Trending

Written by: Eubie Coe | New York Life Investments

From the layman investor to bulge bracket banks, no one can escape the buzz for cryptocurrencies. The COVID-19 pandemic has accelerated this interest in digital finance, and a potential new inflation hedge. Governments are getting increasingly involved as regulation catches up with technology. And for economists, the future of digital assets being used as a mainstream form of exchange is hotly debated.

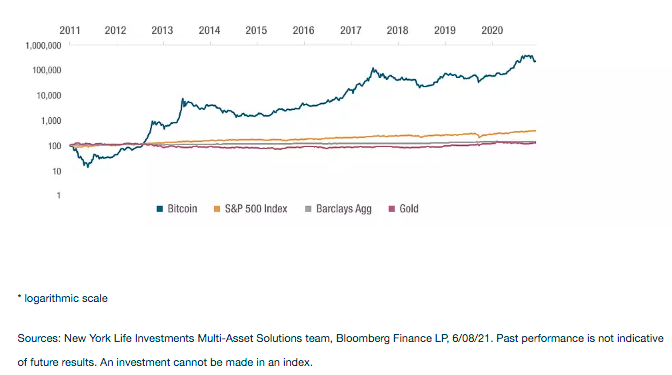

Perhaps most importantly, it’s difficult to ignore crypto’s performance relative to other asset classes since its inception. Throughout this piece, we use Bitcoin, currently the most common cryptocurrency, as a benchmark:

Figure 1: Historical Performance of Bitcoin vs. Other Asset Classes

Why are cryptocurrencies valuable?

A primary draw to cryptocurrencies is that they are decentralized, essentially bypassing the bureaucracy of central banks and governments controlling the currency supply. Elaborating on these benefits:

- Cryptocurrency enables near-instantaneous payments and eliminates concerns about defaults or cancellations

- No foreign exchange rates

- Bypass traditional payment systems, which rely on commercial banking

- Increased financial inclusion with censorship resistance, particularly for developing countries. Nobody can be denied access for any reason.

Risks to crypto uptake

We see potential for digital assets in the future of economic and financial market transactions, but their format has not yet stabilized. This presents some risks:

- Less regulation also means less user protection from economic crises, hacking, or other threats

- Governments are discussing how to regulate cryptocurrency, which may impact current operations

- Central bank and private alternatives to cryptocurrency, such as central bank digital currencies (CBDCs) and Stable coins are also in development. While these alternatives may use different technologies and protocol than cryptocurrency, they may reduce the relative benefit of cryptocurrency in some areas (i.e. ease of digital transaction).

- Environmental impact: A single Bitcoin transaction consumes more than 4x the energy as 100,000 Visa transactions.1 While there are reasonable counterarguments to this structure (i.e. improving energy efficiency; infrastructure required to power credit card transactions), it could present a risk for uptake.

Is cryptocurrency money?

The history of money is complex, but there are traditionally three functions required to meet the definition: it must serve as a medium of exchange, a store of value, and a unit of account. Fiat money (e.g. the U.S. Dollar) fulfills all those requirements.

There is much debate about how cryptocurrencies fit into these three requirements. We’ll use Bitcoin (BTC), currently the most common cryptocurrency, as a benchmark:

- Currently, BTC cannot act as a unit of account. Anything priced in BTC today is also priced in USD – if BTC were to be a unit of account, the number of coins must be independent of the dollar price of BTC.

- BTC is also not a reliable store of value. Now, BTC price is based on speculation that the cryptocurrency might become mainstream money in the future.

- Finally, because there is mass speculation around BTC and much volatility in its performance, it is not yet a mainstream medium of exchange.

If not money, then what is crypto worth?

Underlying “value” is always difficult to determine and often subjective, but if cryptocurrency doesn’t yet check the boxes as “money,” then investors may instead be focused on its role in the future of technology and process.

Remember, crypto isn’t just a currency—it is a technology, a network, and a means of transaction. As such, we have witnessed the rapid emergence of development platforms and enabling technologies. These underlying technological benefits have inspired an explosion of innovation, an entire ecosystem of altcoins, and new business models. The investment space could be impacted not just by cryptocurrency, but also by these new platforms for investment strategies and customer acquisition.

How to invest

There are three things investors should consider when implementing crypto into a portfolio.

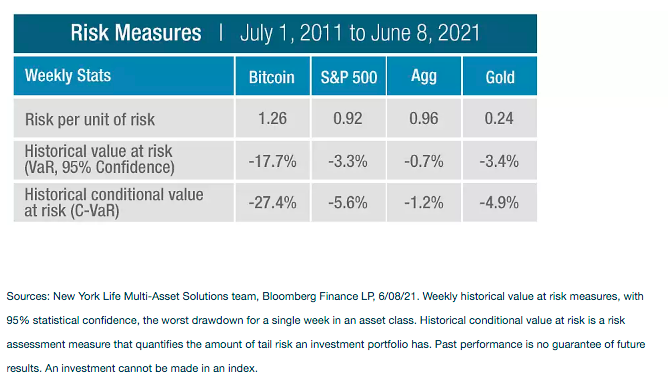

1. Understand the risk profile of the asset class.

When thinking about investor outcomes, it is important to consider the risk potential of any asset class. Investors have several options, but across all of them Bitcoin showed the most potential risk over the 10 years since its inception.

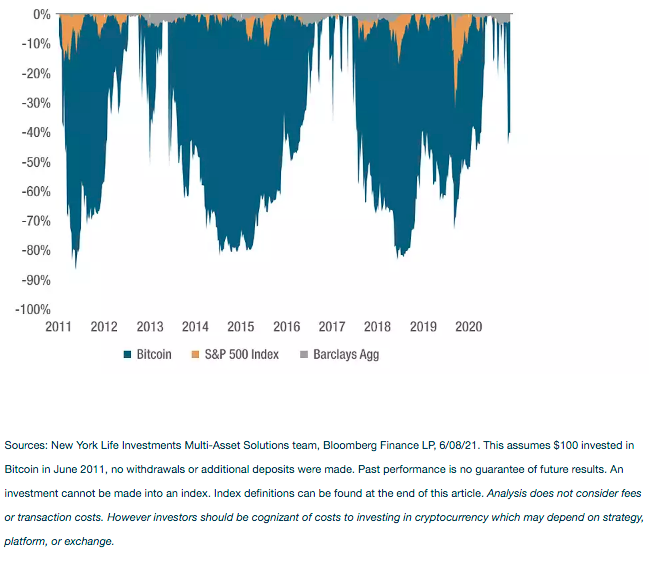

Figure 2 indicates a cyclical drawdown of approximately -80% every 3 years—a significant risk that Bitcoin investors should be wary of. For many investors, this level of volatility is unsuitable. For those with higher risk tolerance, often only a small allocation is appropriate.

Figure 2: Portfolio historical drawdown: Bitcoin, stocks, and bonds

$100 invested 10 years ago

2. Identify your use case for the asset class.

There are two schools of thought when it comes to investing in cryptocurrency. The first is comprised of those who believe in the technological case for a viable mainstream cryptocurrency and disrupting traditional finance, discussed above. The second is those who are interested in diversifying their investments with a high-volatility asset class. While our broad recommendations for allocation are similar for both groups (see below), the distinction may impact the size or specificity of allocation.

3. Consider where it fits in a portfolio.

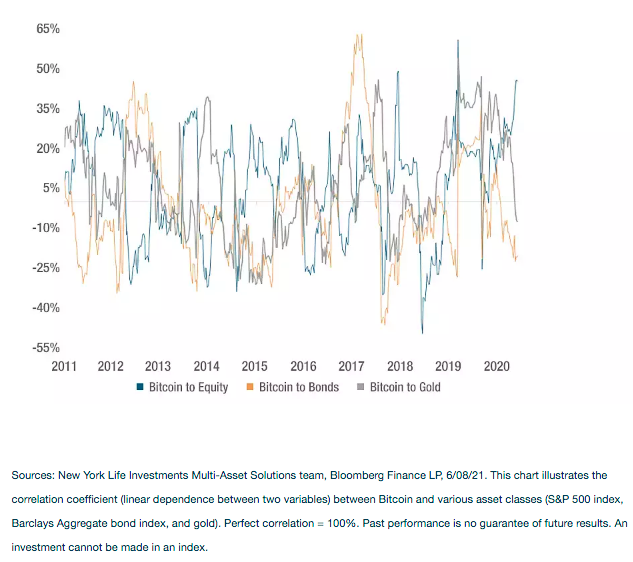

Because cryptocurrency is often referred to as a potential inflation hedge, it can be tempting to allocate to crypto from the core equity or fixed-income portion of a portfolio, as some investors do with gold. This is not our recommended approach. In our view, Bitcoin is inherently different than gold as its intrinsic value is ill-defined, and subsequently the price is much more volatile. Figure 3 below illustrates non-stationarity, as well as the lack of consistent correlation between Bitcoin’s performance in relation to equities, bonds, and gold.

Figure 3: Bitcoin’s correlation to other asset classes

Rolling 6-month average

Instead, cryptocurrencies should be considered as an alternative asset class. A diversified alternative portfolio can vary in its composition: private credit, private equity, real assets, venture capital, and hedged strategies. Portfolios that include alternative asset classes can vary widely depending on investor goals and risk tolerance, and will make up anywhere from 5% - 30% of assets. However, the similarities are in client type: accredited investors (high net worth individuals), investors seeking growth (risk takers), and investors who are willing to lock their money up for a significant period of time (5-15 years).

Conclusion

Ultimately, how optimistic or skeptical one should feel about Bitcoin or cryptocurrencies in general is highly subjective. And as soon as you feel like you have achieved a good understanding of the landscape, a new coin or a technicality comes into play. However, with all the information provided above, the takeaways are:

1. Stay open minded about innovations in digital and decentralized finance as they can improve market efficiency.

2. Learn to separate hype from reality. What are extreme runups based on? Do you agree with the fundamental assumptions made? Once you’ve answered these questions, let that inform your investing.

Related: How to Read Cryptocurrency Charts

1. Source: BCA Research, Bitcoin: A Solution in Search of a Problem, 2/26/21.