Trending

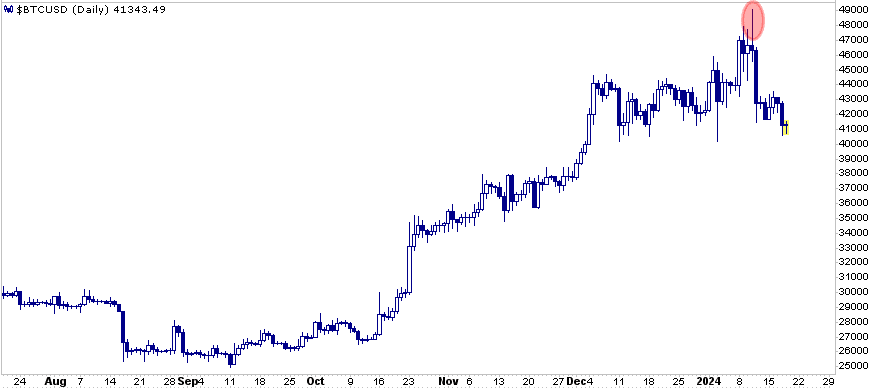

The price of Bitcoin rose over 10% in the first two weeks of 2024, peaking on January 11th. Driving the performance were rumors that the SEC would finally approve Bitcoin ETFs. On January 10th, they approved 11 Bitcoin ETFs. Spot Bitcoin backs these ETFs. Such means that each new share of the ETF is directly backed by bitcoin. Bitcoin rose as the market was opening to many more potential buyers. However, the price has given up all of its 2024 gains since the announcement. This is yet another example of what Wall Street calls “buy the rumor and sell the fact.”

The big question for Bitcoin investors is how the new ETFs will impact the price of Bitcoin. The answer may not be as bullish as it may appear. Certainly, more people will now have easy access to purchase bitcoin, which should bolster the price. However, more people can now short Bitcoin or buy put options via the ETFs. There is another consideration. True Bitcoin believers, not traders, like that it is decentralized and the supply will never be more than 21 million bitcoins. As a result of SEC approval, Bitcoin is now a de facto part of the financial regulatory system and will be more scrutinized by the government. Further, the ability to short Bitcoin makes the supply seemingly unlimited. Might some Bitcoin investors shift to another cryptocurrency? The SEC ruling may not be as rosy for Bitcoin as some believe.

What To Watch

Earnings

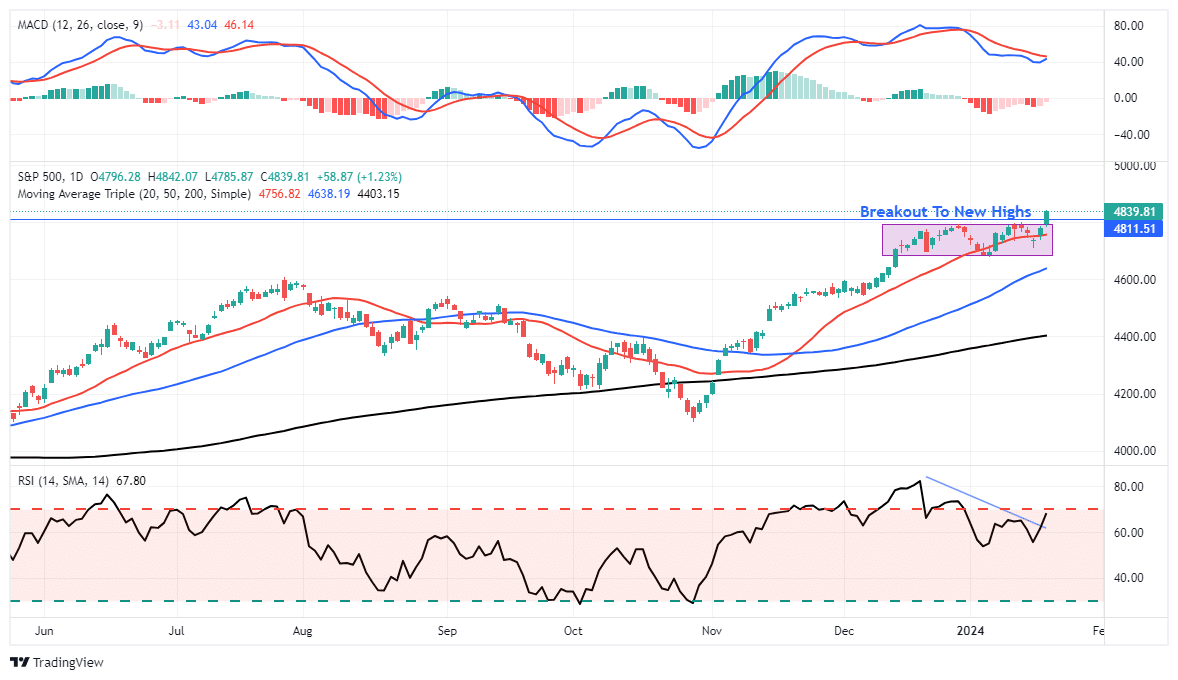

Market Trading Update

In Friday’s Commentary, we discussed the comments from Fed member Raphael Bostic. In that note, we stated:

“The market is likely getting close to the end of this ongoing consolidation, and a breakout above the recent highs will confirm the market’s next move is higher. Continue to manage risk and wait for the breakout to add exposure.”

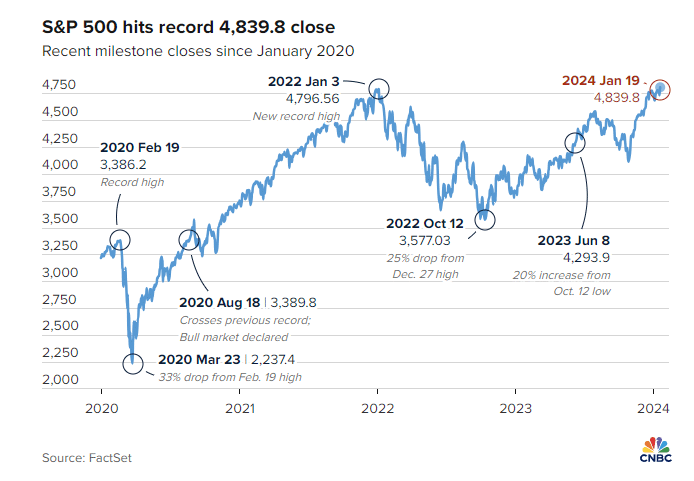

That consolidation likely ended on Friday, with the market breaking out of that consolidation to set a new all-time high for the S&P 500. As is always the case, the media was quick to jump on the headline as well:

“Friday’s milestone confirms that the stock market is officially in a bull market that began in October 2022, and not just a bounce within a bear market. The S&P 500 is up more than 35% since that low.” – CNBC

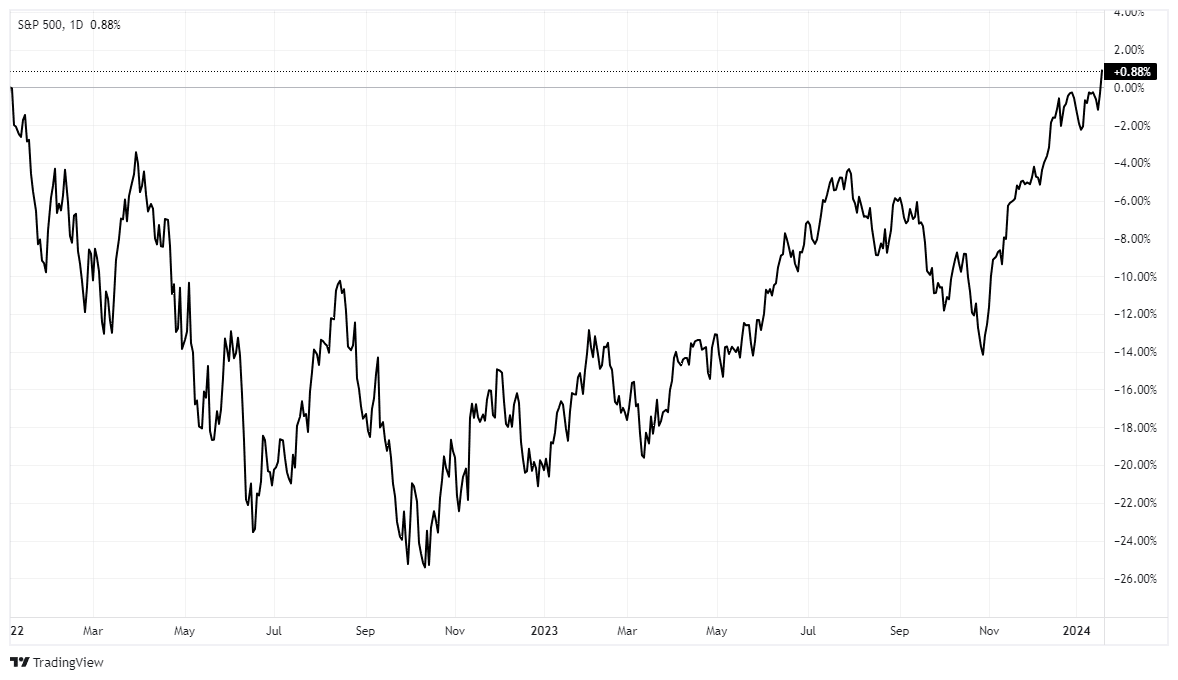

Of course, while the rally of 35% from last October’s lows was fantastic, the media never told you to sell in the first place. Therefore, for most, the 35% rally was used to get back to even. Notably, the “buy and hold” crowd has now achieved a positive return after 24 months of just 0.88%.

Nonetheless, the breakout to new highs is encouraging and suggests the two-year market correction process is now behind us. The action is clearly bullish from a technical perspective, but the more overbought conditions have failed to correct meaningfully. Such suggests that further upside from current levels may be somewhat limited, and another corrective phase is likely sooner rather than later.

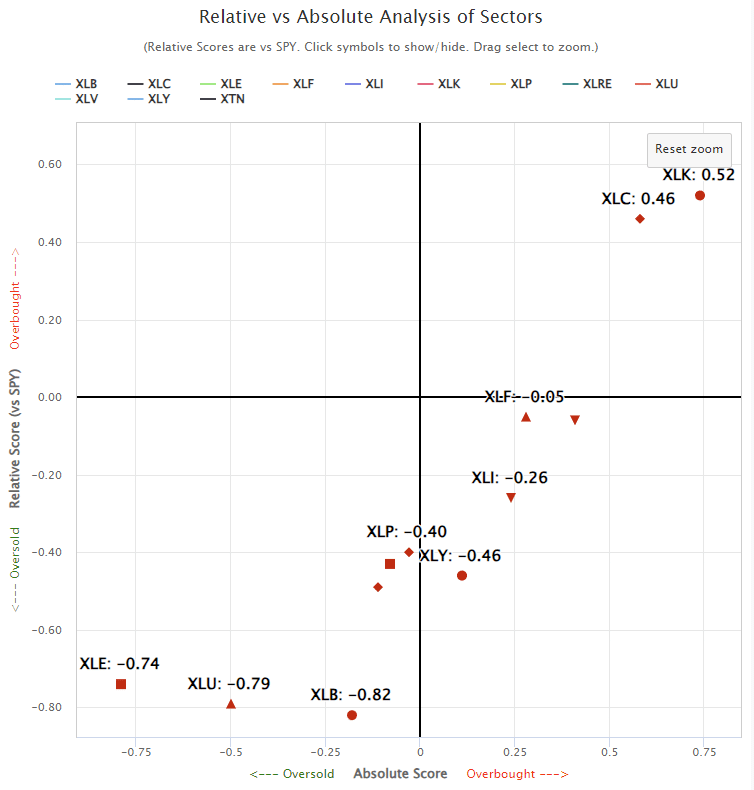

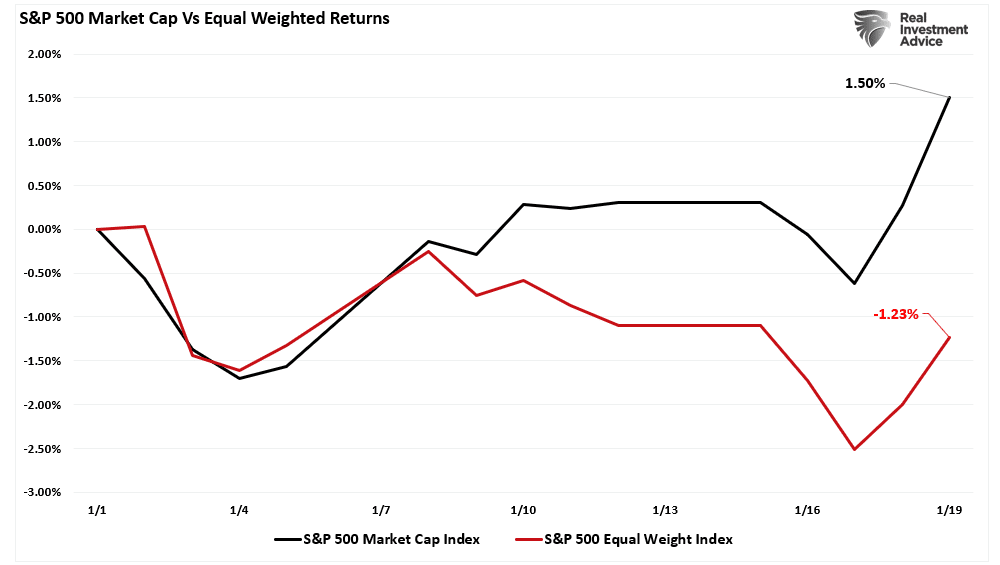

While there seems to be little concern in the market currently, particularly given the low levels of volatility, the rally has once again become very narrow, with the A.I. stocks and the “Magnificent 7” leading the charge. The Simplevisor Relative Rotation Analysis shows this issue more clearly.

And, as in 2023, we see the performance gap between the market capitalization and equal-weighted indices.

Given that the big Mega-capitalization stocks are a place of safety where major asset managers can place large amounts of capital, and the bulk of expected earnings growth will come from those companies, it is not surprising we are seeing the divergence again. Such is also unsurprising given the increased expectations for a significant easing of monetary policy this year as the Fed not only cuts rates but readies the markets for the end of QT.

The bullish backdrop remains intact. We would like to see confirmation of the breakout to new highs before we increase equity exposure further. We will likely have that answer by the end of the week.

The Week Ahead

GDP on Thursday and PCE Prices on Friday will headline this week. GDP is expected to grow by 2.2% in the fourth quarter. Such is solid but well off the 4.9% pace of the previous quarter. Core PCE is expected to rise by 0.1%. Forecasts for PCE declined after the PPI number last week.

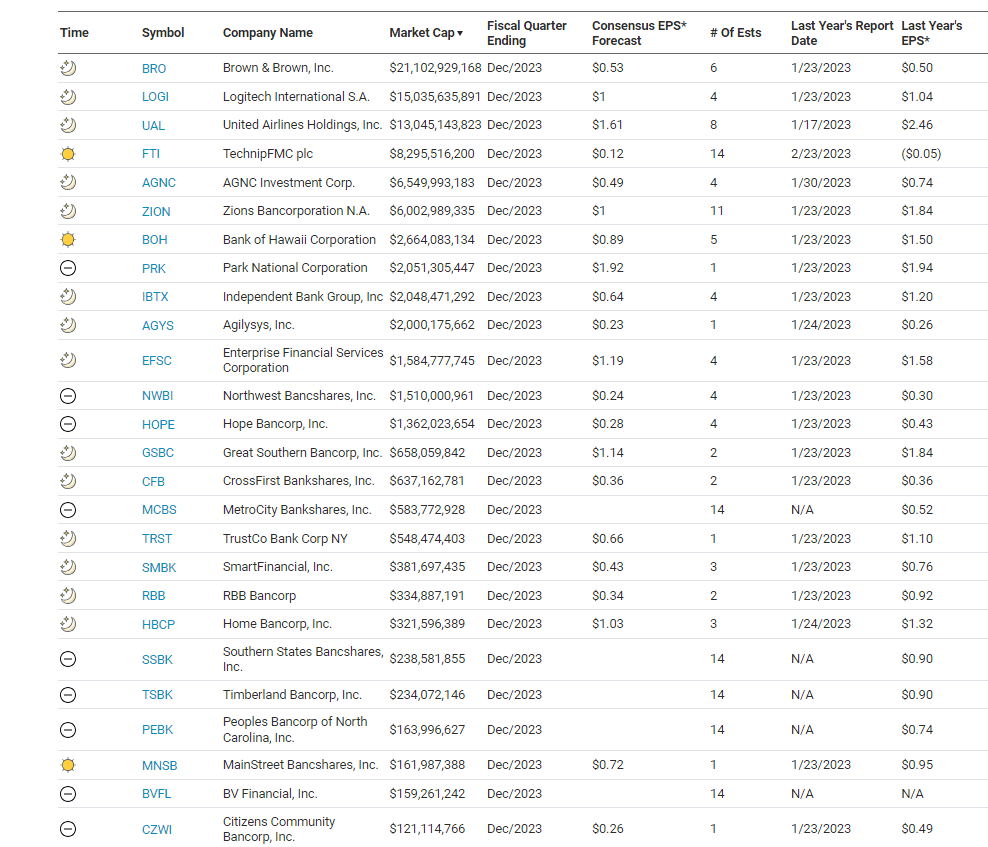

Earnings will loom large this week, as we share in the calendar below from The Transcript. However, most of the large mega-cap companies, which will most affect the market, will report next week.

The Fed will go into a media blackout as they approach next week’s FOMC meeting. Hence, we should expect little guidance as to what they may say at the January 31 meeting.

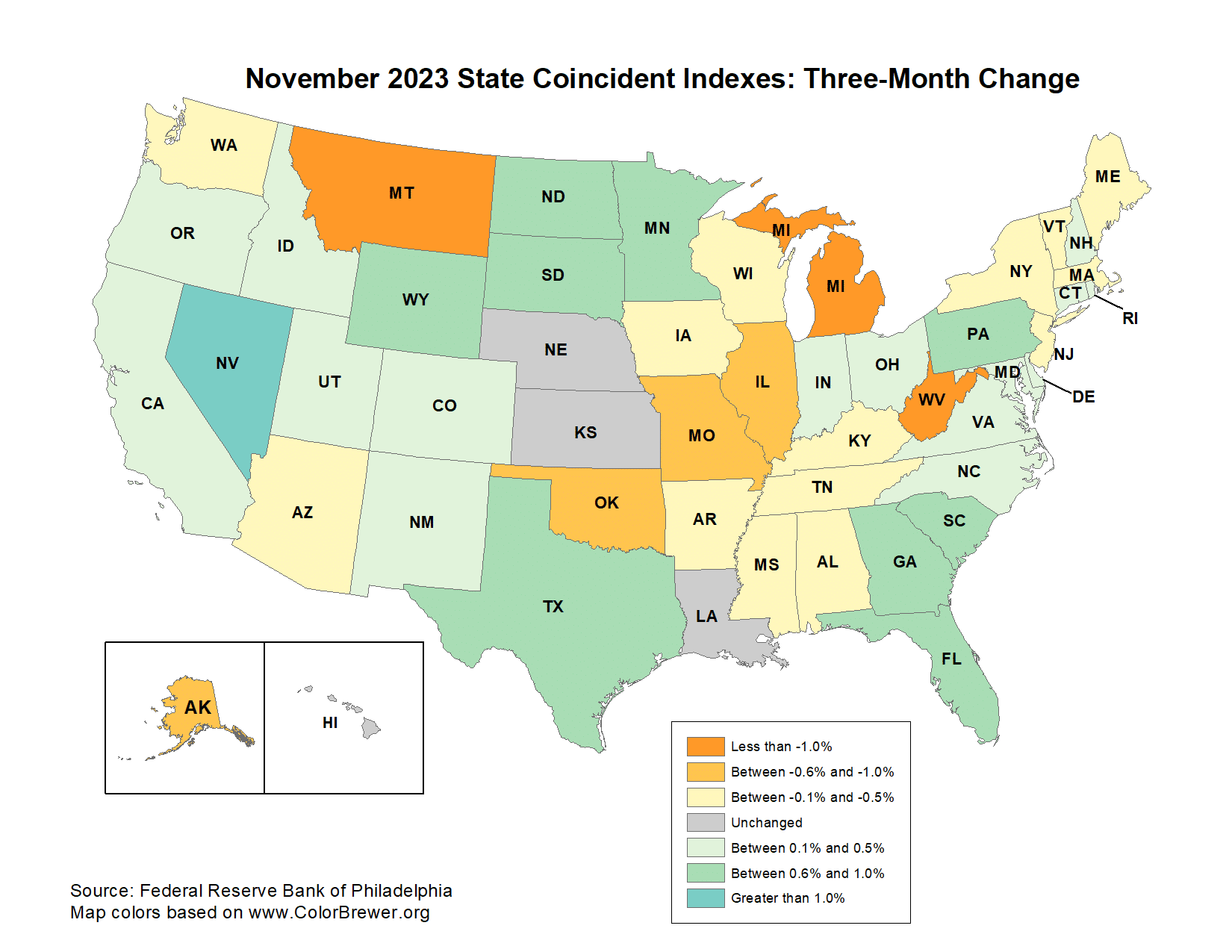

The Philadelphia Fed Sees Economic Contraction In 21 States

The Philadelphia Fed publishes monthly State Coincident Indexes summarizing the current economic conditions by state. The most recent report shows that 21 of the 50 states are seeing economic contraction based on their calculations, as shown below. As you know, each state has different levels of economic activity. Therefore, what matters from a national perspective is the economic activity in the most significant states ranked by GDP. In order, California, Texas, New York, Florida, and Illinois have the biggest GDPs. Three of them, California, Texas, and Florida, have positive economic growth, per the Philadelphia Fed. New York and Illinois are contracting.

The coincident indexes combine four state-level indicators to summarize current economic conditions in a single statistic. The four state-level variables in each coincident index are nonfarm payroll employment, average hours worked in manufacturing by production workers, the unemployment rate, and wage and salary disbursements deflated by the consumer price index (U.S. city average). The trend for each state’s index is set to the trend of its gross domestic product (GDP), so long-term growth in the state’s index matches long-term growth in its GDP.

While the national economy remains robust, there are certainly pockets of weakness. Like for instance, the manufacturing sector has been in a recession for over a year. Further, per the latest Fed Beige Book, measuring economic activity by Fed region, 7 of the 12 Fed banks reported economies in their jurisdiction are either in contraction or stagnation. The other five are barely expanding.

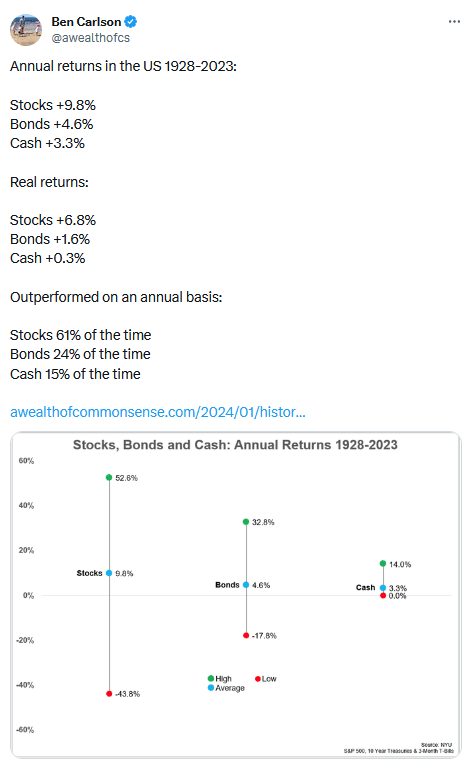

Tweet of the Day

“Want to have better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Related: Deficit Spending Keeping the Economy Out of Recession