Trending

Written by: PacLife | Pacific Life

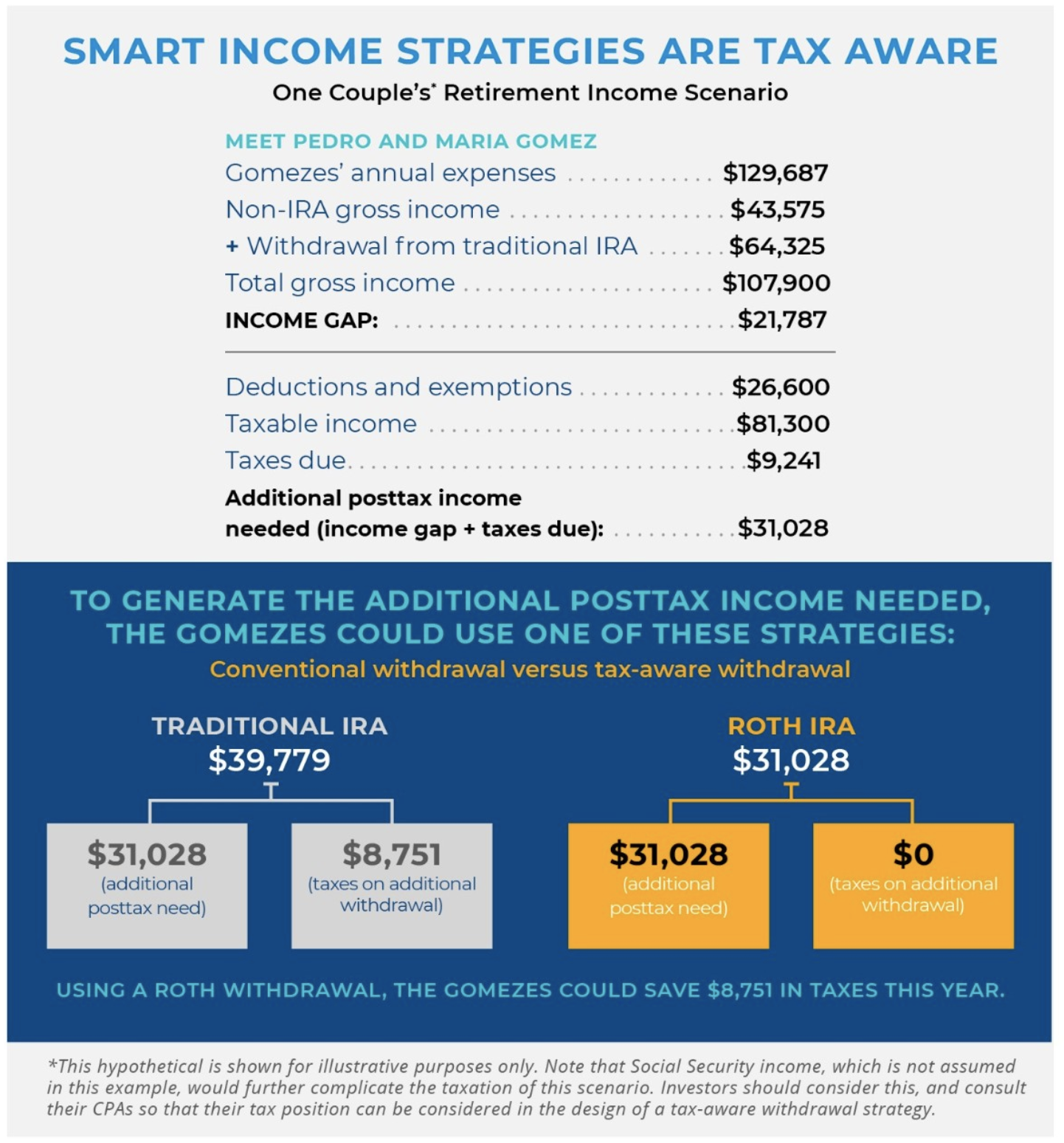

Living the retirement you envision begins with investing and accumulating money over the course of many years. But it doesn’t end there. To truly make the most of your retirement, you’ll need to develop a strategy for drawing down your investments. That will involve looking at all of your accounts and figuring out a tax-efficient way to tap into them in the right order over time. By making a plan for which accounts you should access first, second and so on, you’ll have a better sense of what you can spend and how long you can expect your savings to last.

The first part of developing an income strategy is determining how much money you’ll need for the retirement lifestyle you envision. Work with your financial professional to estimate your retirement spending. The figures could be higher than you imagine: In fact, 37 percent of current retirees reported higher expenses than they’d expected, according to the collaborative work of Greenwald & Associates and the Employee Benefit Research Institute’s 2018 Retirement Confidence Survey.1 In particular, health-care costs were often higher than retirees had anticipated. Be sure to reserve sufficient funds for unexpected expenses as you make your calculations.

Once you’ve estimated your required income, the next step is to determine how to access it. Some income sources are guaranteed, while others are affected by market fluctuations and other external factors. Understanding how these different income sources work will help you decide the right mix for you.

Guaranteed income

Many people want a certain amount of their retirement income to be dependable and predictable. Some pension plans offer defined benefits that guarantee monthly income for life. Social Security is another source of guaranteed income, although the amount you receive in Social Security each month depends on your earning history and marital status, as well as when you begin taking the benefit. Use the Social Security Administration’s retirement estimator to get an idea of how much to expect.

Annuities offer another way to put a floor under your retirement income, providing an income stream in exchange for an initial investment. Immediate annuities begin issuing payments soon after you make your investment, while deferred annuities are invested for a period of time before you start taking withdrawals.

You can also choose between fixed (-rate) and variable annuities. Fixed annuities earn a guaranteed interest rate over time, while variable annuities are tied to the performance of an investment portfolio. Fixed annuities provide more certainty, but variable annuities offer more growth opportunity. Both provide monthly income for life and protection for your loved ones through a death benefit.

Annuities do have some limitations. For example, because they’re designed for retirement savings, you may be charged penalties if you take out your money early. For example, if you take withdrawals before age 59½, you may pay a 10 percent federal tax in addition to ordinary income taxes. Consult your tax professional regarding your unique situation.

Nonguaranteed income sources

Any source of income affected by forces outside of your control, such as inflation or the changing stock market, is considered nonguaranteed. Even low-risk investments like bonds come with some uncertainty, since their prices can be affected by changing interest rates and other factors. Meanwhile, higher-risk investments like stocks are subject to more dramatic fluctuations. The amount you can withdraw from your retirement portfolio depends to some degree on the performance of the investment products you own.

That said, you can make some assumptions about your ability to draw income from your retirement savings. Many experts recommend a 3 to 4 percent annual withdrawal strategy as a way to sustain your savings over your lifetime, potentially adjusting the amount based on market performance. For instance, in the year following a down market, you might withdraw only 3 percent of your portfolio’s assets, whereas 4 percent might make sense under better market conditions. Of course, there is no guarantee that this strategy will meet your income needs in full.

Refining your strategy

The most successful retirement income plans involve ensuring that you have enough money each year to cover your expenses comfortably while allowing other investments to grow. The combination of strategies and products that is right for you depends on how much you’ve saved, your life expectancy and your desired retirement lifestyle. Your financial professional can help you develop a sustainable income strategy that makes sense for your goals and situation.