The big news this week once again coming from the bond market – Treasury Secretary Bessent stated late yesterday that he wanted to focus on 10-year rates rather than the short end of the yield curve. This explains why yesterday’s refunding announcement did not shift Treasury borrowing to longer maturities, as many had expected. It is tough to expect lower long rates while simultaneously increasing supply.

Interestingly, Treasury rates are higher across the curve. It is understandable why the short end is under a bit of pressure, with yields about 2bp higher. The Secretary’s comments said that there will be less of a focus on lowering short rates, partly because he assured us that the President will not be pressing the Federal Reserve to lower rates. Overall, the market should like that the Fed should be able to operate independently, but the combination of continued supply of short-term paper with an unhurried Fed is not helpful to those rates in the near-term. The long end is also about 3bp higher, but that could simply be another sign that bond traders tend to overshoot – with yesterday’s 9bp drop perhaps being a bit too exuberant.

Meanwhile, all sorts of traders can now focus on tomorrow morning’s employment report. The consensus estimate for January Nonfarm Payrolls is 173,000, though ForecastEx shows a 60% chance that the number will be above 180k. The Unemployment Rate is expected by economists to remain unchanged at 4.1%, while ForecastEx traders have a 57% preference for a higher number.

Options markets are relatively sanguine ahead of the report, though. S&P 500 (SPX) options expiring tomorrow show a peak probability in the 6105-6110 range, about ½% above the current index level.

IBKR Probability Lab for SPX Options Expiring February 7th, 2025

Source: Interactive Brokers

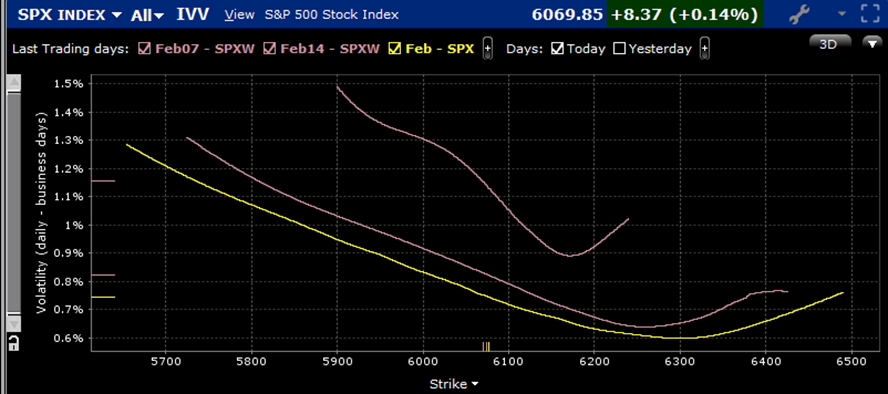

That said, we see a relatively steep skew for options expiring tomorrow, along with a relatively elevated 1.15% daily implied volatility:

Skews for SPX Options Expiring February 7th (top), 14th (middle) 21st (AM, bottom)

Source: Interactive Brokers

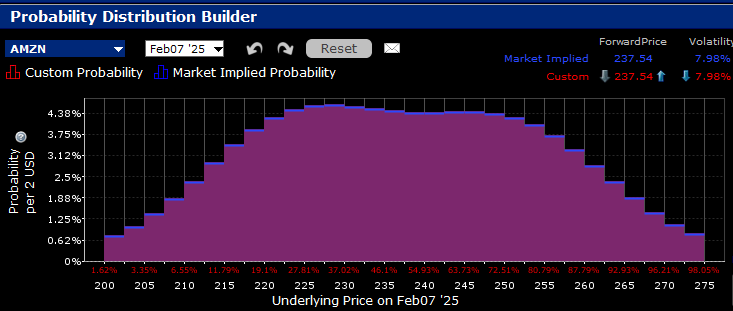

At the same time, traders are far mor unsure about the post-earnings prospects for Amazon (AMZN), who reports after today’s close. Although the peak is in the $227.5-$230 range, somewhat below the current price, the market assigns relatively equal probabilities to outcomes anywhere between $225 and $250:

IBKR Probability Lab for AMZN Options Expiring February 7th, 2025

Source: Interactive Brokers

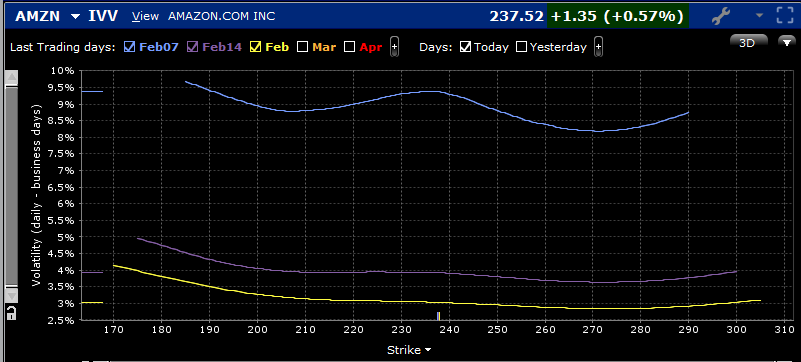

As we might expect from the probability graph above, we see an extraordinarily flat skew in options expiring tomorrow. Perhaps after the recent cloud-computing induced stumbles in Microsoft (MSFT) and Alphabet (GOOGL, GOOG), traders are roughly equally split between concerns about too much competition in that sector versus optimism that AMZN is gaining share at their expense. However, the at-money volatility of just under 9.5% is elevated when compared to the 6.71% average of the past 6 post-earnings moves (+6.19%, -8.78%, +2.29, +7.87%, +6.83%, +8.27%)

Skews for AMZN Options Expiring February 7th (top), 14th (middle) 21st (bottom)

Source: Interactive Brokers

Overall, both stock and markets seem disinclined to do too much today. With potentially market moving events lurking on the horizon, that seems quite sensible.

Related: More About Moats: Do They Still Protect Businesses?