Trending

Written by: Elchin Mammadov, Xinxin Wang, and Drashti Shah | MSCI

Key findings

- Constituents of the MSCI ACWI Investable Market Index (IMI) with high scores on the climate-change theme outperformed globally across most sectors over the past 11 years.

- Over this period, leaders in the environmental-opportunities theme recorded higher market returns compared to laggards, although outperformance has sharply reversed since 2021.

- Despite this reversal, analysts’ consensus estimates suggest an improved outlook for environmental-opportunity leaders, with expected improvements in profitability from 2024 to 2027.

Should investors care about incorporating environmental data into equity analysis? Several academic studies have questioned whether sustainable investing and environmental metrics have been positively correlated with above-market returns.[1] Building on our previous research, we looked at the long-term relationship between MSCI ESG Ratings and market performance to help answer this question. We found that the listed companies worldwide that we rated most highly on their approach to financially material environmental risks and opportunities — the environmental pillar in our ESG Ratings — outperformed their lower-rated peers. On average, the highest-rated companies delivered 0.4% greater annualized total return than the lowest-rated since September 2013, after adjusting for region, industry and company size.[2]

A temporary pause or a significant shift in the climate movement?

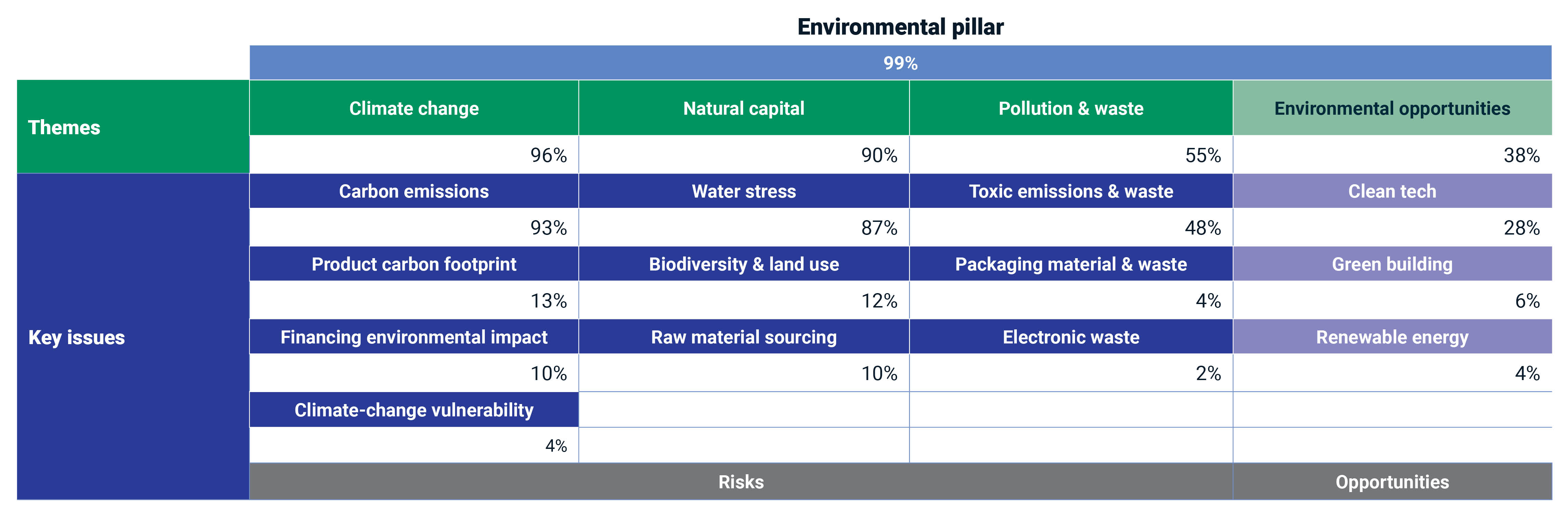

The MSCI ESG Ratings model groups key issues within the environmental pillar into three risk-focused themes (climate change, natural capital and pollution and waste) and one opportunity-focused theme.

Mapping and data coverage rates of financially material environmental risks and opportunities

Data as of July 2024. The exhibit shows the themes within the environmental pillar and the underlying environmental themes and key issues in the MSCI ESG Ratings model. Not all key issues are considered potentially financially material for all companies. The percentages represent average data-coverage rates for the constituents of the MSCI ACWI IMI from Sept. 30, 2013, to March 29, 2024. Data-coverage rates vary depending on the industry and specific environmental risks or opportunities that are applicable. For more information on the model, including how the relevant key issues are selected for each company, please refer to the MSCI ESG Ratings Methodology. Source: MSCI ESG Research

Among them, climate change delivered the strongest outperformance since September 2013 across both developed and emerging markets (EM) on a cumulative return basis. This outperformance could be largely driven by investors’ increasing focus on climate-related risks and opportunities, which has intensified in recent years. The widespread availability of carbon emissions data — relevant for 93% of companies in the MSCI ACWI IMI — has enabled more accurate assessment and alignment of portfolios with climate goals. Notably, the surge in investor interest and corresponding outperformance has been more pronounced since 2020, as global climate commitments and regulatory pressures have accelerated.

Cumulative returns for highest- vs. lowest-rated quintiles, equal weighted

Data from Sept. 30, 2013, to March 29, 2024. Our approach was similar to that used in MSCI ESG Ratings in Global Equity Markets: A Long-Term Performance Review. Quintiles are created every month based on environmental-pillar scores and for each of the four environmental-theme scores. The graph shows the cumulative difference between the top- and bottom-quintiles’ performance. In addition to climate-change and environmental-opportunities themes, the environmental pillar also incorporates the natural capital and pollution and waste themes. Source: MSCI ESG Research

Within key issues focused on environmental risk, companies that were leading on carbon emissions and product carbon footprint delivered the greatest annualized market outperformance (1.6% and 3.2%, respectively) versus laggards since 2013.[3] This may indicate the greater financial relevance of decarbonization compared to environmental risks related to water stress and biodiversity, as well as to toxic, packaging and electronic waste. Within the carbon-emissions key issue, companies that demonstrated leading capabilities to manage this risk had greater market outperformance than companies with the lowest exposure to carbon-emissions-related risks.

Although the leaders in the environmental-opportunities theme recorded higher market returns compared to laggards over the 11-year study period, that outperformance has sharply reversed since 2021, likely due to the headwinds in business activities related to clean tech, renewable energy and green buildings. These headwinds included higher interest rates and inflation as well as supply-chain issues, which hurt the profitability of capital-intensive green infrastructure projects. Rising bond yields, regulatory uncertainty and geopolitical tensions also negatively impacted valuations.

Superior returns across all sectors except energy

Our analysis showed that companies leading on the climate-change theme globally delivered between 2% and 9% annualized market outperformance compared to laggards over the 11 years ending March 2024. The only exception were companies in the energy sector. The outperformance was highest for the information-technology and financials sectors, followed by energy-intensive utilities, materials and industrials. Outperformance was the lowest for health-care companies.

Annualized returns of highest- vs. lowest-rated quintiles, equal weighted

Data from Sept. 30, 2013, to March 29, 2024. Quintiles are created every month based on adjusted climate-change theme scores for each sector. Analysis covers constituents of the MSCI ACWI IMI for which data was available, with data availability for each company dependent on the selection of risks and opportunities we identified as potentially financially material. The real-estate sector was excluded from the exhibit due to lack of data prior to 2016. Scores for the climate-change theme derive from the weighted average of underlying key-issue scores, as shown in the second exhibit. For more information, please refer to the MSCI ESG Ratings Methodology and the MSCI ESG Industry Materiality Map.

Energy was the only sector where laggards in the climate-change theme delivered greater returns. Beginning in 2021, several factors — geopolitical tensions, supply-chain disruptions, the pandemic-induced recovery in energy demand and production cuts by the Organization for Petroleum Exporting Countries (OPEC) — may have contributed to the strong performance by boosting energy prices and earnings for companies overrepresented within the laggards for the climate-change theme. In particular, these were oil and gas companies (notably listed companies from non-OPEC countries) and coal miners (particularly from China, where emissions rules are less onerous and where coal use for power and heat production got a boost as oil and gas fuel became more expensive).

A renewed momentum for environmental-opportunity leaders?

Since the beginning of 2021, improved earnings amid the energy crisis have helped the MSCI World Energy Sector Index outperform the MSCI Global Environment Index and the broader equity market (as measured by the MSCI ACWI IMI). Despite this, our analysis of consensus earnings estimates by equity analysts indicates potentially renewed momentum for environmental-opportunity leaders.[4]

The gap between the aggregate net income of environmental-opportunity leaders versus laggards is set to re-emerge by 2027 amid higher expected net income and EBITDA growth in 2024-27 for the top quintile, consensus shows. This expectation is underpinned by an anticipated relative (and, in many cases, also absolute) improvement in net-income margins of environmental-opportunities leaders versus laggards through 2027 compared to 2023. The shift appears most likely within the utilities, materials and real-estate sectors. Those leaders are also expected to deliver improved performance compared to laggards for price-to-earnings ratios between 2024 and 2027 due to stronger earnings rather than higher share-price valuations.

Median net income of highest- vs. lowest-rated quintiles, equal weighted

Data as of July 1, 2024. Quintiles are created based on scores for the environmental-opportunities theme as of March 29, 2024, with no monthly rebalance of the portfolio. We calculated median values of annual net income for top and bottom quintiles, equal weighted and converted to USD. We excluded companies if they had net-income values missing for any calendar year from 2018-27. After those exclusions, the total sample size was 276 constituents. Values for the 2018-23 calendar years are based on reported net income, and values for 2024-27 are based on the average of analyst consensus estimates for net income. Source: MSCI ESG Research analysis based on data from Refinitiv Eikon

A similarly improved outlook helped fuel strong outperformance in leaders within the environmental-opportunity theme in 2020. This time around it could be explained by an expected easing of headwinds related to high interest rates and inflation, permitting delays and supply-chain bottlenecks. Green policies, including the U.S. Inflation Reduction Act, EU Net-Zero Industry Act, Japan's Green Transformation package and the planned expansion of China’s emissions trading system and its energy-market reforms, could help companies further capitalize on environmental opportunities.

Risk-based strategies outperformed opportunity-focused ones so far

Many investors already choose to align their portfolios with climate goals to aid the assessment and mitigation of financial risks and to capitalize on opportunities related to environmental factors. The link we observed over the last 11 years between climate-change risk scores and equity-market outperformance supports incorporating carbon and footprint data into equity analysis. And while the case for incorporating environmental opportunities has so far been less obvious, that could change going forward.

- Ulrich Atz, Tracy Van Holt, Zongyuan Zoe Liu and Christopher Bruno, “Does sustainability generate better financial performance? Review, meta-analysis, and propositions,” Journal of Sustainable Finance and Investment 13, no. 1: 802-825; Giovanni Bruno, Mikheil Esakia and Felix Goltx, “‘Honey, I Shrunk the ESG Alpha’: Risk-Adjusting ESG Portfolio Returns,” Scientific Beta, April 2021; and Jitendra Aswani, Aneesh Raghunandan and Shiva Rajgopal, “Are Carbon Emissions Associated with Stock Returns?” Review of Finance 28, no. 1 (January 2024): 75-106.

- Our analysis period began in September 2013, based on the highest available data coverage, and ran through to March 2024. Our approach was similar to that used in “MSCI ESG Ratings in Global Equity Markets: A Long-Term Performance Review.” Quintiles are created every month based on environmental-pillar scores. We first regressed environmental scores based on market capitalization to eliminate any size bias. We then obtained the regression residuals and standardized them by region (North America, Europe, Asia Pacific and EM sub-indexes of the MSCI ACWI IMI) and Global Industry Classification Standard (GICS®) sector, finally, forming quintiles within each region and sector based on these standardized z-scores. GICS is the global industry classification standard jointly developed by MSCI and S&P Global Market Intelligence.

- This equates to 28% and 60% cumulative market outperformance from Sept. 30, 2013, to March 29, 2024, for carbon emissions and product carbon footprint, respectively.

- Our analysis is based on consensus estimates gathered by Refinitiv Eikon. See the note of the final exhibit for the detailed methodology.