Trending

Written by: Arkadiusz Sieron, PhD

The US economy generated almost 530,000 jobs in July. That’s good for monetary hawks but bad for gold bulls.

Strong Employment Report Strengthens Fed’s Hawks

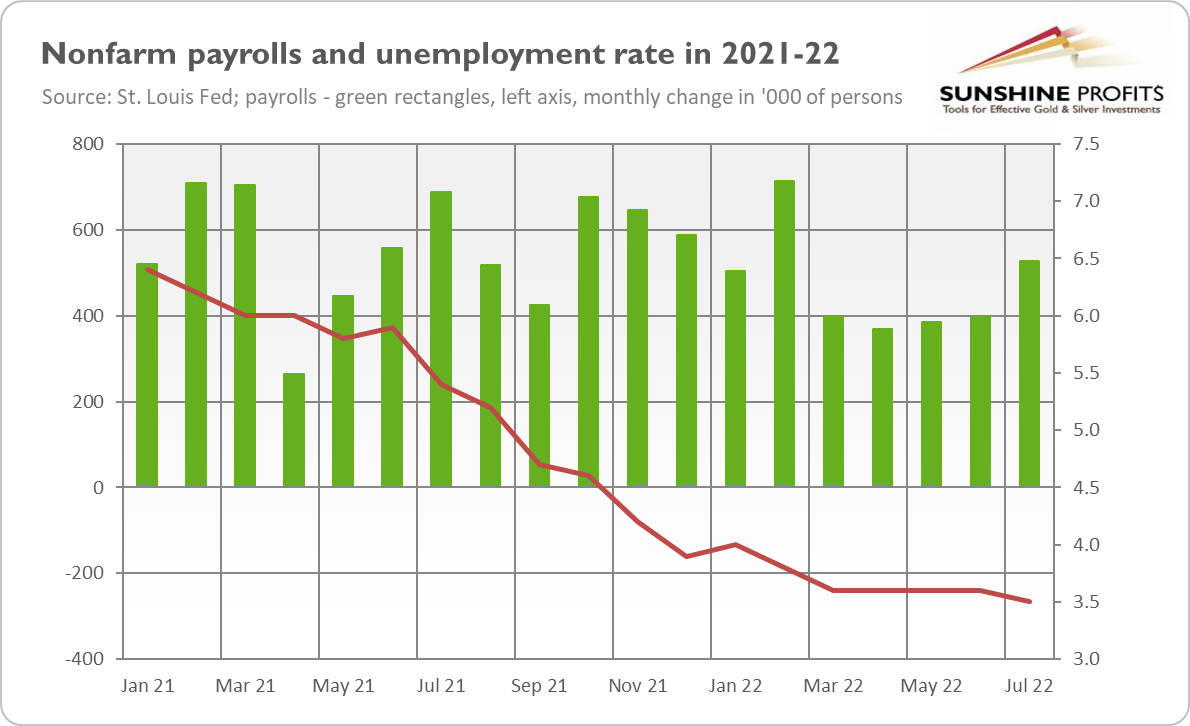

A positive economic surprise! The US labor market added 528,000 jobs last month. As the chart below shows, the number is above June’s figure (+398,000) and much above the market expectations (MarketWatch’s analysts forecasted only 258,000 added jobs). The July number was the highest since February and well above the average monthly gain over the prior 4 months. Importantly, job growth was widespread, led by gains in leisure and hospitality, professional and business services, and health care. Additionally, revised employment in May and June combined was 28,000 higher than previously reported.

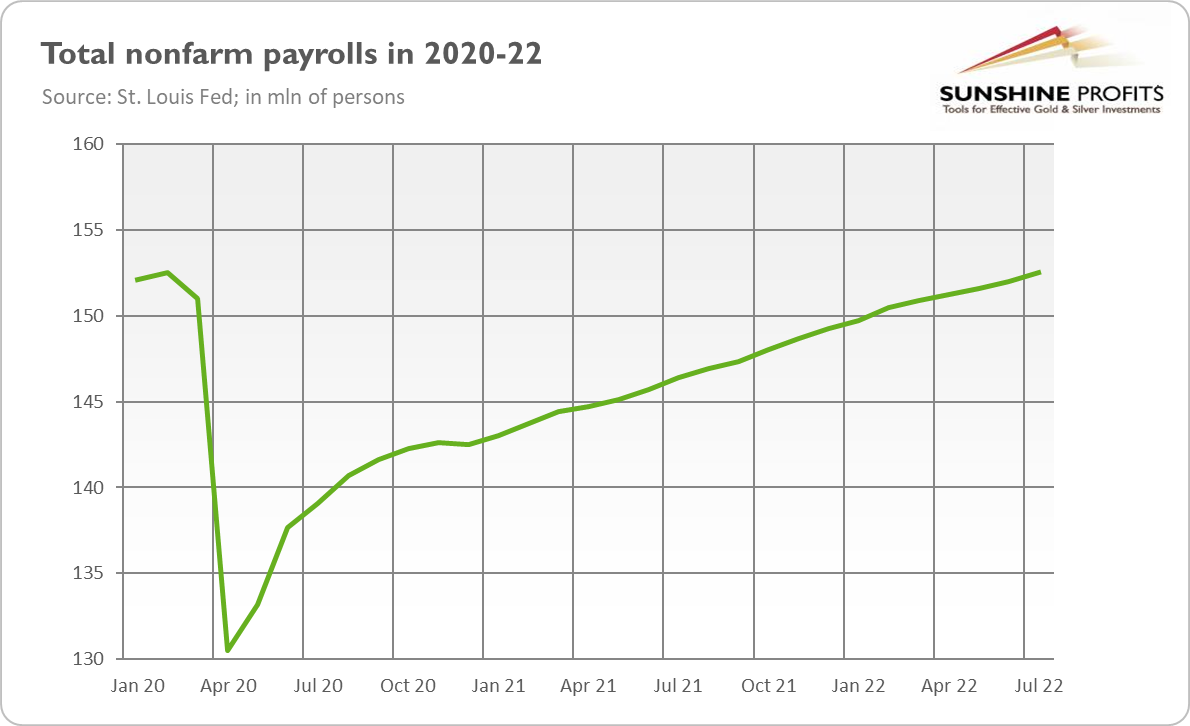

Hence, the latest nonfarm payrolls strengthen the optimistic view of the US economy and soften recessionary worries. After all, the narrative is that the economy can’t be in a recession as long as the labor market remains strong. Importantly, total nonfarm payrolls have returned to the pre-pandemic levels of 152,5 million people, as the chart below shows.

What’s more, strong job creation boosted employment and the unemployment rate decreased slightly from 3.6% in June to 3.5% in July, as the chart above shows. It strengthens the narrative about the healthy state of the US economy. However, the drop in the unemployment rate was accompanied by a decrease in the labor force participation rate from 62.2% to 62.1%.

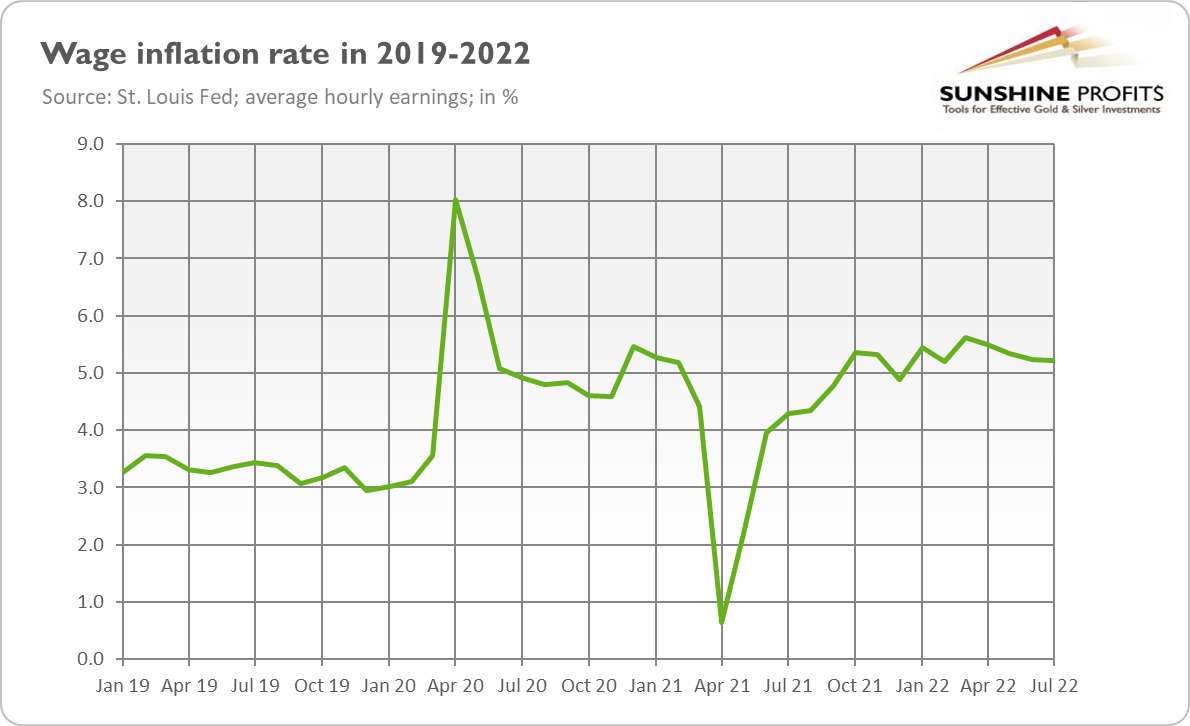

Regarding other labor market indicators, average hourly earnings have increased by 5.2% over the past 12 months. It means that wage inflation remains elevated, which could add to the pressure for the Fed to continue its hawkish stance.

Strong Employment Report Strengthens Fed’s Hawks

The July employment report will further strengthen the already hawkish stance of the US central bank. The surprisingly strong payrolls will strengthen the Fed’s confidence in the American economy and reduce worries about a hard landing. Hence, with strong job creation (and wage growth), the Fed could deliver a larger interest rate hike in September. This is at least what traders have started to expect. The market odds for a 75-basis point move surged from 34% to more than 68%, according to the CME FedWatch Tool. As a result of these expectations, bond yields and the U.S. dollar rose, while the stock market declined following the release of the Employment Report. In other words, the Fed is still on target to raise rates, and the hopes for the pivot early next year could be premature.

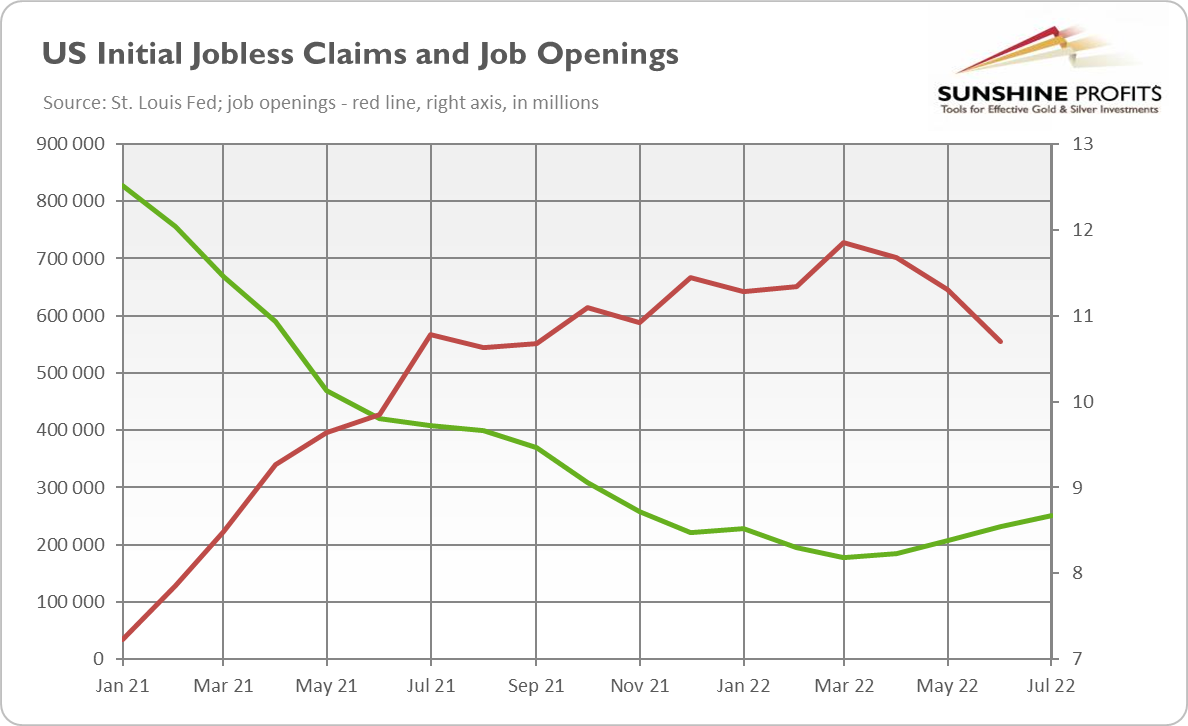

However, I would like to point out two things. One is that the unemployment rate, and the labor market in general, are lagging indicators. So, it’s logically unjustified to conclude that a recession is not likely because the labor market remains strong. The second point is that not all labor market indicators indicate strength. For example, initial claims for unemployment insurance totaled 260,000 last week, near the highest level since November, as you can see in the chart below (it shows monthly averages, but the trend is the same).

Meanwhile, job openings plunged from 11.3 to 10.7 million in June, the lowest level since September 2021, as the chart above shows. Thus, I would say that the labor market has started to slow down, but it’s not yet seen in the nonfarm payrolls or the unemployment rate.

Implications for Gold

What does it all mean for the gold market? Well, gold did the same as equities after the release of the July payrolls – it fell that day. The price of the yellow metal declined from about $1,790 to about $1,770. It’s because strong job creation reduces recessionary fears and the likelihood of the Fed’s monetary policy pivot. No doubt, the latest employment reports give the upper hand to the Fed, so if nothing spectacularly bad occurs in the upcoming weeks, the US central bank could hike interest rates by 75 basis points in September rather than 50 basis points. Such a recalibration of market expectations is clearly negative for gold prices. However, there is still plenty of time before the next FOMC meeting and a lot could happen in the meantime. Stay tuned!

Related: The Yield Curve Inverts. Now It’s Time for Gold to Turn Back