Trending

This week’s Commentary discussed the coming halving of Bitcoin and its pros and cons for Bitcoin miners. While mining for gold is an entirely different endeavor, a couple of readers asked us to opine on the differences between holding gold and gold miners. One common thread between gold and Bitcoin miners is that the easiest, cheapest gold or Bitcoin is mined first. Each additional ounce of gold or bitcoin becomes more expensive to mine.

From a gold miners perspective, their labor and equipment expenses have risen considerably with inflation. Further, as it becomes more difficult to find gold, they must mine in more remote places. That comes with higher costs and less yield. While the added expenses of finding new gold are a slow upward trend, the inflation surge is hitting miners now. Accordingly, even though gold prices are up significantly, mining costs have also risen appreciably. If you want to own gold, we think buying gold bullion or an ETF is the best way to express such an investment. Suppose you want leverage on the price of gold. Further, you are willing to be subject to the costs of running a mining operation, including bad management decisions. In that case, gold miners may be a suitable investment. As with any stock, there are efficient and non-efficient gold miners. Do your due diligence.

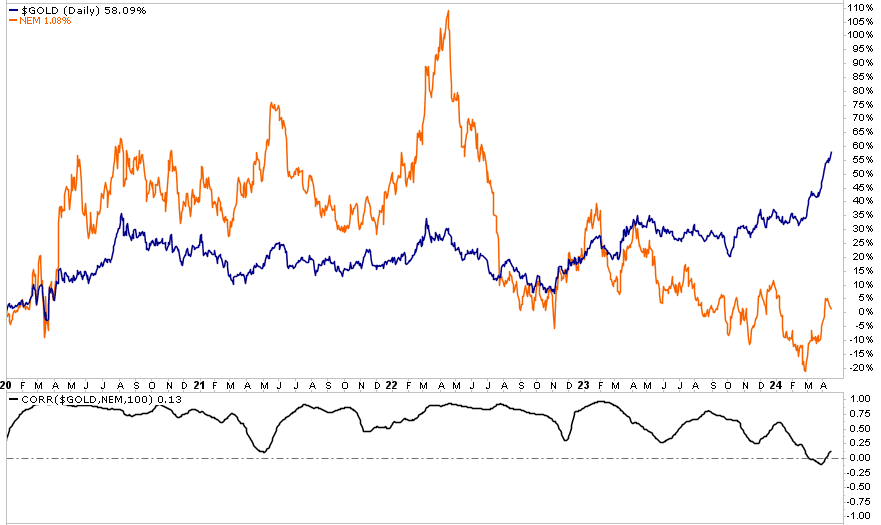

The graph below shows that since 2020, gold has risen by 60%, while Newmont (NEM), the largest holding of the popular GDX gold mining ETF, is flat. The lower graph shows the correlation between gold and NEM has been close to zero for the last two months.

What To Watch

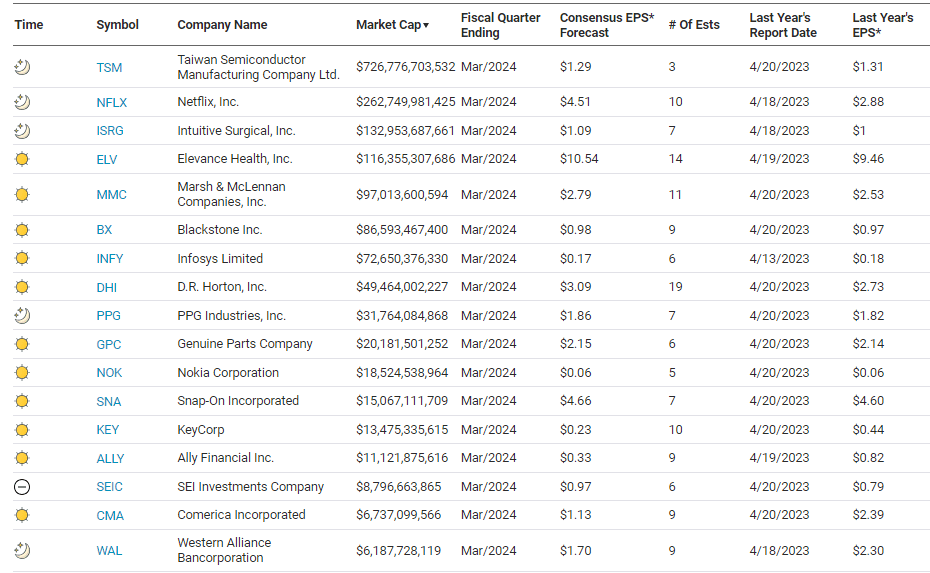

Earnings

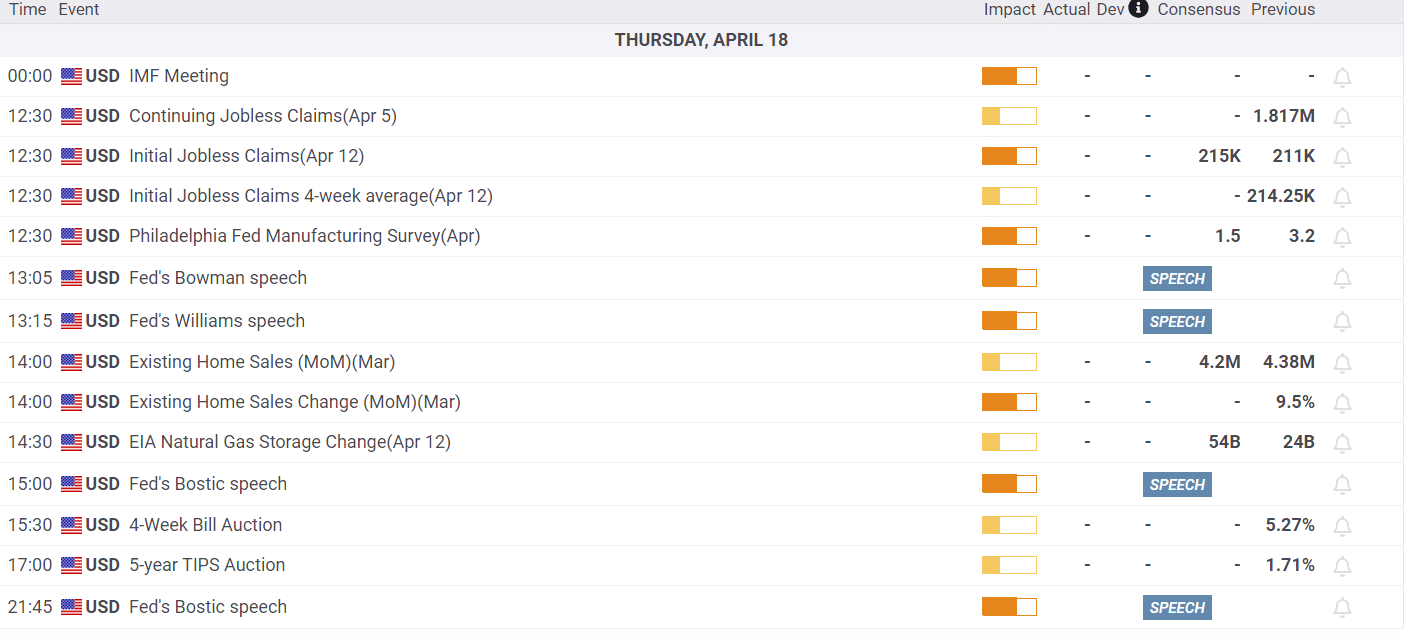

Economy

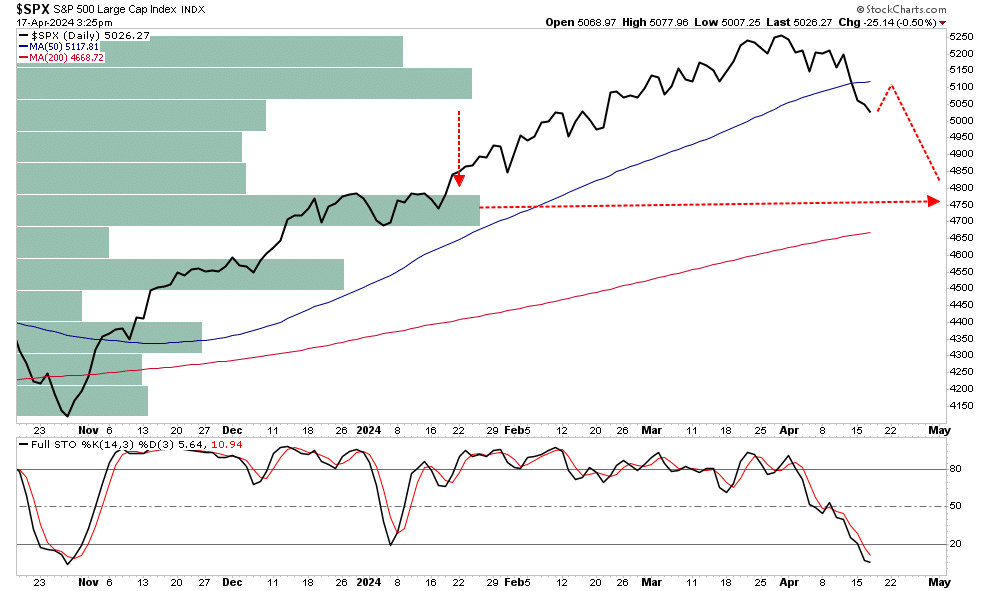

Market Trading Update

The market continues its current correction process. This correction, which we discussed was coming for the last two months, is in process. We noted previously that “sellers live higher, buyers live lower,” which is why the market is declining to try and find where buyers are currently “living.”

As shown, there is a fairly sizable gap between the current and next levels, where most of the volume occurred. However, if that is where the market is ultimately headed, it most likely won’t do it in a straight line. With the market decently oversold and following several consecutive days of selling, a decent bounce toward the 50-DMA is likely. Use that bounce to reduce risk and add hedges as needed.

Given that algorithms and programmatic trading do a large chunk of daily trading activity, it is difficult to know exactly where those programs will turn from “selling rips” back to “buying dips.” However, we have been through these corrections before, and they will end. While corrections are never fun, they provide investors with a great opportunity to buy positions they want at cheaper prices.

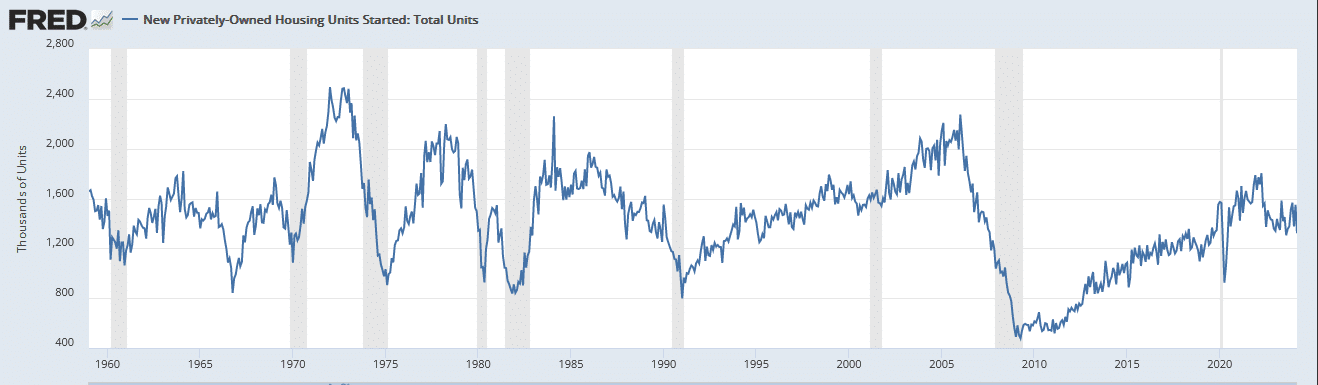

Housing Starts Like Multifamily Building Permits Normalize

Yesterday, we discussed the decline in multifamily building permits and the expected soon-to-come decline in multifamily construction projects. We also shared how the reductions will result in job losses in the construction industry and become a headwind for inflation. Similarly, new housing permits show weakness. Per the Census Bureau, housing starts plunged 14.7% month-over-month in March to an annualized rate of 1.321 million. That was well below forecasts of 1.48 million. It is the lowest reading since August and the biggest decline since April 2020. As we share below, housing starts are now close to pre-pandemic levels.

Wall Street Sticks With 2 Cuts While Powell Buys Time

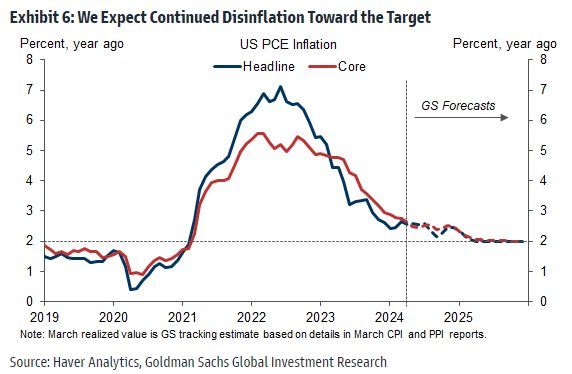

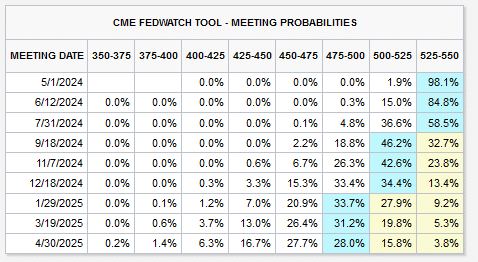

Per BofA, 76% of institutional fund managers polled still expect two or more Fed interest rate cuts in 2024, while 8% project no rate cut at all. The survey was conducted in early April before comments from Jerome Powell on Tuesday. The first graph below shows that Goldman Sachs forecasts that inflation’s rate of decline may be slowing, but it should reach the Fed’s 2% target in early 2025. The second table, courtesy of the CME, shows the market is mixed as to whether there will be one or two cuts by year-end. However, Fed Fund futures imply a zero chance of rate hikes.

On Tuesday, Jerome Powell confirmed what other Fed speakers have been saying. The expected rate cuts are still on the table but will likely be pushed back. Further, Powell raises some doubt about whether the Fed may cut at all this year. However, despite what appears to be a more hawkish tone, we are not hearing anything from Powell regarding the possibility of rate hikes. The recent tightening of financial conditions via higher bond yields and weaker stock prices may also provide the Fed a little comfort in their projections.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”