount each time rates rise. Is this time the end of the “bond bull?” Or, is there another huge bond-buying opportunity to come?

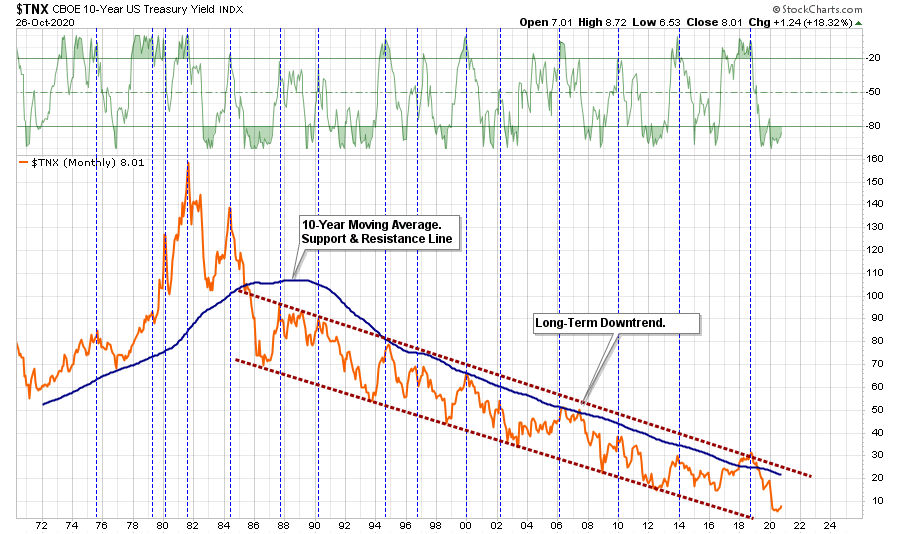

We recently reduced our exposure to bonds, the first time in years, due to the more extreme overbought condition of Treasury bonds following the pandemic’s onset. The long-term chart of yields below shows this to be the case.

There are two critical points to take away from the chart above.

- Interest rates are currently extremely oversold (top and bottom panels), suggesting that rates could indeed rise over the next few months. Such could coincide with another stimulus package or the passage of an “infrastructure” bill that leads to short-term inflationary concerns.

- When rates do rise from deeply oversold levels, there is a point where high rights collide with debt levels triggering either a credit-related event, a stock-market correction, or worse.

There are currently two significant risks from rising interest rates, which investors should heed.

Valuation Expansion

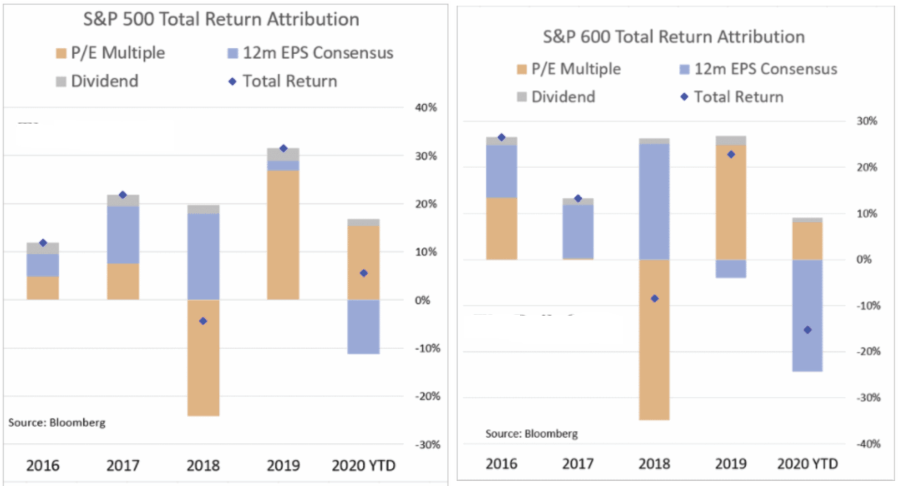

One of the primary themes used by the “Permabulls” is that “valuations are cheap due to low interest rates.” That argument has been the clarion call of a generation of investors who have ignored fundamentals and valuations to chase market returns.

Since 2019, when earnings growth began to deteriorate in earnest, investors bid up shares. As such, the primary driver of returns, as shown below, has come from “multiple expansion.”

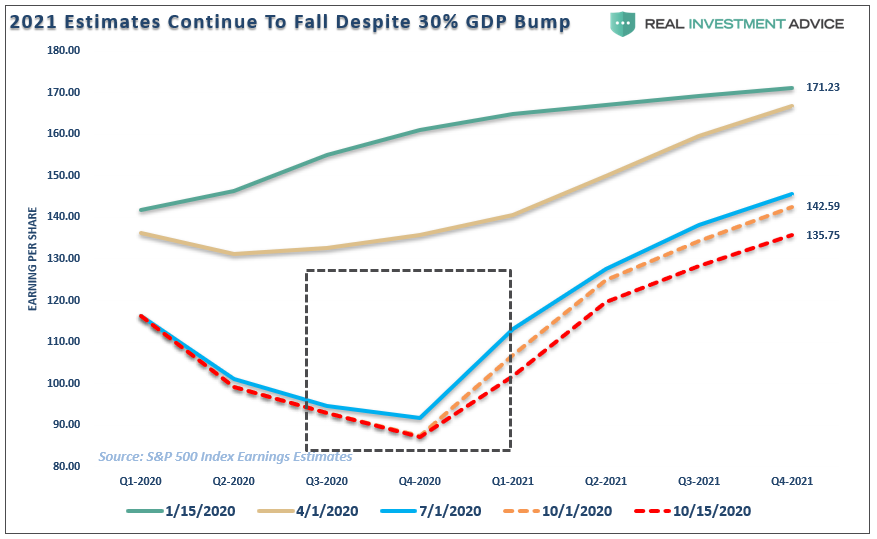

The “hope” remains that earnings growth will eventually catch up with valuations. However, despite being 3/4ths of the way through 2020, the outlook for earnings continues to deteriorate. In just the last 15-days, the estimates for 2021 have declined by almost $7 per share despite repeated statements of a recovering economy.

There are two problems with the thesis that “low rates justify high valuations.”

- Historically, such has not ever been the case; and,

- When rates rise, valuations quickly become an issue.

However, since stock prices reflect economic growth, the impact of rising rates on the economy is a far more significant issue.

The Debt Problem

People don’t buy houses or cars. They buy payments. Payments are a function of interest rates, and when interest rates rise sharply, mortgage activity falls as payments rise above expectations. In an economy where roughly 70% of Americans have little or no savings, an adjustment higher in payments significantly impacts consumption.

- Rising interest rates raise the debt servicing requirements, which reduces future productive investment.

- As stated above, rising interest rates will immediately slow the housing market taking that small contribution to the economy. People buy payments, not houses, and rising rates mean higher payments.

- An increase in interest rates means higher borrowing costs. Such leads to lower profit margins for corporations reducing corporate earnings and financial markets.

- The negative impact on the massive derivatives and credit markets is the Fed’s worst fear.

- As rates increase, so does the variable rate interest payments on credit cards. With the consumer struggling with stagnant wages and increased living costs, higher credit payments lead to a contraction in spending and rising defaults.

- Rising defaults on debt service will negatively impact banks, which are still not adequately capitalized and still burdened by massive levels of bad debts.

- Many corporate share buyback plans and dividend issuances are accomplished through cheap debt, leading to increased corporate balance sheet leverage. That will end.

- Corporate capital expenditures are dependent on borrowing costs. Higher borrowing costs lead to lower CapEx.

- The deficit/GDP ratio will begin to soar as borrowing costs rise. The many forecasts for lower future deficits will crumble as new forecasts begin to propel higher.

Payments Matter

I could go on, but you get the idea as we discussed concerning debt-to-income ratios:

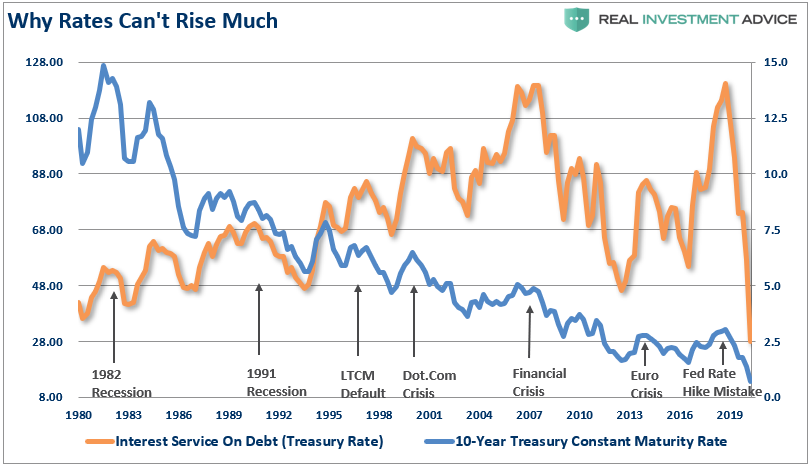

“Such is also why interest rates CAN NOT rise by very much without triggering a debt-related crisis. The chart below is the interest service ratio on total consumer debt. (The graph is exceptionally optimistic as it assumes all consumer debt benchmarks to the 10-year treasury rate.) While the media proclaims consumers are in great shape because interest service is low, it only takes small increases in rates to trigger a ‘recession’ or ‘crisis’ event.”

Am I saying rates can’t rise at all?

Absolutely not. However, there is a limit before it negatively impacts the economy, and ultimately the stock market.

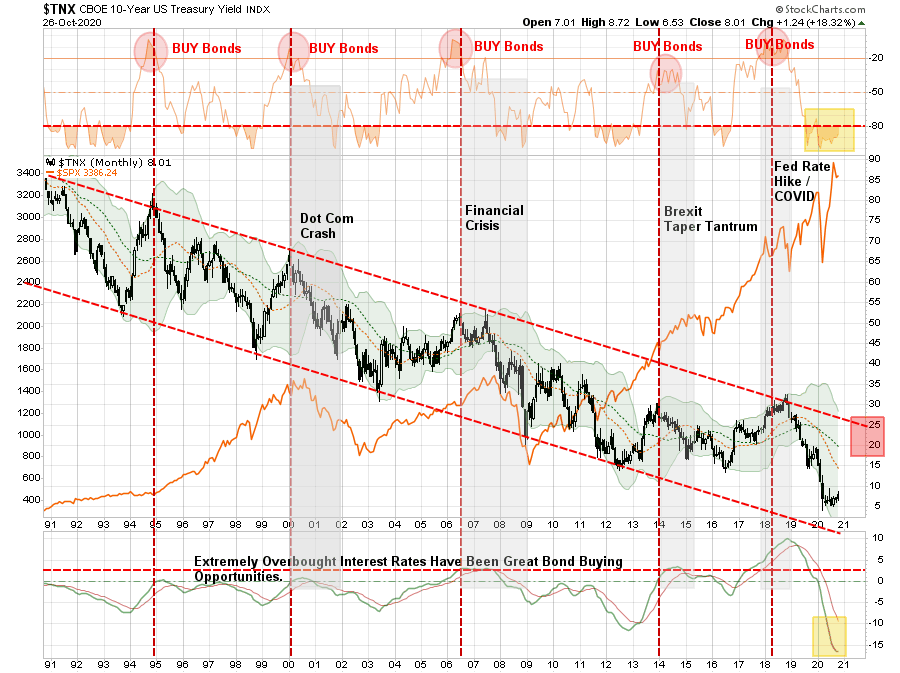

Bond Prices Very Overbought

In June of 2013, when the cries of the “death of the bond bull market” were rampant, I made repeated calls that then was an ideal time to be a “buyer” of bonds.

“However, the recent spike in interest rates has certainly caught everyone’s attention and begs the question is whether the 30-year bond bull market has indeed seen its inevitable end. I do not think this is the case and, from a portfolio management perspective, I believe this is a prime opportunity to increase fixed income holdings in portfolios.”

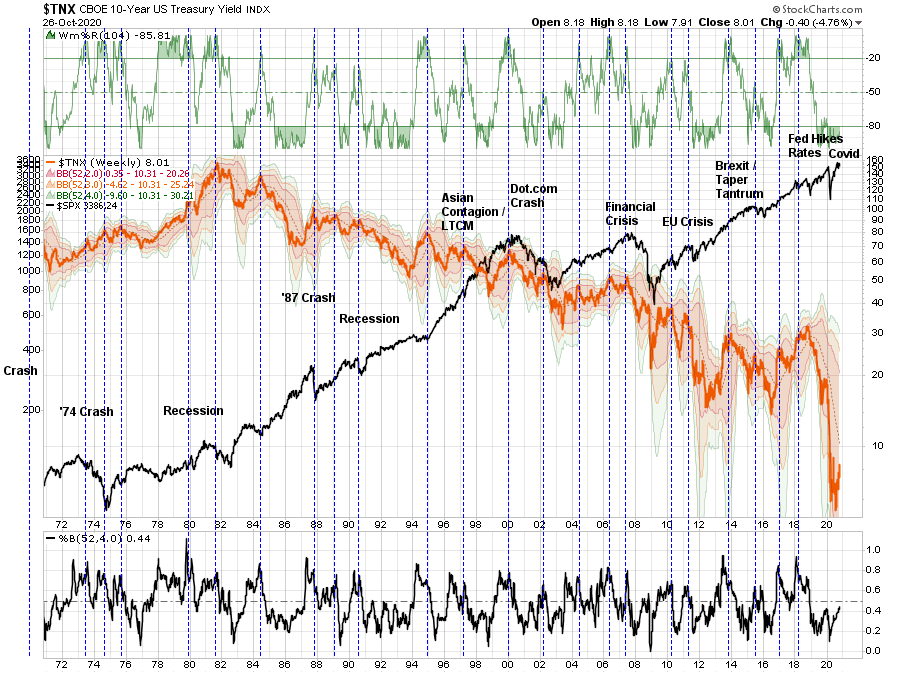

As shown in the chart below, that was the correct call and, despite repeated wrong calls by the mainstream analysts, bonds remained in an ongoing bullish trend.

Since interest rates are the inverse of bond prices, we can look at a long-term chart of rates to determine when bonds are overbought or oversold.

In 2019, rates began to slide slower as the realization that economic growth was weakening weighed on outlooks. As the yield curve began to invert, the Federal Reserve stepped in with expanded “repo” operations to shore up financial institutions.

Rates kept going lower.

In March of 2020, the economy was shut down due to the pandemic causing rates to plunge to record lows.

Huge Bond Buying Opportunity Coming

The plunge in rates and massive Fed liquidity caused stocks to surge to new highs despite an underlying recessionary economy.

Currently, the plunge in interest rates pushed bonds to an extreme “overbought” condition.

Such suggests the most likely target for rates in the near term could be as high as 2.0%. While an increase of 1.2% from current levels doesn’t sound like much, that increase would push bonds back to “oversold.” That move will provide the best opportunity to increase bond exposure in portfolios.

We can confirm the same using a very long-term chart (50-years) of 10-year interest rates overlaid with a 10-year moving average. As you can see, that moving average has provided formidable resistance and denoted every peak in rates going back to 1988.

Currently, with interest rates at the bottom of their long-term trend, the risk is that rates could indeed rise in the months ahead.

What could cause such an increase in rates?

- A massive debt-funded stimulus package that sends increased amounts of funds directly to households.

- More debt-funded infrastructure programs.

- If the government further increases deficit spending programs that fail to produce economic benefits such as universal basic incomes.

- An increase of economic activity as the economy reopens, and a post-recessionary recovery occurs.

- If there is a point where the Federal Reserve is unable or unwilling to monetize the entirety of the debt issuance

- A lack of demand by foreign buyers of U.S. debt over concerns on economic strength and financial stability due to debt-to-GDP ratios.

These lead to concerns over temporary inflationary spikes, which could drive interest rates back to the top of the long-term downtrend.

Where To Invest While We Wait For Bonds

While bond prices currently remain overbought, such a condition will likely not last very long. As shown below, markets and volatility have an inverse relationship with rates, hence the non-correlation for portfolios. The long-term log-chart of interest rates and the stock market tells the tale.

This analysis also suggests that the correction that started in March is likely not over as of yet in the longer term. If rates rise back toward the long-term downtrend, bond prices will come under pressure as the stock market corrects.

For investors, we can turn to our colleague Jeffrey Marcus of TPA Analytics. He recently analyzed the best places to invest during rising interest rates for our RIAPro Subscribers.

“The 4 best performing sectors are:

- Technology

- Consumer Discretionary

- Industrials

- Materials

The 4 worst performing sectors are:

- Utilities

- Telecomm

- REIT’s

- Staples

The 2 best performing broad categories are:

- Small-Cap Growth

Small-Cap

The 2 worst performing sectors are:

- Large-Cap Value

Large-Cap

Commodities: Crude and Copper are positive over half the time. Crude is the best performing commodity, historically.

Gold is the worst-performing commodity; it is only positive 14% of the time.

2 more focus items:

- TECH beat the S&P500 100% of the time

- Utilities underperformed the S&P500 100% of the time”

Not The End Of The Bond Bull

In the short term, we have cut our bond exposure and have begun to shift our allocations to protect portfolios for a rise in interest rates.

However, as rates rise within their technical downtrend, the media will be replete with headlines about the death of the 40-year “bond bull market.”

It won’t be.

- The stock market will defy higher rates initially until rates start to undermine the valuation story.

- A weaker economy will undermine the valuation story as higher interest rates impede consumption.

- The bullishly biased media will find themselves lost as to why stocks crashed and earnings fell.

While in the very short-term, the current overbought condition suggests we could see more downside pressure in bonds over the next few months. Such would not be surprising.

However, as we approach that point where the market begins to realize the impact of higher rates on economic growth and corporate profitability, bonds will again emerge as a haven for investors against market declines.

In an economy that is $75 Trillion in debt, requires $5.50 of debt per $1 of growth, and running a $3 Trillion deficit, rates can’t rise much.

Which is also why the Federal Reserve is now forever trapped at zero.

Related: Market Bulls Are “All-In” Again