Trending

Late last year, when we drafted our outlook for 2020 we gave it the title “The Era of Choice and Change.” We certainly had the change part right.

Whereas the year started on a “normal” trajectory, by March, the pandemic quickly put a halt to an immeasurable scope of in-person activities, requiring massive shifts in behavior across all socio-economic levels with impacts to the global economy both immediate and yet to be seen.

In late May, the tragic death of George Floyd brought racism and inequality into the global spotlight on another unprecedented scale with protests and demonstrations occurring not just locally, but in every major city nationwide and across the globe. Ted Mathas, CEO of our parent company, New York Life Insurance Company, spoke for all of us under the New York Life umbrella when he wrote recently that “the COVID-19 crisis is a human tragedy – one that has forced society to reassess almost all aspects of our daily lives. George Floyd’s senseless death is a societal tragedy – one that could not be more human. And it is one that requires all of us, in our professional and personal lives, to define who we are through words and deeds that reject racism and bias and repel discrimination and hatred.”

Through these dual lenses of an ongoing global health crisis and a profound social transformation, this is perhaps one of our most ambiguous outlooks to date. So rather than attempt to draw any significant conclusions as to how the markets will shape up over the next several months, we’re going to take a look at the notable developments from the first half of the year continuing before assessing the second half of 2020.

Another Type of March Madness – The Disconnect Between the Markets and the Economy

Ambiguity often drives volatility, so the dramatic market swings to the downside in mid to late March, disconcerting as they may have been, largely made sense as investors faced significant, unsettling ambiguity as to the potential extent of both the COVID-19 pandemic and the economic lockdowns that many states began to put into place. But while much of the same ambiguity remains, we have seen a remarkable decoupling of the markets from major economic data in recent months.

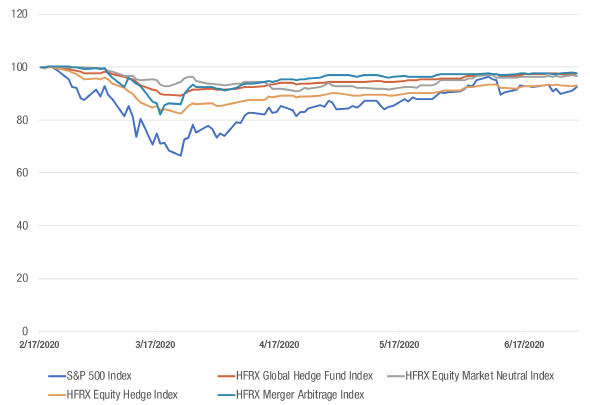

We’ve certainly had days where it appeared the market was about to race to the downside again, but as of June 30, 2020 the major indexes have all managed to hang onto most of the gains they’ve made since hitting Q1 lows:

Source: IndexIQ. High yield credit spreads are represented by the Barclays Capital U.S. Corporate High Yield Bond Index, Oil is represented by the Bloomberg WTI Crude Oil Subindex Total Return. Past performance is no guarantee of future results, which will vary. It is not possible to invest directly in an index.

Looking to Liquid Alts

The modest rebound may be cold comfort for investors who are wondering just how long this current environment may last, which is why we continue to point to liquid alternatives as a means of mitigating volatility, which seems more likely to return this year than not.

Volatile markets are a time for alternative strategies to shine. When taking a look at the major hedge fund indices, they participated in less downside in market volatility in the first half of the year.

Hedge Fund Indices vs. S&P 500 Index

Source: HFRI, IndexIQ as of 6/30/20. Past performance is not a guarantee of future results. It is not possible to invest directly in an index.

This, however, did not translate to outperformance across the board for traditional LP hedge fund managers. In fact, several leading active managers made headlines – in both extremes. Moore Capital saw a 17% gain through May 7th, however it is closed to new investors.1 On the other end of the spectrum, SkyBridge Capital saw a 22% plunge in March, followed by large redemptions.2

It’s difficult to pick winners as strategies are designed to perform differently in various market conditions. This dispersion can be unsettling to an investor who is required to commit large amounts of capital at a 2/20 fee structure over the course of several years. Liquid alt ETFs can help provide that exposure, while offering transparency, daily liquidity, all at a lower cost structure.

The Fed as ETF Portfolio Strategist

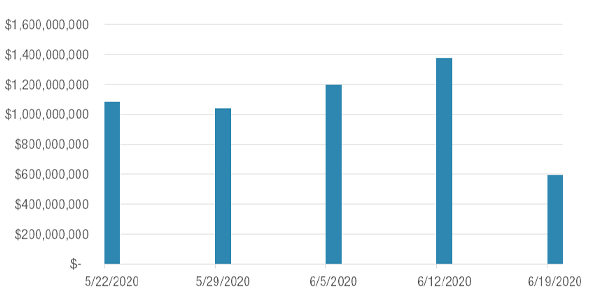

According to Barron’s, between May 12 and 19, the Fed bought $1.58B in investment grade and high yield ETFs with a June 1 market value of $1.31B.3

Fed ETF Purchases by Week

Source: Bloomberg, as of June 19, 2020.

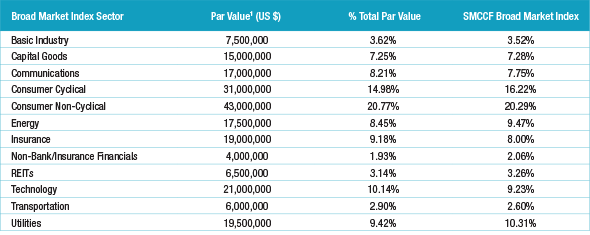

While we have long lived with an “active” Fed, few would have predicted at the start of this year that it would end June among the top shareholders of more than a dozen fixed income ETFs, bought as part of their efforts to inject liquidity into the markets. More recently, the Fed has become active in individual issues and is now acting as a passive bond portfolio manager themselves with the development of the Secondary Market Corporate Credit Facility (SMCCF).

Source: The Federal Reserve, as of 6/30/20. The SMCCF (Secondary Market Corporate Credit Facility) Broad Market Index is intended generally to track the composition of the broad, diversified universe of secondary market bonds that meet the criteria specified in the Term Sheet for Eligible Broad Market Index Bonds, subject to generally applicable issuer-level caps specified by the Term Sheet.

The Fed’s purchases seem to have gone according to plan thus far and have perhaps helped usher out the tired old trope that fixed income ETFs would be the root of the next crisis (they have, in this case, proven to be quite a valuable tool during the current one).

Consumer Price Index inflation had already been ticking up as 2019 came to a close and after the COVID-19 driven emergency rate cut in March the Fed may have very little ammunition left to fend off more inflationary factors. Here, we see opportunities for investors to help hedge against a reemergence of inflation with a variety of alternative strategies and also for investors to take a fresh look at some of their income strategies to see what other fixed income exposures may help mitigate the effect of inflation on a portfolio.

Where We Are Now

Yes, we had to bid goodbye to an 11-year bull market, but certainly some of the more dire outcomes being forecast in mid-March managed to be avoided. Perhaps no single future development will have as much of an impact on the markets and our social fabric as the identification and wide-scale deployment of a vaccine for COVID-19 – which isn’t likely until early next year. Until then, we are left in a pattern of virus growth and economic fallout with social distancing measures as the primary tool to manage the spread.

The Election is the Main Event in the Second Half

The current administration’s response to the crisis has met with much criticism. However, the markets flourished. This election cycle has already been unlike any other with traditional conventions and campaigning either cancelled or conducted virtually. There remains a great deal of time between now and Election Day, and the chances for additional unexpected events and controversies to flare up between now and then are significant, if 2020 so far is any indication. A contested result is but one outcome that could contribute to a new spike in volatility to end the year.

Conclusion

As members of an interconnected global society, we have quickly become accustomed to living through unprecedented times. We move forward with the hope that our global health and social justice issues will begin to see additional progress and resolution over the coming months and the markets and economy will take on more normal behaviors.

However, as this is an uncertain process, we do expect volatility to remain elevated through the end of the year. As markets typically do not care for ambiguity, we reiterate the importance of looking into strategies that offer risk mitigation and liquidity – with more ETFs available now than ever before to meet those needs for investors.

Continue to stay safe and stay well.

Related: Will the Coronavirus Change ESG Investing?

https://www.ft.com/content/c1ef73e0-4b49-4357-bc45-a05b7f0b865a