Trending

Written by: Gabriela Santos and Tom Murray

"Since early November, when vaccine trial results were first announced, international has actually outperformed the U.S. by 3.9 percentage points, and we believe this is only the beginning of the rotation."

International equities have underperformed the U.S. by a cumulative 189% over the past 13 years (in U.S. dollars). Unsurprisingly, many investors are underweight international, with the average portfolio analyzed by our Portfolio Insights team showing a 22% weighting to international equities (versus a “neutral” 35%). Investors should always look forward: a new global economic cycle is beginning in which international can take the baton from the U.S. due to: valuations, U.S. dollar, and cyclicality. Since early November, when vaccine trial results were first announced, international has outperformed the U.S. by 3.9%pts – only the beginning of the rotation.

- Valuation discount: International equities are trading at a discount of 23% versus the U.S., close to a record high and significantly above the 20-year average of 13%. At the beginning of the last cycle, the international discount was only 6%.

- U.S. dollar weakness: We are likely at the beginning of a cycle of U.S. dollar weakness given the prospects for more diversified global growth. During the last cycle, U.S. dollar strength subtracted 24%pts from international returns for U.S. dollar-based investors.

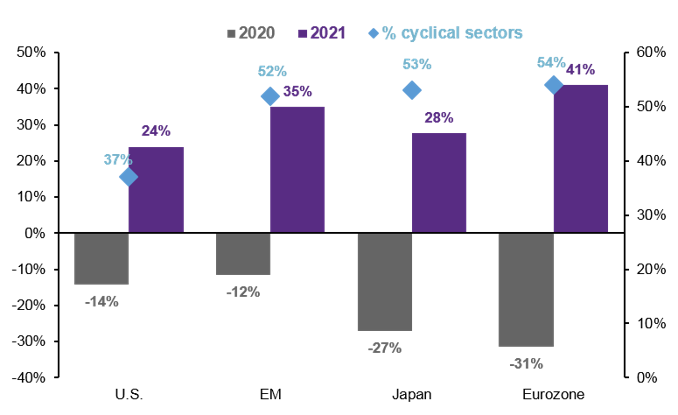

- Cyclicality: International markets have a much larger weighting to cyclical sectors than the U.S. at 56% of the MSCI All Country World ex-U.S. versus only 37% of the S&P 500. International markets stand to benefit the most from the expected surge in global economic growth this year. As the economic recovery takes hold, we expect the outlook for international earnings recovery to outpace that of the U.S. The cyclical nature of those markets will benefit from the reopening of the global economy, and we expect earnings in financials, industrials, and the consumer to lead the recovery.

We would also continue to have investors focus on the impressive array of structural growth opportunities that are available outside the U.S.:

- The decarbonisation and electrification trend is real and accelerating. President Biden’s climate plan and the EU Green Deal will drive investment here. International companies are leading the drive to renewables, with offshore wind capacity currently dominated by European companies.

- We also find genuine technological innovation outside the US. Within semi-conductors for example, where the leading manufacturers of lithography machines, and leading edge foundry all sit in international markets.

- The demographic opportunities in emerging markets remain as attractive today as ever, and we can find exciting investments here both directly and indirectly. The rise of the consumer within these markets provides opportunity for deepening financial penetration, digital platforms to thrive, and for the European luxury goods and beverage companies to find new fast growing markets for their products.

International markets’ cyclicality suggests a stronger earnings rebound this year

Consensus earnings estimates

Source: FactSet, MSCI, Standard & Poor’s, J.P. Morgan Asset Management.

Cyclical sectors include consumer discretionary, financials, industrials, energy and materials.

Data are as of February 5, 2021

Related: How Has the Pandemic Impacted Retirement Strategies?